中東・アフリカの産業用空気質管理システム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Middle-East and Africa Industrial Air Quality Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687293

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

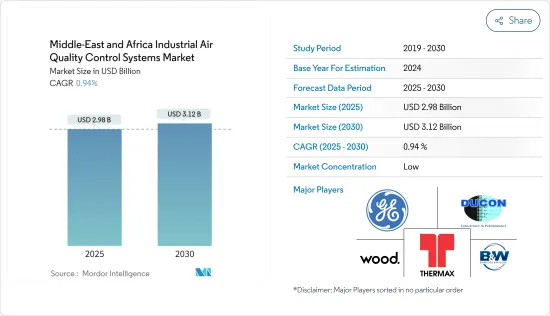

中東・アフリカの産業用空気質管理システムの市場規模は2025年に29億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは0.94%で、2030年には31億2,000万米ドルに達すると予測されます。

主なハイライト

- 長期的には、産業インフラの急増と大気質問題が相まって、中東・アフリカの大気質管理システム市場を予測期間中に牽引するとみられます。

- 一方、いくつかの憲法上の障壁や、無公害の再生可能エネルギー利用の増加が、市場調査の主な抑制要因になると予想されます。

- とはいえ、この地域全体の政府によって設定された厳しい規制基準を満たすために、古い産業プラントの大気質制御システムによる改修は、将来的に機会として作用する可能性が高いです。

中東・アフリカの産業用空気質管理システム市場動向

鉄鋼が市場で大きなシェアを占める見込み

- 一貫生産、直接還元鉄、電気炉のいずれかの方法で生産される鉄鋼は、原料の輸送、貯蔵、マテリアルハンドリング、加熱、変成を必要とします。これらの工程はすべて、主に粉塵(または粒子状物質(PM))、二酸化硫黄(SO2)、亜酸化窒素(NOx)の形で大気への排出を発生させる可能性があります。その他に少量発生する排出物には、ダイオキシン類や重金属があり、これらは通常、粉塵粒子に付着しています。

- 高炉からのキャストハウス床からの排出を含む製鉄・製鋼作業からの排出は、建物内の収集ポイントを持つ二次除塵システム(i.e.バッグフィルター、湿式スクラバー、ESPなど)を介して制御されます。

- すべての製鉄所は、大気への排出を制限する要件を設定する環境規制の対象です。現代生活の大部分は鉄鋼で構成されています。インフラ、建物、機械、電気機器、自動車、そして調理器具から家具に至るまで、さまざまな製品が大量の鉄と鋼を必要とします。鉄鋼需要は2050年までに5倍になると推定されています。

- 世界鉄鋼協会の統計によると、2022年現在、同地域の粗鋼生産は主にトルコ、イラン、サウジアラビア、南アフリカ、アルジェリア、アラブ首長国連邦などの国々が独占しています。

- 中東・アフリカ地域は、高品位の鉄鉱石が入手可能なため、鉄鋼生産のポテンシャルが非常に高いです。さらに、近年、この地域の鉄鋼生産は、特に中東・北アフリカ地域における鉄鋼部門への投資の増加などにより、著しい成長を遂げています。

- 2022年5月、アルセロール・ミッタルはモーリタニアに拠点を置く鉄鉱石採掘会社SNIMと、モーリタニアにおけるペレット化プラントと直接還元鉄生産プラントを共同開発する機会を評価するための拘束力のない覚書に調印しました。

- 2022年9月、サウジアラビアは総額93億2,000万米ドル、年間生産能力620万トンの3つの鉄鋼生産プロジェクトを実施する意向であると発表しました。同月、Essar Groupは、同国での一貫平鋼工場設立に40億米ドルを投資することを発表しました。この工場は年間400万トンの鉄鋼生産能力を持ち、2025年までに完成する予定です。

- 同地域の鉄鋼・製鉄業における開発と投資を考慮すると、産業用空気質管理システムの需要は予測期間中に大幅な成長が見込まれます。

サウジアラビアが市場を独占

- サウジアラビアは、発電、セメント、石油・ガス、金属、その他のセクターの著しい成長により、産業用空気質管理システムの最大かつ急成長市場の1つになる可能性が高いです。これらの産業にとって空気品質制御システム(AQCS)は極めて重要であるため、予測期間中も同様のペースで市場が成長し、市場の成長を支えるものと予想されます。

- サウジアラビアはこの地域で最大の汚染国のひとつであり、2022年のCO2排出量はCO2換算で約7億2,400万トンに達します。国民1人当たりのCO2排出量は約19トンと、世界でも有数の排出国です。

- 石油・ガスなどの化石燃料から発電される電力が大きな割合を占めており、大気質制御システムなど、より高度な技術を導入する道を開いています。2022年、サウジアラビアの発電量は化石燃料が約99.8%を占め、次いで非水力再生可能エネルギー(~0.2%)が続きます。

- さらに、同国は化石燃料ベースの発電プロジェクトへの投資を続けており、これがIAQCS市場の需要を支えるものと期待されています。例えば、2022年9月、韓国のDoosan Enerbility社は、サウジアラビアで3億8,300万米ドルの熱電併給発電所の建設契約を受注しました。2025年に予定されている建設工事の完了後、このプラントは320MWの電力と毎時314トンの蒸気を発電し、ジャフラ・ガス田に電力と熱を供給する予定です。

- さらに、石油・ガス、鉱業、金属セクターの急成長により、大気中の汚染物質レベルが大幅に上昇しています。したがって、工業用空気品質管理システム(IAQCS)の採用が予想されます。

- 鉄鋼業界も大気汚染の大きな原因となっています。鉄鋼は主に石炭をエネルギー源としているため、石炭の燃焼によってかなりの排出量が発生します。製鉄所は、粒子状物質(PM2.5およびPM10)、二酸化炭素、硫黄酸化物、窒素酸化物、一酸化炭素などの大気汚染物質を排出するため、サウジアラビアでは産業用大気質管理システム(IAQCS)の潜在的なエンドユーザーとなっています。

- 世界鉄鋼協会によると、2022年のサウジアラビアの鉄鋼生産量は約910万トンで、前年比4.5%増加しました。2022年9月、投資大臣によると、サウジアラビアでは、低コストの電力や天然ガスなどの技術オプションや、サウジ・グリーン・イニシアチブなどの政府プログラムにより、鉄鋼業界はグリーンで持続可能な製品への移行に適した位置にあります。

- さらに、サウジは新しい製油所や石油化学コンビナートの建設を進めています。例えば、2022年12月、サウジアラビア石油公社とトタルエナジーズは、世界規模の石油化学施設の建設に関する最終投資決定に達しました。アミラル」コンプレックスは、サウジアラビアの東海岸ジュベイルに位置する既存のサウジアラムコ・トタル精製石油化学(SATORP)製油所と一体的に運営、所有、統合される予定です。石油化学施設の建設により、SATORPはアラムコから供給される製油所オフガス、ナフサ、エタン、天然ガソリンをより価値の高い化学品に変換することができるようになり、アラムコの液体から化学品への戦略をサポートします。このコンプレックスの一部として、年間165万トンのエチレンを生産できる混合フィード・クラッカーが建設されます。

- 南アフリカにおける様々な産業への現在の投資とそのバリューチェーンの成長を考慮すると、製造業は同国の産業用空気質管理システムの成長にとって極めて重要です。

中東・アフリカの産業用空気質管理システム産業の概要

中東・アフリカの産業用空気質管理システム市場は断片化されています。主要企業(順不同)には、Alfa Laval AB、Aircure、CFW Environmental、Pure Air Solutions、ERG Groupなどがいます。

CFWエンバイロメンタルの大気汚染防止システムのポートフォリオは、数多くの産業用途の要件や特定の属性に準拠するためのさまざまな技術に基づいています。さらに同社は、最初の問い合わせからアフターサービスに至るまで、包括的なサービスを提供しています。また、大気汚染防止システムの設計と製造において、国際的なベストプラクティスの採用にも注力しています。世界市場で持続可能であり続けるために、市場調査と革新的な製品開発を通じて顧客の要件を評価し、製品を常に強化しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- ダウンストリーム産業からの需要

- 抑制要因

- 再生可能でクリーンなエネルギー源の採用

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 電気集塵装置(ESP)

- 排煙脱硫装置(FGD)とスクラバー

- 選択触媒還元(SCR)

- ファブリックフィルター

- その他

- 用途

- 発電産業

- セメント産業

- 化学・肥料

- 鉄鋼業界

- 自動車産業

- 石油・ガス産業

- その他の用途

- 排出ガス

- 窒素酸化物(NOX)

- 硫黄酸化物(SO2)

- 粒子状物質(PM)

- 地域

- サウジアラビア

- 南アフリカ

- アルジェリア

- その他中東とアフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Alfa Laval AB

- Aircure

- CFW Environmental

- Pure Air Solutions

- The ERG Group

- Redecam Group SpA

- Donaldson Company Inc.

- Durr AG

- FLSmidth & Co. A/S

- Siloxa Engineering AG

第7章 市場機会と今後の動向

- 各社による新技術大気品質管理システムの開発

目次

The Middle-East and Africa Industrial Air Quality Control Systems Market size is estimated at USD 2.98 billion in 2025, and is expected to reach USD 3.12 billion by 2030, at a CAGR of 0.94% during the forecast period (2025-2030).

Key Highlights

- Over the longer term, a surge in industrial infrastructure, coupled with air quality issues, is expected to drive the market for air quality control systems in Middle-East and Africa over the forecast period.

- On the other hand, several constitutional barriers and growth in renewable energy usage which is pollution-free are expected to act as major restraints for the market studied.

- Nevertheless, retrofitting of old industrial plants with air quality control system to meet stringent regulatory norms set up by governments across the region is likely to acts as an opportunity in the future.

MEA Industrial Air Quality Control Systems Market Trends

Iron and Steel is Expected to Have Significant Share in the Market

- Steel, produced by either integrated, direct reduced iron, or electric arc furnace route, requires transportation, storage, handling, heating, and transformation of raw materials. All these processes have the potential to generate emissions into the air, primarily in the form of dust (or particulate matter (PM), sulfur dioxide (SO2), and nitrous oxides (NOx). Other emissions generated in small quantities include dioxins and heavy metals, typically attached to dust particles.

- Emissions from iron and steelmaking operations, including cast house floor emissions from blast furnaces, are controlled via secondary dedusting systems (i.e., bag filters, wet scrubbers, ESPs, etc.) with a collection point inside the building.

- All steel plants are subject to environmental regulation, which sets the requirements to restrict emissions into the air. A large portion of modern life is comprised of steel. Infrastructure, buildings, machinery, electrical equipment, automobiles, and various products, from cookware to furniture, require large amounts of iron and steel. The steel demand is estimated to increase by five times by 2050.

- According to the World Steel Association statistics, as of 2022, the crude steel production in the region is mainly dominated by countries like Turkey, Iran, Saudi Arabia, South Africa, Algeria, and the United Arab Emirates, amongst others.

- The Middle East and Africa region has a very high potential for steel production due to the availability of high-grade iron ore. Additionally, in recent years steel production in the area has witnessed significant growth, mainly driven by increasing investments in the sector, especially in the Middle East and North Africa.

- In May 2022, ArcelorMittal signed a non-binding Memorandum of Understanding with SNIM, an iron ore mining company based in Mauritania, to evaluate an opportunity to jointly develop a pelletization plant and a direct reduced iron production plant in Mauritania.

- In September 2022, Saudi Arabia announced that it intends to implement three steel production projects worth USD 9.32 billion with a total production capacity of 6.2 million tons annually. In the same month, Essar Group announced it is looking to invest USD 4 billion in setting up an integrated flat steelworks plant in the country. The plant will have a steel production capacity of 4 million tonnes annually and will be completed by 2025.

- Considering the developments and investments in the steel and iron industry in the region, the demand for industrial air quality control systems is expected to witness significant growth during the forecast period.

Saudi Arabia to Dominate the Market

- Due to the significant growth in its power generation, cement, oil & gas, metal, and other sectors, Saudi Arabia is likely to be one of the largest and fastest-growing markets for industrial air quality control systems. The market is expected to grow at a similar rate during the forecast period, supporting the market growth, as air quality control systems (AQCS) are crucial to these industries.

- Saudi Arabia is one of the largest polluters in the region, with CO2 emissions amounting to approximately 724 million tonnes of CO2 equivalent in 2022. The country is one of the largest producers of CO2 emissions per capita worldwide, at about 19 metric tons per person.

- A significant share of power generated from fossil fuels, such as oil and gas, paving the way for more advanced technologies, such as air quality control systems, to be implemented. In 2022, Saudi Arabia's power generation was dominated by fossil fuels, which account for approximately 99.8% of the electricity generated, followed by non-hydro renewable sources (~0.2%).

- Further, the country continues to invest in fossil fuel-based power projects, which are expected to support the demand for the IAQCS market. For instance, in September 2022, South Korean company Doosan Enerbility was awarded a contract to construct a combined heat and power plant in Saudi Arabia valued at USD 383 million. Upon completion of the construction work scheduled for 2025, the plant will generate 320 MWs of electricity and 314 tons per hour of steam to supply electricity and heat to the Jafurah gas field.

- Further, the rapid growth of the oil & gas, mining, and metal sectors has resulted in a massive increase in the levels of pollutants in the air. Accordingly, the adoption of industrial air quality control systems (IAQCS) is anticipated.

- The Iron and Steel industry is another significant contributor to air pollution. Steel mainly requires coal for energy, so considerable emissions are caused by coal combustion. Steel plants emit air pollutants, such as particulate matter (PM2. 5 and PM10), carbon dioxide, sulfur oxides, nitrogen oxides, carbon monoxide, etc. hence, being a potential end-user for the industrial air quality control systems (IAQCS) in Saudi Arabia.

- According to World Steel Association, in 2022, steel production in Saudi Arabia was approximately 9.1 million, an increase of 4.5% from the previous year. In September 2022, according to the minister of investment, In Saudi Arabia, the iron and steel industry is well positioned for the transition to green and sustainable products due to its technology options, such as low-cost electricity and natural gas, and government programs, such as the Saudi Green Initiative.

- Further, the country has been constructing new refineries and petrochemical complexes. For instance, in December 2022, Saudi Arabian Oil Company and TotalEnergies reached a final investment decision on constructing a world-scale petrochemical facility. The "Amiral" complex is going to be operated, owned, and integrated with the existing Saudi Aramco Total Refining and Petrochemical Co. (SATORP) refinery located on Saudi Arabia's eastern coast, Jubail. With the construction of the petrochemical facility, SATORP will be able to convert its refinery off-gases, naphtha, ethane, and natural gasoline supplied by Aramco into higher-value chemicals, thus supporting Aramco's liquids-to-chemicals strategy. As part of the complex, there will be a mixed feed cracker capable of producing 1.65 million tons of ethylene annually, a first of its kind in the region that will be integrated with a refinery.

- Considering the current investments in the various industries and the increased growth of its value chain in South Africa, the manufacturing sector is critical to the growth of the country's industrial air quality control systems.

MEA Industrial Air Quality Control Systems Industry Overview

The Middle-East and Africa industrial air quality control systems market is fragmented. some of the key players (in no particular order) include Alfa Laval AB, Aircure, CFW Environmental, Pure Air Solutions, and ERG Group, among others.

CFW Environmental's portfolio of air pollution control systems is based on a range of technologies to comply with the numerous industrial application requirements and specific attributes. Furthermore, the company provides comprehensive services, ranging from first inquiry to after-sales service. It also focused on adopting international best practices in designing and manufacturing air pollution control systems. To remain sustainable in the global market, the products are constantly enhanced by evaluating customers' requirements through market research and innovative product development.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Demand from the Downstream Industry

- 4.5.2 Restraints

- 4.5.2.1 Adoption of Renewable and Clean Energy Sources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Electrostatic Precipitators (ESP)

- 5.1.2 Flue Gas Desulfurization (FGD) and Scrubbers

- 5.1.3 Selective Catalytic Reduction (SCR)

- 5.1.4 Fabric Filters

- 5.1.5 Others

- 5.2 Application

- 5.2.1 Power Generation Industry

- 5.2.2 Cement Industry

- 5.2.3 Chemicals and Fertilizers

- 5.2.4 Iron and Steel Industry

- 5.2.5 Automotive Industry

- 5.2.6 Oil & Gas Industry

- 5.2.7 Other Applications

- 5.3 Emissions

- 5.3.1 Nitrogen Oxides (NOX)

- 5.3.2 Sulphur Oxide (SO2)

- 5.3.3 Particulate Matter (PM)

- 5.4 Geography

- 5.4.1 Saudi Arabia

- 5.4.2 South Africa

- 5.4.3 Algeria

- 5.4.4 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Alfa Laval AB

- 6.3.2 Aircure

- 6.3.3 CFW Environmental

- 6.3.4 Pure Air Solutions

- 6.3.5 The ERG Group

- 6.3.6 Redecam Group SpA

- 6.3.7 Donaldson Company Inc.

- 6.3.8 Durr AG

- 6.3.9 FLSmidth & Co. A/S

- 6.3.10 Siloxa Engineering AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Technology Air Quality Control System Developments by Various Companies

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日