|

市場調査レポート

商品コード

1851445

ウッドコーティング:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Wood Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ウッドコーティング:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月01日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

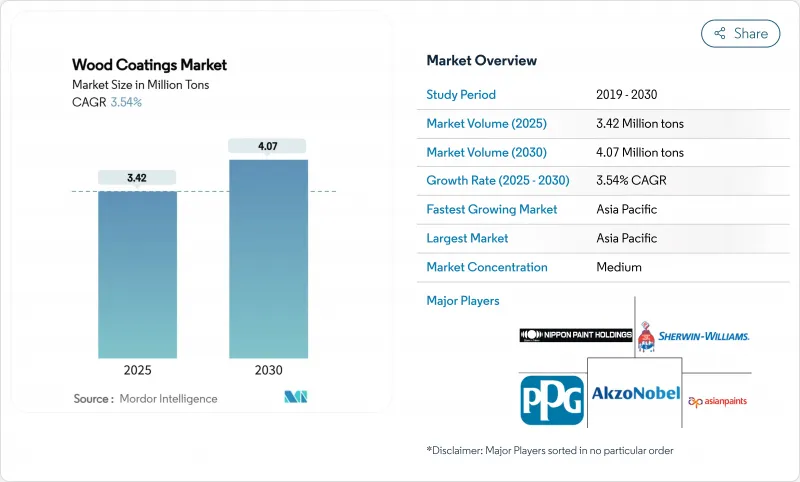

ウッドコーティング市場規模は2025年に342万トンと推計され、予測期間(2025-2030年)のCAGRは3.54%で、2030年には407万トンに達すると予測されます。

この着実な拡大は、アジア太平洋の製造基盤、水性化学物質へのシフトの加速、世界の家具セクターからの持続的な需要に支えられています。ポリウレタンはその耐久性により主要な樹脂プラットフォームであり続ける一方、環境規制により低VOC代替品の採用が急速に進んでいます。メーカーはまた、配合の柔軟性と現地調達に投資することで、原料価格の変動(特に二酸化チタン)を乗り切っています。トップサプライヤー間の統合は、バイオベース添加剤における中堅層の技術革新の高まりと相まって、競争を強化すると同時に、中小企業が適合させなければならない性能の基準値を引き上げています。

世界のウッドコーティング市場の動向と洞察

アジア太平洋地域におけるモジュラー家具とRTA家具のブーム

急速な都市化とアパート面積の縮小により、中国、インド、インドネシアではモジュール式家具と組み立て式家具の急増に拍車がかかっています。これらの大量生産家具は、傷に強く、硬化が早い仕上げ材を必要とし、配合者はMDFのような人工基材への浸透を最適化する必要に迫られています。インドネシアの工場だけで、2024年10月までに100万4,000トンの塗料が生産され、ウッドコーティングはその7%を占めています。速乾性ポリウレタンーアクリルハイブリッドで対応するサプライヤーは新規契約を獲得しており、アジア太平洋地域がウッドコーティング市場で中心的な役割を果たしています。

EU主導の低VOC水性処方へのシフト

欧州連合(EU)のVOC規制強化により、溶剤系からの移行が加速しています。最近の水性ポリウレタン・ディスパージョンの耐久性は溶剤系に匹敵するようになり、歴史的な性能差は解消されました。これらの適合製品を北米やアジアに輸出している欧州のフォーミュレーターは、単一のレシピでグローバルな生産ラインを稼働させることでコストシナジーを実現し、他地域が同様の規則を目指す中で先行者利益を得ています。このような連携は、ウッドコーティング市場の主要な構造的促進要因であり、排出量をさらに削減するバイオベースのコバインダーに焦点を当てた研究開発を刺激しています。

樹脂と溶剤の価格変動

EUに流入する中国製酸化チタンに対する11.4%~32.3%の反ダンピング関税(2025年1月発効)により、原材料コストは急上昇しています。ウッドコーティング市場の小規模メーカーはマージンの圧縮に直面し、一部のメーカーは顔料の量を減らしたり、代替のエクステンダーを使用して再製造を行う一方、多国籍企業は長期供給契約を通じてエクスポージャーをヘッジしています。

セグメント分析

2024年のウッドコーティング市場のシェアはポリウレタンが60%を占め、2030年までのCAGRは3.79%になると予想されます。ポリウレタンの架橋密度は、家具輸出業者が厳しい耐久性試験をクリアするために要求する耐薬品性を実現します。ポリウレタンは2024年時点ですでに樹脂のウッドコーティング市場規模の最大部分を占めており、硬度を犠牲にすることなく化石含有量を削減するバイオポリオールグレードの導入でリードを広げ続けています。アクリル樹脂はUV安定性により依然として外装用樹脂の主力であり、ニトロセルロースは安全規制の緩い地域では依然としてクラシック家具に使用されています。Solusに対応したバイオベースシステムは、より安全なドロップインオプションへとバイヤーを誘導しています。ポリエステルは、ピアノやブティック・キャビネット用の高光沢仕上げにニッチな地位を占めており、その特殊な位置づけを物語っています。新興のリグニン系バインダーは、持続可能性主導の試験的プロジェクトを取り込む態勢にあるが、現在の総需要の1%未満にとどまっています。そのため、ポリウレタンの確固たる地位は、ウッドコーティング市場に参入しているすべての主要メーカーの競合配合ロードマップを支えています。

湿気硬化型脂肪族ポリウレタンの進歩により、VOC含有量は50g/L未満となり、オープンタイムを犠牲にすることなく従来の仕様を上回るようになりました。ベトナムとポーランドの大手OEM家具メーカーは、フラットラインスプレーと真空コーターでこれらのシステムを検証しており、ポリウレタンが今後もプレミアム性能層を形成し続けることを示しています。</p><h3><u>Geography Analysis</u></h3><p>アジア太平洋は2024年に57%のシェアでウッドコーティング市場を独占し、最も早い地域CAGR 3.9%を記録しました。中国は、国内消費と輸出志向の家具クラスターに支えられ、依然として基軸である一方、インドでは中産階級が台頭し、現地のプレミアムセグメントを牽引しています。アジア太平洋地域は、各国政府が排出規制を強化するにつれて、水を媒体とする製品の採用が加速しており、規模主導の技術革新にとって極めて重要な舞台となっています。

北米はウッドコーティング市場で大きなシェアを占め、技術のアップグレードでリードしています。DIYへの参加と高級装飾品のフォーマットが購買パターンを形成し、大型小売店のプライベート・ラベル・プログラムが第三者の持続可能性認証を要求するようになっています。HIRIは、2025年の住宅設備投資は3.9%回復すると予測しており、短期サイクルの需要回復力を強化しています。また、気候変動により、サイディング下地全体の湿度変化に対応する柔軟な膜を持つ外壁用ステインへの需要が高まっており、この地域のウッドコーティング市場のSKU数はさらに多様化しています。

欧州では、厳しい規制と建築用木材の採用が組み合わされています。EUのグリーン・ディール奨励策は低炭素建材を優遇し、集合住宅のCLT部材を保護する高性能コーティングの需要を促進しています。ホルムアルデヒドとVOCの閾値の施行により、2022年以降、地域の家具仕上げラインの半分近くが水性またはUV硬化型の化学薬品に移行し、他のどの地域よりも早く溶剤型ベースが圧縮されました。こうした力学により、欧州は規制のベンチマークであると同時に、発展途上市場向けの配合技術の輸出拠点でもあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- アジア太平洋におけるモジュラー家具とRTA家具のブーム

- EU主導の低VOC水性配合へのシフト

- 北米におけるプレミアムインテリアデコの動向

- DIYホームセンターの拡大

- 欧州における木造多世帯住宅

- 市場抑制要因

- 樹脂と溶剤の価格変動

- ホルムアルデヒド/VOC規制の強化

- 家具におけるラミネートとプラスチックによる代替

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 樹脂タイプ別

- ポリウレタン

- アクリル

- ニトロセルロース

- ポリエステル

- その他

- 技術別

- 水系

- 溶剤系

- UV硬化型

- パウダーコーティング

- 用途別

- 家具および備品

- ドアと窓

- キャビネット

- その他の用途(床、デッキ、成形品を含む)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ナイジェリア

- エジプト

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Akzo Nobel N.V.

- Asian Paints

- Axalta Coating Systems

- Benjamin Moore & Co.

- Ceramic Industrial Coatings

- Hempel A/S

- Jotun

- Kansai Nerolac Paints Limited

- KAPCI Coating

- MAS Paints

- National Paints Factories Co. Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- Ritver

- RPM International Inc.

- Teknos Group

- The Sherwin-Williams Company