|

市場調査レポート

商品コード

1686650

インドのHVDCトランスミッション:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)India HVDC Transmission Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのHVDCトランスミッション:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

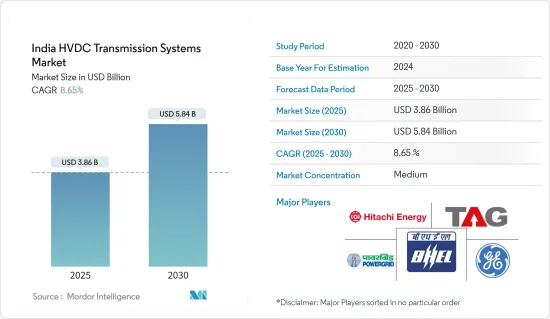

インドのHVDCトランスミッション市場規模は2025年に38億6,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは8.65%で、2030年には58億4,000万米ドルに達すると予測されます。

COVID-19のパンデミックによって、同国の送電に関する中長期計画が変更されることはありません。COVID-19の期間中、電力省によって必須サービスに分類された送電は、国内では通常の事業として継続されました。再生可能エネルギー分野の成長、急速な都市化、農村部の電化の増加といった要因が、予測期間中に市場を牽引すると予想されます。一方、国内における分散型電力システムや遠隔地電力システムの増加は、市場成長の妨げになる可能性が高いです。

主なハイライト

- HVDC架空送電システムは、予測期間中も大きな市場シェアを維持すると見られ、インドHVDC市場の主要セグメントとなっています。

- 同国は2030年までに30GWの洋上風力発電設備を導入する計画であり、洋上環境でより効率的なHVDCトランスミッションシステムにいくつかのビジネスチャンスが生まれると期待されています。

- インドにおけるトランスミッションの拡大は、予測期間中、同国のHVDCトランスミッションシステム市場を牽引すると見られています。

インドのHVDCトランスミッション市場動向

HVDC架空送電システムが市場を独占する見込み

- HVDC架空送電システムは、HVAC送電線に比べて送電線タワーの建設要件がシンプルです。また、HVDC架空送電システムは、送電線1km当たりのコストや送電電力1MV当たりのコストなど、単位当たりのコストが低いです。

- 世界の主要地域では、高圧架空送電は一般的な送電手段です。直流送電は、架空送電ケーブルによる長距離送電の総コストを低減します。

- さらに、高圧架空送電は、地下送電に比べて建設費がはるかに安く、修理も早いです。しかし、人口密度の高い都市部や商業地区での用途は減少しています。

- HVDCトランスミッションのコストは、ターミナル・ステーションのコストと送電線のコストに依存します。しかし、HVACトランスミッションの場合、HVDCに比べて導体が多く、機械的負荷が増加します。負荷の増加により、送電線コストは距離とともに増加します。HVACのコスト増加は送電線100KmあたりHVDCトランスミッション線よりも大きいため、長距離トランスミッションではHVDCがよりコスト効率の高い選択肢となります。

- 既存のHVDCネットワークの容量増強もインドの架空送電網を牽引しています。例えば、2019年から2020年にかけて、3000MVAの容量を追加したJharsuguda(Sundargarh)S/S、Aligarh(PG)765 kV GISなど、複数のプロジェクトでHVDC変電所の展開が見られます。インドでは、既存の変電所の容量が合計で12870MVA増加しており、HVDCベースの変電所が大きなシェアを占めています。

- インドでは現在、大規模なCOVID-19ワクチン接種が行われており、その結果、市場環境が改善しつつあります。このような中、2021年2月19日にPower Gridの320kV 2000MW Pugalur(Tamil Nadu)-Thrissur(Kerala)HVDCプロジェクトが開通しました。5070カロールインドルピーを投じたこのプロジェクトは、Raigarh-Pugalur-Thrissur 6000MW HVDCシステムの一部であり、ThrissurのHVDCステーションを通じて2000MWをケララ州に送電します。2020年9月、インド電力公社(Power Grid Corporation of India Ltd.)は、ライガールHVDCターミナル・ステーション(チャッティースガル州)とプガールHVDCターミナル・ステーションからなるライガール・プガールHVDCトランスミッションのポール1を完成させました。

- このため、予測期間中はHVDC架空送電システムが市場を独占すると予想されます。

トランスミッション送電網の拡大が市場を牽引

- HVDCトランスミッション線では、送電損失は定格電圧に反比例します。さらに、HVDCトランスミッション線はHVAC送電線よりも高い電圧の電流を送ることができます。HVDCトランスミッション線は送電容量が大きいため、土地の有効利用が限られている場所では、HVAC送電線よりもHVDCトランスミッション線の方が好まれます。

- インドは世界で2番目に人口が多いです。人口が多いため、インドでは電力エネルギーとトランスミッション・ネットワークの需要が伸びています。しかし、送電網の規模と複雑さが増すと、負荷フロー、電力振動、電圧品質に関する問題が発生します。そのため、こうした問題を解消するために、インドの中央、州、非公開の各送電会社ではHVDCトランスミッション線を優先的に整備しています。

- 2020年現在、インド国内のトランスミッションの58%以上が400kV以上の定格電圧を持ち、42%が220kVです。

- HVDCトランスミッション網の増加は、電力が余っている州や設備容量の大きい州から電力を輸入することで、いくつかの州が電力需要を満たすのに役立ちました。一国一送電網」計画のもと、5つの地域送電網が相互接続され、地域間で余剰電力を融通し合うようになりました。さらに、電力省の発表によると、2019年度、インドの送配電会社は、主に送配電ロスにより27,000カロールインドルピーの損失を被りました。

- さらに、地域間の電力交流を強化するために、いくつかのHVDCプロジェクトが拡張段階にあります。2022年までにChampa Pool-Kurukshetra HVDC Bipoleを1500MWから2000MWにアップグレードすることも、拡張プロジェクトのひとつです。さらに2020年12月、マハラシュトラ州はパルガール県のアーレイからクドゥスまでの10億米ドルの地下HVDCプロジェクトを発表しました。このプロジェクトは州の提案によるもので、2020年10月にムンバイ首都圏で起こる完全停電などの問題を解決するのに役立ちます。

- したがって、上記の要因に基づき、送電網の拡大が予測期間中のインドHVDCトランスミッションシステム市場を牽引すると予想されます。

インドのHVDCトランスミッション産業概要

インドのHVDCトランスミッション市場は適度に統合されています。主な企業には、日立エネルギー、ゼネラル・エレクトリック、TAGコーポレーション、パワー・グリッド・コーポレーション・オブ・インド、バーラト・ヘビー・エレクトリカルズなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2027年までの市場規模および需要予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- PESTLE分析

第5章 市場セグメンテーション

- トランスミッションタイプ

- HVDC架空送電システム

- HVDC地下・海底トランスミッション

- コンポーネント

- コンバーター・ステーション

- トランスミッション(ケーブル)

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Hitachi Energy Ltd

- Siemens AG

- General Electric Company

- Adani Transmission Ltd

- TAG Corporation

- Power Grid Corporation of India Limited

- Bharat Heavy Electricals Limited

- Tata Projects Limited

第7章 市場機会と今後の動向

The India HVDC Transmission Systems Market size is estimated at USD 3.86 billion in 2025, and is expected to reach USD 5.84 billion by 2030, at a CAGR of 8.65% during the forecast period (2025-2030).

The COVID-19 pandemic did not alter the country's medium- to long-term plans for power transmission. Power transmission, which was categorized as an essential service by the Ministry of Power during the COVID-19 period, continued as an usual business in the country. Factors such as growing renewable energy sector, rapid urbanization, and increasing rural electrification, are expectde to drive the market during the forecast period. On the other hand, the growing distributed and remote power systems in the country is likely to hinder the market growth.

Key Highlights

- The HVDC overhead transmission system is likely to maintain its larger market share during the forecast period, thus making it a dominating segment in the India HVDC market.

- The country's pan to deploy 30 GW of offshore wind energy installations by 2030, is expected to create several opportunities for HVDC transmission systems, which are more efficient for offshore environments.

- The increasing expansion of transmission electrcity grid in India is expected to drive the country's HVDC transmission systems market during the forecast period.

India HVDC Transmission System Market Trends

HVDC Overhead Transmission Systems Expected to Dominate the Market

- HVDC overhead transmission systems have a simpler line tower construction requirement compared to HVAC transmission lines. Also, HVDC overhead transmission systems have lower per-unit costs, including cost per km of line and per MV of transmitted power.

- In major part of the world, high-voltage overhead transmission is a popular means of power transmission. DC decreases the total cost for long-distance power transmission with overhead lines cables.

- Moreover, the high-voltage overhead transmission is much less expensive to build and much quicker to repair than underground transmission. However, it has seen decreasing applications in densely-populated urban and commercial areas.

- The cost of HVDC transmission depends on the terminal station's cost and the cost of the transmission line. But in case of HVAC transmission network there are more conductors in comparison to HVDC, which increases the mechanical load. Due to the increased load the transmission line cost increases with the distance. The cost increase in HVAC is greater than the HVDC line per 100Km of a transmission line, thus making HVDC a more cost efficient option for long transmissions.

- Capacity additions in pe-existing HVDC networks are also driving the overhead transmission network in India. For instance, during 2019-2020, deployment of HVDC substations is witnessed in multiple projects, including Jharsuguda (Sundargarh) S/S with capacity addition of 3000 MVA, Aligarh (PG) 765 kV GIS, and others. In total, the nation increased the capacity of the pre-existing substation by the 12870 MVA, with the HVDC-based substations holding a significant share.

- India is currently witnessing large-scale COVID-19 vaccination, which is resulting in improving market conditions. Amid this, Power Grid's 320 kV 2000 MW Pugalur (Tamil Nadu) - Thrissur (Kerala) HVDC project was inaugurated on 19th February 2021. The project, with cost of INR 5070 crore, is part of the Raigarh-Pugalur-Thrissur 6000 MW HVDC system and enables the transfer of 2000 MW to Kerala through the HVDC station at Thrissur. Earlier in September 2020, Power Grid Corporation of India Ltd. commissioned Pole-1 of the Raigarh Pugalur HVDC Transmission system comprising Raigarh HVDC Terminal Station (Chhattisgarh) & Pugalur HVDC Terminal Station.

- Therefore, owing to the above points, HVDC overhead transmission systems are expected to dominate the market during the forecast period.

Increasing Expansion of Transmission Electrcity Grid expected to Drive the Market

- For HVDC transmission lines, the transmission losses are in inverse relation with the voltage ratings of electricity, i.e., the higher the voltage rating of electricity transmitted, the lower will be the transmission losses. Furthermore, the HVDC transmission lines can transmit higher voltage current than HVAC lines. In places with limited availability of land, HVDC transmission lines are preferred over HVAC, as they have higher power transmission capacity, and hence, can transmit more electricity per unit land usage.

- India has the second-highest population globally. With a high population, demand for electrical energy and transmission network is growing in India. However, the increasing size and complexity of a transmission network create problems related to load flow, power oscillation, and voltage quality. Thus, to eliminate the issues, HVDC transmission lines are prioritized by various central, state and private power transmission companies in India.

- As of 2020, more than 58% of the transmission lines in the country have voltage ratings of above 400 kV while 42% were 220 kV.

- The growth in HVDC transmission networks helped several states to meet the electricity demand, by importing electricity from states with surplus electricity or high installed capacity. Under the One Nation-One Grid plan, the five regional grids were interconnected to exchange surplus electricity among the regions. Moreover, as per the Ministry of power, in FY 2019, power transmission and distribution companies in India suffered a loss of INR 27,000 crore, primarily due to transmission and distribution losses.

- Further to enhance the interregional electricity exchange, a few HVDC projects are in expansion phases. Upgradation of Champa Pool- Kurukshetra HVDC Bipole from 1500 MW to 2000 MW by 2022 is one among the expansion projects. Additionally, in December 2020, Maharashtra unveiled USD one billion underground HVDC project from Aarey to Kudus in Palghar District. The project is under the proposed state and will help to solve an issue like a complete blackout in the Mumbai Metropolitan Region in October 2020.

- Therefore, based on the above-mentioned factors, increasing expansion of transmission electricity grid is expected to drive the India HVDC transmission systems market during the forecast period.

India HVDC Transmission System Industry Overview

The India HVDC transmission systems market is moderately consolidated. Some of the major companies include Hitachi Energy Ltd, General Electric Company, TAG Corporation, Power Grid Corporation of India Limited, and Bharat Heavy Electricals Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 PESTLE ANALYSIS

5 MARKET SEGMENTATION

- 5.1 Transmission Type

- 5.1.1 HVDC Overhead Transmission System

- 5.1.2 HVDC Underground & Submarine Transmission System

- 5.2 Component

- 5.2.1 Converter Stations

- 5.2.2 Transmission Medium (Cables)

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Hitachi Energy Ltd

- 6.3.2 Siemens AG

- 6.3.3 General Electric Company

- 6.3.4 Adani Transmission Ltd

- 6.3.5 TAG Corporation

- 6.3.6 Power Grid Corporation of India Limited

- 6.3.7 Bharat Heavy Electricals Limited

- 6.3.8 Tata Projects Limited