|

市場調査レポート

商品コード

1907270

北米のポリ塩化ビニル(PVC):市場シェア分析、業界動向、統計、成長予測(2026年~2031年)North America Polyvinyl Chloride (PVC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のポリ塩化ビニル(PVC):市場シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

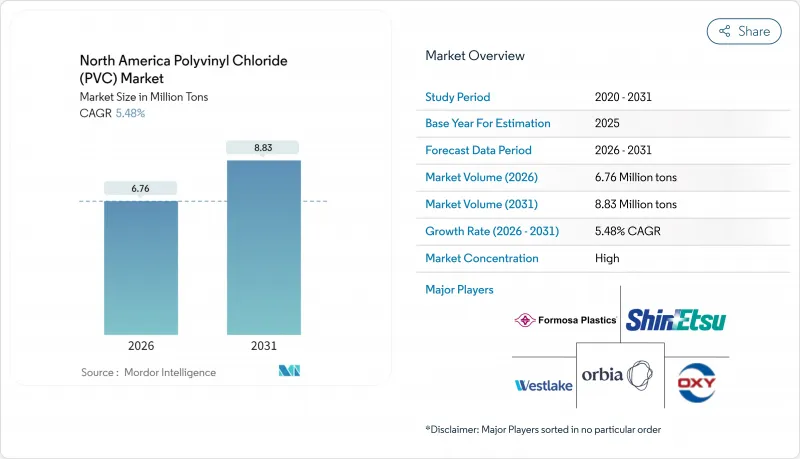

北米のポリ塩化ビニル(PVC)市場は、2025年の641万トンから2026年には676万トンへ成長し、2026年から2031年にかけてCAGR5.48%で推移し、2031年までに883万トンに達すると予測されています。

インフラの近代化が継続していること、特に連邦政府資金による鉛製給水管の交換事業が、サプライチェーンの変動が続く中でもこの拡大を支えています。自治体は鉛製配管の全面交換を10年以内に完了させる義務があるため、需要の見通しは堅調であり、配管購入は広範な経済変動の影響を受けにくい状況です。地域別では米国が最大のPVC消費国であり、原料価格の急騰から生産者を保護する有利なエタンコストがこれを支えています。医療分野は、人口動態の動向とフタル酸フリー医療機器への移行を背景に、最も成長が著しいエンドユーザーとして重要性を増しています。競争の激化は、垂直統合、特殊コンパウンディング、持続可能性の革新に焦点が当てられており、これらは世界的に供給過剰状態にある樹脂市場において利益率を守る役割を果たしています。

北米のポリ塩化ビニル(PVC)市場の動向と洞察

建築・建設分野における需要増加

建設分野におけるPVC消費量は公共事業支出の回復に連動しており、配管・継手用途が全用途のほぼ半数を占めます。連邦規則による延期禁止のため、州・地方自治体では老朽化した配管網の更新が進められています。鉛含有量を規制する建築基準により、プロジェクトは硬質ビニルシステムへ移行する一方、生産者は統合エチレンチェーンを活用してコスト安定化を図っています。長期インフラ計画は予測可能な受注基盤を創出し、民間住宅サイクルに左右されず、国内工場の設備増強を促進し樹脂需要を持続させています。

医療用機器・輸液バッグ分野での急増

医療分野の需要はCAGR6.34%で拡大しており、病院では血液バッグ、チューブ、カテーテルに非DEHP化合物を指定しています。材料配合メーカーは現在、透明性、柔軟性、滅菌耐性を損なうことなくFDA試験を通過するフタル酸エステルフリー添加剤を提供しています。規制障壁の高まりとバリデーションコストの増加は、確立されたサプライヤーに有利に働き、北米のポリ塩化ビニル市場における商品マージンの圧力を相殺するプレミアム価格設定を可能にしております。高齢化と在宅医療の拡大が、この需要の成長余地をさらに拡大しております。

塩化ビニルモノマー及びエチレン価格の変動性

原料コストが製造原価の最大70%を占めるため、原料価格の変動はマージンを圧迫します。最近の鉄道事故は物流リスクを浮き彫りにし、主要クラッカーの計画停止は地域的な供給逼迫を招き、スポット市場の変動性を増幅させています。統合企業は優位なエタン供給により影響の一部を緩和できますが、商社バイヤーはより急激な価格高騰に直面し、北米塩化ビニル市場全体の在庫計画を複雑化させています。

セグメント分析

2025年における総生産量の59.65%を硬質塩化ビニルが占め、寿命とコスト安定性が重視される地下水道インフラ分野での強みを示しました。このシェアは北米塩化ビニル市場規模における最大の割合に相当し、連邦政府資金プロジェクトで義務付けられたパイプ需要が基盤となっています。硬質配合は窓枠やサイディングにも使用され、公共事業以外でも安定した需要を生み出しています。

軟質カテゴリーは、医療機器、ホース、電線被覆材における特殊化合物の採用により、CAGR5.82%で拡大しています。メーカーは透明性、低温柔軟性、フタル酸フリー化学組成で差別化を図っています。塩素化PVCは給湯管でニッチ市場を維持し、低発煙グレードは交通機関や高占有率ビルにおける防火安全基準に対応しています。製品構成は高利益率を実現し、世界の商品サイクルへの依存度を低減する特殊グレードへ継続的に移行しています。

北米のポリ塩化ビニル(PVC)市場レポートは、製品タイプ(硬質PVC、軟質PVC、低煙PVC、塩素化PVC)、用途(パイプ・継手、フィルム・シートなど)、エンドユーザー産業(建築・建設、電気・電子、医療、自動車など)、地域(米国、カナダ、メキシコ)別に分類されています。市場予測は数量(トン)単位で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 建築・建設分野における需要の増加

- 医療機器および点滴バッグにおける使用量の急増

- 水道インフラ更新のための連邦政府資金

- 鉛フリー配管に対する規制面の追い風

- バイオベース可塑剤がプレミアムニッチ市場を開拓

- 市場抑制要因

- 塩化ビニルモノマー及びエチレン価格の変動性

- 環境・健康面での監視強化

- フタル酸系可塑剤に対する規制強化

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 輸出入動向

第5章 市場規模と成長予測(金額ベースおよび数量ベース)

- 製品タイプ別

- 硬質PVC

- 透明硬質PVC

- 非透明硬質PVC

- 軟質PVC

- 透明軟質PVC

- 不透明軟質PVC

- 低煙性ポリ塩化ビニル

- 塩素化ポリ塩化ビニル

- 硬質PVC

- 用途別

- パイプおよび継手

- フィルムおよびシート

- 電線・ケーブル

- ボトル

- プロファイル、ホース及びチューブ

- その他の用途

- エンドユーザー業界別

- 建築・建設

- 電気・電子機器

- ヘルスケア

- 自動車

- 包装

- 履物

- その他のエンドユーザー産業

- 国別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- AMCO International

- Aurora Material Solutions

- Braskem

- Formosa Plastics Corporation

- GEON

- INEOS

- Kem One

- LG Chem

- Lubrizol

- Occidental Petroleum Corporation

- Orbia Polymer Solutions(Vestolit)

- SABIC

- Shin-Etsu Chemical Co., Ltd.

- SIMONA AMERICA

- Teknor Apex

- Westlake Corporation