光学コーティング-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Optical Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687128

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

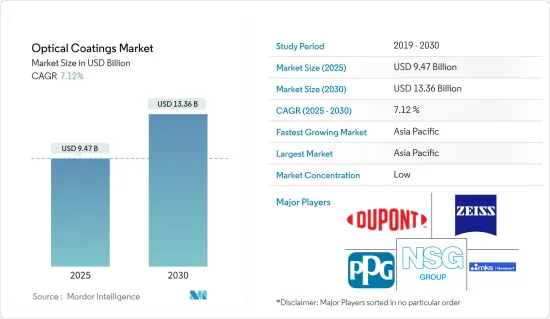

光学コーティング市場規模は2025年に94億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.12%で、2030年には133億6,000万米ドルに達すると予測されます。

主要ハイライト

- 短期的には、太陽電池産業からの光学コーティング需要の増加と光学コーティングプロセスの技術進歩が市場を牽引すると予想されます。

- 高コストと光学コーティングのいくつかの制限特性が市場成長の妨げになると予想されます。

- 電気自動車に対する今後の需要は、今後数年間で市場に機会をもたらすと考えられます。

- アジア太平洋が市場を独占し、予測期間中に最も高いCAGRで推移する可能性が高いです。

光学コーティング市場動向

エレクトロニクス半導体セグメントが市場を独占する見込み

- 光学コーティングは、光が光学表面をシームレスに通過することを保証する、電子アプリケーションにおいて極めて重要な役割を果たしています。スマートフォン、タブレット端末、ウェアラブル端末などの最先端電子機器に対する需要が急増するにつれ、高級光学コーティングに対する需要も急増しています。これらのコーティングは、電子ディスプレイの性能を高めるだけでなく、耐久性も向上させています。

- 透明導電性コーティングは、電子ディスプレイにも採用されています。注目される市場は、コンシューマーエレクトロニクスの需要の絶え間ない成長によって支えられています。デバイスが小型化し、コンパクトになるにつれて、巧みな光学コーティングの必要性が高まっています。これらのコーティングは、熱を巧みに管理し、まぶしさを緩和し、小型部品の光学的透明度を高めています。

- 半導体産業は、精密で高性能な光学コーティングを優先しています。半導体製造の要であるフォトリソグラフィーに不可欠なこれらのコーティングは、半導体デバイスの効率と品質を向上させます。様々なセグメントでIoTの影響力が高まるにつれ、半導体の需要が急増し、光学コーティング市場を後押ししています。

- 例えば、社団法人電子情報技術産業協会(JEITA)のデータによると、2023年に日本のエレクトロニクスセグメントの生産額は10兆7,000億円(約760億米ドル)に迫るといいます。民生用電子機器、産業用機器、無数の電子部品を含むエレクトロニクス産業は、2024年までに3兆6,800億米ドルに達すると予測され、前年比9%増という素晴らしい成長を遂げます。

- 世界半導体貿易統計は2023年12月31日、2023年の世界半導体市場規模は5,268億9,000万米ドルで、2024年には16.0%の成長が見込まれると報告しました。

- ZVEIが2024年7月に発表したデータによると、ドイツの電子・デジタルセクターの2023年の売上高は2,380億ユーロ(2,592億8,000万米ドル)で、前年比10%の堅調な伸びを示しました。

- このような動態を踏まえると、同市場は当面大きな動きを見せそうです。

アジア太平洋が市場を独占する見込み

- 予測期間中、アジア太平洋が光学コーティング市場をリードするとみられます。中国、日本、インド、韓国などの主要国では、エレクトロニクス、半導体、航空宇宙、防衛などさまざまなセグメントで光学コーティングの需要が急増しています。

- 2024年7月12日に中国民用航空局(CAAC)が発表したデータによると、2024年上半期の旅客輸送量は3億5,000万米ドルを超え、前年同期比23.5%増、2019年同期比9%増を記録しました。

- さらに、2023年12月のAviation A2Zの報告書は、中国が17機の国産航空機(COMAC)を取得し、今後2年間に引き渡しが予定されていることを強調し、光学コーティングの需要をさらに強化しています。

- India Brand Equity Foundation(IBEF)によると、インドは2024年に再生可能エネルギー、風力発電、太陽光発電容量で世界第4位にランクされます。Annual 2023 India Solar Market Updateによると、2023年12月末までにインドの太陽光発電の累積容量は約135GWに達し、2025年3月までに約170GWに達すると予測されています。

- IBEFはまた、政府の支援と有利な経済性に後押しされ、再生可能エネルギー部門が投資家を惹きつける魅力となっていることを強調しました。自給自足を目指すインドは、2040年までに1万5,820TWhに達すると予測されるエネルギー需要を満たすことを目指しています。

- 日本電子情報技術産業協会(JEITA)の報告によると、2023年には、電子部品デバイスは日本のエレクトロニクス産業に約6兆9,700億円(470億米ドル)貢献し、その総生産額は約10兆7,000億円(760億米ドル)を誇りました。

- このような力学を考えると、アジア太平洋の光学コーティング市場は予測期間中に安定した成長を遂げると考えられます。

光学コーティング産業概要

光学コーティング市場は、その性質上、非常に細分化されています。同市場の主要企業(順不同)には、DuPont、Zeiss International、Newport Corporation、PPG Industries Inc.、Nippon Sheet Glassなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 太陽電池産業からの需要拡大

- 光学コーティングプロセスにおける技術進歩

- 抑制要因

- 高いコストと光学コーティングのいくつかの制限特性

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ別

- 光学フィルターコーティング

- 反射防止コーティング

- 透明導電性コーティング

- ミラーコーティング(高反射率)

- ビームスプリッターコーティング

- その他の製品タイプ(温度管理コーティング)

- 技術別

- 化学蒸着

- イオンビームスパッタリング

- プラズマスパッタリング

- 原子層蒸着

- サブ波長構造表面

- エンドユーザー産業別

- 航空宇宙・防衛

- エレクトロニクスと半導体

- 通信

- 医療

- ソーラー

- 自動車

- その他のエンドユーザー産業(軍事・防衛、医療)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Abrisa Technologies

- AccuCoat inc.

- Artemis Optical Ltd

- Edmund Optics Inc.

- DuPont

- Inrad Optics

- Materion Corporation

- Newport Corporation

- Nippon Sheet Glass Co. Ltd

- Optical Coatings Technologies

- PPG Industries Inc.

- Quantum Coating Inc.

- Reynard Corporation

- SIGMAKOKI CO. LTD

- Schott AG

- Zeiss International

- Zygo

第7章 市場機会と今後の動向

- 電気自動車による今後の需要

目次

Product Code: 55454

The Optical Coatings Market size is estimated at USD 9.47 billion in 2025, and is expected to reach USD 13.36 billion by 2030, at a CAGR of 7.12% during the forecast period (2025-2030).

Key Highlights

- Over the short term, increasing demand for optical coatings from the solar industry and technological advancements in the optical coatings process are expected to drive the market.

- High costs and some limiting properties of optical coatings are expected to hinder the market's growth.

- The upcoming demand for electric vehicles is likely to create opportunities for the market in the coming years.

- Asia-Pacific is expected to dominate the market and is likely to witness the highest CAGR during the forecast period.

Optical Coatings Market Trends

The Electronics and Semiconductors Segment is Expected to Dominate the Market

- Optical coatings play a pivotal role in electronic applications, ensuring light seamlessly passes through optical surfaces. With the surging demand for cutting-edge electronic devices such as smartphones, tablets, and wearables, the appetite for premium optical coatings has surged. These coatings not only bolster the performance of electronic displays but also enhance their durability.

- Transparent conductive coatings find their place in electronic displays as well. The market in focus is buoyed by the relentless growth in demand for consumer electronics. As devices shrink in size and become more compact, the need for adept optical coatings grows. These coatings adeptly manage heat, mitigate glare, and elevate the optical clarity of smaller components.

- The semiconductor industry prioritizes precise, high-performance optical coatings. Integral to photolithography-a cornerstone of semiconductor fabrication-these coatings amplify the efficiency and quality of semiconductor devices. With the rising influence of IoT across diverse sectors, semiconductor demand has surged, subsequently propelling the optical coatings market.

- For instance, data from the Japan Electronics and Information Technology Industries Association (JEITA) highlighted that in 2023, Japan's electronics sector achieved a production value nearing JPY 10.7 trillion Japanese (~USD 76 billion). Encompassing consumer electronics, industrial equipment, and myriad electronic components, the industry is projected to touch USD 3.68 trillion by 2024, marking a commendable 9% Y-o-Y growth.

- World Semiconductor Trade Statistics reported on December 31, 2023, that the global semiconductor market was valued at USD 526.89 billion in 2023, with a promising 16.0% growth anticipated in 2024.

- Data from ZVEI in July 2024 indicates that Germany's electronic and digital sector achieved a turnover of EUR 238 billion (USD 259.28 billion) in 2023, reflecting a robust 10% growth from the previous year.

- Given these dynamics, the market is poised for significant movements in the foreseeable future.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is likely to lead the optical coatings market during the forecast period. Leading countries such as China, Japan, India, and South Korea are showcasing a surge in demand for optical coatings across various sectors, including electronics, semiconductors, aerospace, and defense.

- Data from the Civil Aviation Administration of China (CAAC) on July 12, 2024, revealed that passenger traffic in the first half of 2024 exceeded USD 350 million, marking a 23.5% Y-o-Y increase and a 9% rise from the same period in 2019.

- Furthermore, a report by Aviation A2Z in December 2023 highlighted that China would acquire 17 domestically manufactured aircraft (COMAC), with deliveries scheduled over the next two years, further bolstering the demand for optical coatings.

- As per the India Brand Equity Foundation (IBEF), India ranks fourth globally in renewable energy, wind power, and solar power capacity in 2024. The Annual 2023 India Solar Market Update noted that by the end of December 2023, India's cumulative solar capacity reached approximately 135 GW, with projections of hitting around 170 GW by March 2025.

- IBEF also highlighted that bolstered by government support and favorable economics, the renewable sector has become a magnet for investors. With an eye on self-sufficiency, India aims to meet its energy demand, which is projected to hit 15,820 TWh by 2040.

- The Japan Electronics and Information Technology Industries Association (JEITA) reported that in 2023, electronic components and devices contributed approximately JPY 6.97 trillion (USD 47 billion) to the nation's electronics industry, which boasted a total production value of around JPY 10.7 trillion (USD 76 billion).

- Given these dynamics, the optical coatings market in Asia-Pacific is set for steady growth during the forecast period.

Optical Coatings Industry Overview

The optical coatings market is highly fragmented in nature. Some of the key players in the market (not in any particular order) include DuPont, Zeiss International, Newport Corporation, PPG Industries Inc., and Nippon Sheet Glass Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Solar Industry

- 4.1.2 Technological Advancements in the Optical Coatings Process

- 4.2 Restraints

- 4.2.1 High Costs and Some Limiting Properties of Optical Coatings

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Product Type

- 5.1.1 Optical Filter Coatings

- 5.1.2 Anti-reflective Coatings

- 5.1.3 Transparent Conductive Coatings

- 5.1.4 Mirror Coatings (High Reflective)

- 5.1.5 Beam Splitter Coatings

- 5.1.6 Other Product Types (Temperature Management Coatings)

- 5.2 By Technology

- 5.2.1 Chemical Vapor Deposition

- 5.2.2 Ion-beam Sputtering

- 5.2.3 Plasma Sputtering

- 5.2.4 Atomic Layer Deposition

- 5.2.5 Sub-wavelength Structured Surfaces

- 5.3 By End-user Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Electronics and Semiconductors

- 5.3.3 Telecommunications

- 5.3.4 Healthcare

- 5.3.5 Solar

- 5.3.6 Automotive

- 5.3.7 Other End-user Industries (Military and Defense and Medical)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Qatar

- 5.4.5.4 United Arab Emirates

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Abrisa Technologies

- 6.4.3 AccuCoat inc.

- 6.4.4 Artemis Optical Ltd

- 6.4.5 Edmund Optics Inc.

- 6.4.6 DuPont

- 6.4.7 Inrad Optics

- 6.4.8 Materion Corporation

- 6.4.9 Newport Corporation

- 6.4.10 Nippon Sheet Glass Co. Ltd

- 6.4.11 Optical Coatings Technologies

- 6.4.12 PPG Industries Inc.

- 6.4.13 Quantum Coating Inc.

- 6.4.14 Reynard Corporation

- 6.4.15 SIGMAKOKI CO. LTD

- 6.4.16 Schott AG

- 6.4.17 Zeiss International

- 6.4.18 Zygo

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Upcoming Demand from Electric Vehicles

光学コーティング-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日