|

市場調査レポート

商品コード

1686653

タイのペットフード市場:シェア分析、産業動向、成長予測(2025年~2030年)Thailand Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| タイのペットフード市場:シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 282 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

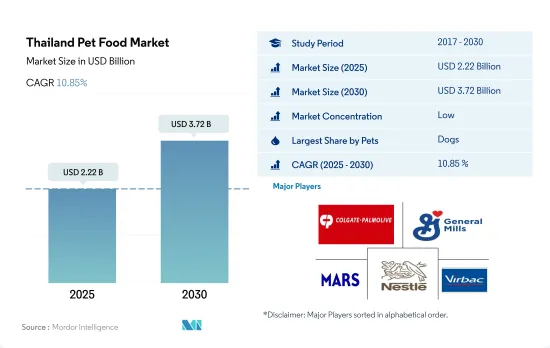

タイのペットフード市場規模は2025年に22億2,000万米ドルと推計され、2030年には37億2,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは10.85%で成長する見込みです。

ペット飼育の増加とプレミアム・ペットフードの需要が同国のペットフード市場を牽引

- タイはアジア太平洋における新興ペットフード市場のひとつです。2022年には地域のペットフード市場の5.5%のシェアを占め、2017年から2022年の間に63.1%成長しました。この成長は、同国のペット飼育の増加、人間化、プレミアム化によるものと考えられます。

- タイのペットフード市場の犬セグメントが最大のシェアを占め、2022年の市場価値は10億3,840万米ドルに達しました。2029年には23億150万米ドルの市場規模に達すると予測されています。このような大きなシェアと成長は、国内で家庭料理から市販のペットフードに移行する飼い主が多いことと、犬の飼育数が多いことに起因していると考えられます。例えば、2022年の同国のペット数に占める犬の割合は44.9%、猫は20.3%です。また、プレミアムドッグフード製品への動向も高まっています。

- 猫はタイのペットフード市場で第2位のシェアを占め、2022年には2億9,560万米ドルを占めました。予測期間中のCAGRは12.1%と推定されます。ペットの飼い主の猫に対する考え方が変化していることと、メンテナンスの必要性が低いことから、2017年から2022年の間にその人口は27.5%増加しました。

- その他のペットには、鳥類、小型哺乳類、げっ歯類、観賞魚が含まれます。これらの動物には特有の栄養要求があり、特殊なペットフード製品で満たす必要があります。そのため、2022年の市場規模は2億7,790万米ドルでした。

- 業務用フードの使用の増加、ペットの人間化の進展、国内のペット数の増加が、予測期間中のペットフード市場をCAGR 11.1%で牽引すると予想されます。

タイのペットフード市場の動向

王室の新築祝いの儀式や雨乞いのパレードにおける猫の文化的重要性から、猫の飼育が増加し、同国における猫の飼育数増加を牽引しています。

- 猫は古来よりタイの文化において重要な位置を占めており、単なるペット以上の存在と考えられています。そのカリスマ的で神秘的なオーラはしばしば幸運をもたらすとされ、王室の新築祝いや雨乞いのパレードなど、多くの縁起の良い伝統行事に欠かせない存在となってきました。その文化的意義から、猫はタイでペットとして飼われる最も人気のある動物のひとつとなっており、2022年にはペット総数の20.3%を占めるまでになりました。

- 文化的意義があるにもかかわらず、タイにおける猫の飼い主の数は犬の飼い主の数を下回っています。2022年には、猫のペット数は犬のペット数より121.2%少なくなりました。しかし、猫を飼う世帯の割合は増加しており、2017年の10.4%から2021年には11.1%に上昇しています。この動向は、狭いスペースへの適応性やユニークな性格など、猫の魅力的な特性に起因していると考えられます。

- タイにおけるペットの猫の飼育数は着実に増加しており、2019年から2022年にかけては18.1%増加しているが、これは主にCOVID-19パンデミック時のコンパニオンのニーズによるものです。猫の平均寿命は20年以上であるため、パンデミックの影響は5~10年間は見られると予想されます。Z世代、Y世代、高齢者層がペットを好むようになり、ペットの人間化の動向は国内でますます広まっています。また、賃貸住宅を借りている人の約35.0%が、ペットの飼育に適した新居に転居しています。これらの要因は、予測期間中のペット猫の飼育数増加に寄与すると思われます。

プレミアム化が進み、プレミアムで高品質なペットフード製品への需要が高まっていることが、タイでのペット支出を促進しています。

- タイのペットオーナーはペットへの支出を大幅に増やしています。同国におけるペットフード支出は2019年から2022年にかけて約16.9%成長したが、これは主にペットが最愛の家族、あるいは子供とみなされるペット飼育へのシフトによるものです。このような認識の変化が、プレミアムペットフード製品に対する需要の増加に寄与しています。

- プレミアム・ペットフードの需要増加を促す要因としては、ペットの人間化、ペットの健康に対する飼い主の意識の高まり、COVID-19パンデミックの影響などが挙げられます。こうした要因から、安全性や健康上の懸念に対応した特定の栄養やペットフードの需要が急増しています。同国におけるプレミアムドライドッグフードの売上高は2017年の9,400万米ドルから2021年には1億3,040万米ドルに増加し、プレミアムドライキャットフードの売上高は2017年の4,360万米ドルから2021年には7,490万米ドルに増加しました。同国で販売されている主なプレミアムブランドには、Royal Canine、Whiskas、Me-oなどがあります。

- このような特殊なペットフードへの需要の増加により、特にプレミアムとスーパープレミアムセグメントでは平均単価が上昇しました。2022年には、ペットの飼い主がペットフード製品に費やす金額が最も高く(年間596.1米ドル)、動物用食事に費やす金額は年間平均148.4米ドルでした。2022年、タイにおけるペットフードの売上は、店舗型小売が91.5%と大半を占めています。残りの売上はeコマースによるもので、市場シェアは8.5%であり、オンライン小売は大流行期に成長を遂げました。ペットフードのプレミアム化や、高品質なペットフードの利点に対する意識の高まりは、今後も同国のペット支出を促進すると予想されます。

タイのペットフード業界の概要

タイのペットフード市場は断片化されており、上位5社で26.45%を占めています。この市場の主要企業は以下の通り。 Colgate-Palmolive Company(Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle(Purina)and Virbac(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他のペット

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブプロダクト別

- ドライペットフード

- サブ製品別ドライペットフード

- キブル

- その他のドライフード

- ウェット・ペットフード

- ペット用栄養補助食品・サプリメント

- サブプロダクト別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用おやつ

- サブプロダクト別

- カリカリおやつ

- デンタル・トリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のおやつ

- ペット用動物飼料

- サブプロダクト別

- 糖尿病

- 消化器過敏症用

- オーラルケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンライン・チャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Alltech

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- DoggyMan H. A. Co., Ltd.

- EBOS Group Limited

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- Schell & Kampeter Inc.(Diamond Pet Foods)

- Thai Union Group PCL

- Virbac

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Thailand Pet Food Market size is estimated at 2.22 billion USD in 2025, and is expected to reach 3.72 billion USD by 2030, growing at a CAGR of 10.85% during the forecast period (2025-2030).

Increasing pet adoption and the demand for premium pet foods are driving the pet food market in the country

- Thailand is one of the emerging pet food markets in Asia-Pacific. It accounted for a 5.5% share of the region's pet food market in 2022, which grew by 63.1% between 2017 and 2022. This growth can be due to the country's increasing pet ownership, humanization, and premiumization.

- The dogs segment of the Thai pet food market held the largest share, reaching a market value of USD 1,038.4 million in 2022. It is anticipated to reach a market value of USD 2,301.5 million in 2029. This significant share and growth can be due to a high number of pet owners in the country shifting from home-cooked food to commercial pet food and a higher dog population. For instance, dogs accounted for 44.9% of the country's pet population in 2022, while cats accounted for 20.3%. There is also a growing trend toward premium dog food products.

- Cats held the second-largest share of the Thai pet food market, accounting for USD 295.6 million in 2022. They are estimated to record a CAGR of 12.1% during the forecast period. Their population grew by 27.5% between 2017 and 2022 due to changing attitudes toward cats among pet owners and their low maintenance requirements.

- The other pets include birds, small mammals, rodents, and ornamental fish. These animals have unique nutritional requirements that need to be fulfilled through specialized pet food products. Therefore, in 2022, they accounted for a market value of USD 277.9 million.

- The increasing usage of commercial foods, the rising pet humanization, and the growing population of pets in the country are anticipated to drive the pet food market during the forecast period, with a CAGR of 11.1%.

Thailand Pet Food Market Trends

Increasing adoption of cats due to their cultural significance in the royal housewarming ceremony and the rain-making parade is driving the growth of the cat population in the country

- Cats have held a significant place in Thai culture since ancient times, and they are considered more than just pets. Their charismatic and mysterious aura is often associated with bringing good fortune, and they have been an essential component of many auspicious traditions, including the royal housewarming ceremony and the rain-making parade. Due to their cultural significance, cats have become one of the most popular animals kept as pets in Thailand, making up 20.3% of the total pet population in 2022.

- Despite cultural significance, the number of cat owners in Thailand is lower than the number of dog owners. In 2022, the pet cat population was 121.2% smaller than pet dogs. However, there has been an increase in the proportion of households owning cats, rising from 10.4% in 2017 to 11.1% in 2021. This trend can be attributed to the appealing characteristics of cats, including their adaptability to small spaces and unique personalities.

- The pet cat population in Thailand has been steadily increasing, with a rise of 18.1% between 2019 and 2022, mainly due to the need for companionship during the COVID-19 pandemic. The effect of the pandemic is anticipated to be witnessed for 5-10 years, as the average lifespan of cats is more than 20 years. The trend of pet humanization is becoming increasingly prevalent in the country as Gen Z, Gen Y, and the elderly populations prefer pets. About 35.0% of individuals who rent homes have relocated to a new residence more suitable for their pets. These factors are likely to contribute to an increase in the population of pet cats during the forecast period.

Premiumization, with the growing demand for premium high-quality pet food products, is driving pet expenditure in the country

- Pet owners in Thailand are significantly increasing their expenditure on pets. The pet food expenditure in the country grew by about 16.9% between 2019 and 2022, primarily due to a shift in pet ownership toward pet parenting, where pets are considered beloved family members or even children. This changing perception is contributing to the increased demand for premium pet food products.

- The factors driving the heightened demand for premium pet food include the humanization of pets, growing awareness among pet owners about their pets' well-being, and the impact of the COVID-19 pandemic. These factors have led to a surge in demand for specific nutrition and pet food that addresses safety and health concerns. Premium dry dog food sales in the country increased from USD 94 million in 2017 to USD 130.4 million in 2021, while premium dry cat food sales increased from USD 43.6 million in 2017 to USD 74.9 million in 2021. The major premium brands sold in the country include Royal Canine, Whiskas, and Me-o.

- This increasing demand for specialized pet food increased the average unit price, particularly in the premium and super-premium segments. In 2022, pet owners spent the highest amount (USD 596.1 per year) on pet food products, with an average spending of USD 148.4 per year on veterinary diets. In 2022, store-based retailing accounted for most pet food sales in Thailand, i.e., 91.5%. The remaining sales are through e-commerce, with an 8.5% market share, with online retailing experiencing growth during the pandemic. The premiumization of pet food and growing awareness of high-quality pet food benefits are expected to continue driving pet expenditure in the country.

Thailand Pet Food Industry Overview

The Thailand Pet Food Market is fragmented, with the top five companies occupying 26.45%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and Virbac (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Alltech

- 6.4.2 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.3 DoggyMan H. A. Co., Ltd.

- 6.4.4 EBOS Group Limited

- 6.4.5 General Mills Inc.

- 6.4.6 Mars Incorporated

- 6.4.7 Nestle (Purina)

- 6.4.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.9 Thai Union Group PCL

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms