|

市場調査レポート

商品コード

1687185

板ガラス:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Flat Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 板ガラス:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

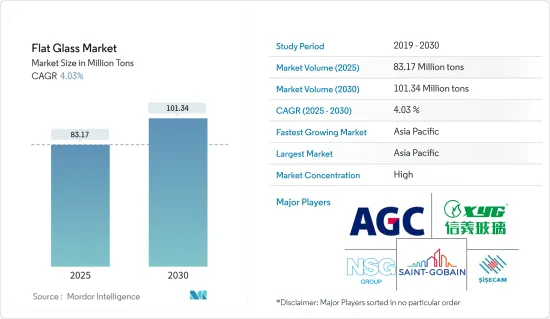

板ガラス市場規模は2025年に8,317万トンと推定され、予測期間(2025~2030年)のCAGRは4.03%で、2030年には1億134万トンに達すると予測されます。

COVID-19は市場にマイナスの影響を与えました。パンデミックによりほとんどの製造施設が閉鎖され、自動車生産に深刻な影響を与えました。さらに、パンデミックの発生による経済不安も建設産業の落ち込みにつながりました。現在、市場はパンデミックから回復し、著しい成長を見せています。

主要ハイライト

- 短期的には、建設セクターへの投資拡大と自動車産業からの需要増加が市場成長の主要要因です。

- しかし、代替品の入手可能性が市場の成長を抑制する可能性が高いです。

- しかし、太陽エネルギーセグメントで新たな機会が生まれれば、世界市場に有利な成長機会がまもなく生まれると考えられます。

- アジア太平洋が市場を独占し、予測期間中に最も高い年間成長率を記録すると予想されます。

板ガラス市場の動向

建設産業が市場を独占する見込み

- 建築・建設産業の要である板ガラスは、極めて重要な役割を果たしています。薄板ガラスは透明で自然光を取り入れ、屋内と屋外のギャップを埋める役割を果たします。これにより、居住者の福利厚生が向上し、人工照明の必要性が減少します。

- 板ガラスは切断、成形、加工が容易で、多様な美的・機能的要求を満たすことができるため、その多様性が光ります。着色、反射、エネルギー効率に優れたコーティングなど、現代の板ガラスはその強度、耐傷性、風化に対する耐久性で際立っています。また、板ガラスはリサイクル可能であるだけでなく、再生材を使用することも可能です。

- アジア太平洋は世界最大の建設産業であり、人口の急増、中間所得層の所得増加、急速な都市化がその成長を後押ししています。この勢いは、現在進行中の多数の住宅・商業プロジェクトによってさらに強化され、製品の需要を下支えしています。

- インドのムンバイでは、3,000万米ドル規模のArkade Aspire Residential Complexプロジェクトが進行中です。総面積3万5,366平方メートルの18階建て住宅タワーを2棟建設するという意欲的な試みで、2022年第2四半期に着工し、2025年第1四半期の完成を目指しています。

- 米国の建築・建設産業は依然として経済の要です。米国国勢調査局によると、2023年の建設総額は1兆9,787億米ドルで、2022年の1兆8,487億米ドルから7%増加しました。特に、住宅建設は2023年に8,649億米ドルを占めました。

- さらに、米国では商業建設プロジェクトが急増しており、産業の需要拡大が見込まれています。特に、2024年1月、インディアナ州政府はMeta Platforms Inc.と共同で、フージャー州に8億米ドルのデータセンターキャンパスの建設を開始しました。リバー・リッジ・コマースセンターにあるこの70万平方フィートの施設は、2026年までに完成する予定です。

- さらに南アフリカ政府は、中低所得者層に手頃な価格の住宅を提供するため、数多くの住宅プロジェクトに着手しています。

- 2020年に発表されたハウテン州のムーイクルーフ・メガシティプロジェクトもそのひとつです。2023年に完了予定の第1段階は、2030年までの完成を目指すより大きなビジョンの一部です。この野心的なプロジェクトは、住宅、商業施設、教育施設を含む5万戸を想定しています。

- 建設産業におけるこのような事業の規模と勢いを考えると、板ガラスの需要は今後数年間で様々な用途で急増するものと考えられます。

アジア太平洋が市場を独占する見込み

- アジア太平洋は、建築・建設、自動車、ソーラーガラスなどの用途で需要が増加しており、板ガラス市場を独占すると予想されています。

- 中国自動車工業会(CAAM)の最新データによると、同国の自動車生産台数は2023年に3,016万台を突破し、前年比11.6%増となりました。2023年の乗用車販売台数は3,009万台で、前年比12%増となりました。

- さらに、インド自動車製造協会(SIAM)が発表したデータによると、2023会計年度には458万台の自動車が製造されたのに対し、2022会計年度には365万台が製造されました。2023年度の自動車生産台数は前年度比で約25%増加しました。

- また、国土交通省が発表した最新データによると、2023年度に着工した新築住宅は81万9,620戸に上りました。

- また、インド政府は2023年11月、全国12州で合計容量約3,749万kWの50のソーラーパークを承認しました。2023年1月から11月までに、系統連系屋根上ソーラープログラムのもとで741MW以上の容量が設置されました。

- 従って、自動車、建設、その他の産業の成長が、予測期間中の同地域の板ガラス市場を牽引すると考えられます。

板ガラス産業概要

板ガラス市場は部分的に統合されています。主要企業(順不同)には、AGC Inc.、Xinyi Glass Holdings Limited、Saint-Gobain、Nippon Sheet Glass、Sisecamが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設産業への投資拡大

- 自動車産業からの需要増加

- 抑制要因

- 代替品の入手可能性

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ

- アニールガラス

- 透明ガラス

- 着色ガラス

- コーターガラス

- 反射ガラス

- 低Eガラス

- 加工ガラス

- 合わせガラス

- 強化ガラス

- ミラーガラス

- パターンガラス

- アニールガラス

- エンドユーザー産業

- 建築・建設

- 自動車

- ソーラーガラス

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Adamant Holding Company

- AGC Inc.

- Cardinal Glass Industries Inc.

- Central Glass Co. Ltd

- China Glass Holdings Limited

- Euroglas

- Guardian Industries

- Nippon Sheet Glass Co. Ltd

- Phoenicia

- Saint-Gobain

- SCHOTT

- Sisecam

- Taiwan Glass Ind. Corp.

- Vitro

- Xinyi Glass Holdings Limited

第7章 市場機会と今後の動向

- 太陽エネルギーにおける新たな機会

The Flat Glass Market size is estimated at 83.17 million tons in 2025, and is expected to reach 101.34 million tons by 2030, at a CAGR of 4.03% during the forecast period (2025-2030).

COVID-19 negatively impacted the market. Most manufacturing facilities were shut down due to the pandemic, severely affecting automotive production. Further, economic instability caused by the pandemic outbreak also led to a downfall in the construction industry. Currently, the market has recovered from the pandemic and is growing at a significant rate.

Key Highlights

- Over the short term, the growing investments in the construction sector and increasing demand from the automotive industry are major factors driving the growth of the market.

- However, the availability of alternatives is likely to restrain the growth of the market.

- However, emerging opportunities in the solar energy sector will likely create lucrative growth opportunities for the global market soon.

- Asia-Pacific is expected to dominate the market and is likely to witness the highest annual growth rate during the forecast period.

Flat Glass Market Trends

The Construction Industry is Expected to Dominate the Market

- Flat glass, a cornerstone of the building and construction industry, plays a pivotal role. It offers clarity, ushering in natural light, and bridges the gap between indoor and outdoor spaces. This enhances occupant well-being and reduces the need for artificial lighting.

- Its versatility shines as flat glass can be easily cut, shaped, and treated to meet diverse aesthetic and functional demands. Whether tinted, reflective, or energy-efficiently coated, modern flat glass stands out for its strength, scratch resistance, and durability against weathering. Additionally, flat glass is not only recyclable but can also be crafted with recycled content.

- Asia-Pacific boasts the world's largest construction industry, a growth primarily fueled by a burgeoning population, rising middle-class incomes, and rapid urbanization. This momentum is further bolstered by a slew of ongoing residential and commercial projects, underpinning the demand for the product.

- In Mumbai, India, the Arkade Aspire Residential Complex project, valued at USD 30 million, is underway. This ambitious endeavor involves erecting two 18-story residential towers covering a total area of 35,366 sq. m construction commenced in Q2 2022 and is slated for completion by Q1 2025.

- The building and construction industry in the United States remains a cornerstone of its economy. In 2023, the US Census Bureau reported a total construction value of USD 1,978.7 billion, marking a 7% increase from the USD 1,848.7 billion spent in 2022. Notably, residential construction accounted for USD 864.9 billion in 2023.

- In addition, the United States is witnessing a surge in commercial construction projects, promising a heightened demand for the industry. Notably, in January 2024, Indiana's government, in collaboration with Meta Platforms Inc., commenced the construction of a USD 800 million data center campus in Hoosier State. This 700,000-square-foot facility at the River Ridge Commerce Center is slated for completion by 2026.

- Moreover, the South African government has embarked on numerous residential projects to provide affordable housing to its middle and lower-income populations.

- One such initiative is the Mooikloof Mega City project in Gauteng, which was announced in 2020. Its Phase 1, set to conclude in 2023, is part of a larger vision that anticipates completion by 2030. The ambitious project envisions 50,000 units, encompassing residential spaces, commercial establishments, and educational facilities.

- Given the scale and momentum of such ventures in the construction industry, the demand for flat glass is set to surge across various applications in the coming years.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is expected to dominate the market for flat glass with the increasing demand for applications in building and construction, automobiles, solar glasses, etc.

- According to the most recent data from the China Association of Automobile Manufacturers (CAAM), car production in the country surpassed 30.16 million units in 2023, marking an 11.6% increase compared to the previous year. A total of 30.09 million units of passenger cars were sold in the country in 2023, registering a 12% increase compared to the previous year.

- Further, according to the data released by the Society of India Automotive Manufacturing (SIAM), 4.58 million automotive vehicles were manufactured in the financial year 2023, compared to 3.65 million vehicles produced in the financial year 2022. The country saw a rise of around 25% in automotive production in 2023 compared to the previous year.

- In addition, according to the latest data released by the Ministry of Land Infrastructure, Transport and Tourism (MLIT) Japan, a total of 819.62 thousand new construction houses started in 2023.

- Also, the Government of India approved 50 solar parks with an aggregate capacity of around 37,490 MW in 12 states across the country in November 2023. More than 741 MW capacity was installed under the grid-connected rooftop solar program from January to November 2023.

- Therefore, the growth in automotive, construction, and other industries is likely to drive the market for flat glass in the region during the forecast period.

Flat Glass Industry Overview

The flat glass market is partially consolidated in nature. The major players (not in any particular order) include AGC Inc., Xinyi Glass Holdings Limited, Saint-Gobain, Nippon Sheet Glass Co. Ltd, and Sisecam.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Investments in the Construction Industry

- 4.1.2 Increasing Demand From the Automotive Industry

- 4.2 Restraints

- 4.2.1 Availability of Alternatives

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Annealed Glass

- 5.1.1.1 Clear Glass

- 5.1.1.2 Tinted Glass

- 5.1.2 Coater Glass

- 5.1.2.1 Reflective Glass

- 5.1.2.2 Low E Glass

- 5.1.3 Processed Glass

- 5.1.3.1 Laminated Glass

- 5.1.3.2 Tempered Glass

- 5.1.4 Mirror Glass

- 5.1.5 Patterned Glass

- 5.1.1 Annealed Glass

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Solar Glass

- 5.2.4 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Adamant Holding Company

- 6.4.2 AGC Inc.

- 6.4.3 Cardinal Glass Industries Inc.

- 6.4.4 Central Glass Co. Ltd

- 6.4.5 China Glass Holdings Limited

- 6.4.6 Euroglas

- 6.4.7 Guardian Industries

- 6.4.8 Nippon Sheet Glass Co. Ltd

- 6.4.9 Phoenicia

- 6.4.10 Saint-Gobain

- 6.4.11 SCHOTT

- 6.4.12 Sisecam

- 6.4.13 Taiwan Glass Ind. Corp.

- 6.4.14 Vitro

- 6.4.15 Xinyi Glass Holdings Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Opportunity in the Solar Energy