|

市場調査レポート

商品コード

1686611

原子炉廃止措置:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Nuclear Power Reactor Decommissioning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 原子炉廃止措置:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

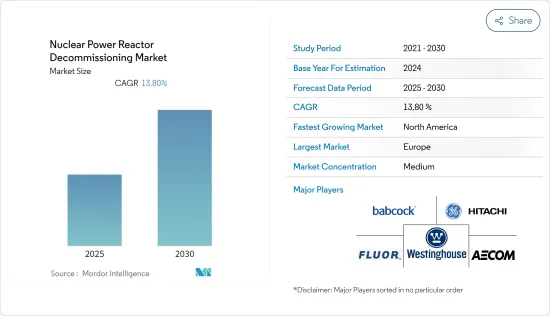

原子炉廃止措置市場は予測期間中に13.8%のCAGRで推移すると予測されます。

この市場は、2020年のCOVID-19パンデミックによって中程度の影響を受けたが、回復しつつあり、パンデミック前のレベルに達しています。

市場の成長を促す主な要因は、運転定年を迎える原子炉の増加、再生可能電源(i.e.風力や太陽光)の価格低下、環境問題への感度の高まりです。

しかし、政府の好意的な政策による原子力発電所の寿命延長は、市場成長の妨げになると予想されます。

ドイツ、英国、韓国など数ヵ国における脱原発政策は、廃炉市場を発展させるために必要な専門知識を国のニーズに合わせて提供する国内外の企業に機会をもたらすと予想されます。

北米は、原子力発電炉の廃止措置において最も急成長している市場になると予想され、米国はこの地域における重要な廃止措置ホットスポットのひとつです。

原子炉廃止措置市場の動向

商業炉セグメントが市場を独占する見込み

2022年10月現在、32カ国で437基の商業用原子力発電所が稼働しています。米国は最大の原子力発電能力を有し、他のどの国よりも原子力発電量が多いです。フランスは原子力発電容量が2番目に大きく、原子力発電量も2番目に多いです。

商業用原子力発電所の停止と廃炉には、経済的要因、規制的要因、社会的要因など、いくつかの要因が絡んでいます。運転寿命の終了や、太陽光や風力といった代替エネルギー発電源のコスト低下といった一次情報が、原子力エネルギーのコスト競合力を低下させました。2011年の福島原発事故後、世界中で原子力の安全プロトコルがアップグレードされ、インフラのアップグレードや運転・保守コストの増加に伴う追加コストが発生しました。このため、多くの古い商業用原子炉の運転者は、運転寿命が40年で、インフラのアップグレードによってさらに20年延長できる古い原子炉を廃炉にすることを選択しています。

世界各国の政府による政策レベルの取り組みも、原子力発電所の閉鎖につながっています。多くの国の政府が、自国のエネルギーミックスにおける原子力の削減を計画しました。このような規制政策は、再生可能エネルギーが充実しており、商業用原子力発電所を運転することによる環境への影響や潜在的なリスクについて深刻な懸念を抱いている西欧諸国に広く見られます。

ドイツは国策として、2022年末までにすべての原子炉を停止する予定です。2017年、スイスは国内からの原子力発電所の段階的廃止を決議しました。2020年9月、ベルギー政府は2025年までに段階的に原発を廃止することを再確認する協定に署名しました。スペインは、稼働中の商業用原子炉7基のうち4基を2030年までに閉鎖し、残りの3基を今後5年以内に閉鎖し、2035年までに原子力発電を完全に廃止すると宣言しました。

再生可能エネルギー技術の開発と経済性の向上により、原子力発電は大規模な発展を遂げています。世界中の国々が再生可能エネルギーに関連する巨大なインフラを構築しており、それが原子炉の必要性を相殺しています。原子力発電は再生可能エネルギー発電に取って代わられつつあり、それが原子炉の閉鎖につながっています。したがって、再生可能エネルギー源の開発の急増は、世界の原子炉廃止措置市場にとって大きな後押しとなっています。

したがって、前述の要因から、予測期間中は商業用原子炉が調査対象市場を独占すると予想されます。

北米が大きな成長を遂げる見込み

北米は、世界で運転可能な原子炉の数が最も多い地域のひとつです。原子炉廃止措置市場は、米国、カナダ、メキシコからの需要により大きな成長が見込まれています。

米国は最大級の原子力発電国であり、2021年には世界の原子力発電量の30%を占める。同国の原子炉は2021年に778.15TWhの電力を生産し、2020年から1.48%の微減となりました。

2022年8月現在、米国では30の州で合計94.7GWeの容量を持つ92基の原子炉が稼働しており、30社の電力会社によって使用されています。2基の原子炉が建設中で、合計容量は223万kWeです。

米国では原子力の時代が終わりつつあり、原子力発電所の廃炉は重要な産業となっています。非公開会社がこれらの原発を買収し、ライセンス、賠償責任、廃炉資金、廃棄物契約を引き継いでいます。合計容量1997万kWの約41基の原子炉が停止し、最新のものは2022年5月に停止したミシガン州のパリセーズ原発です。2021年12月、ホルテックインターナショナルは、ミシガン州コバートにあるパリセーズ原発を取得し、廃炉・解体するための認可を原子力規制委員会から受けました。2030年までに約198基の原子炉が停止すると予想されています。

米国の原子炉は老朽化しています。米国原子力規制委員会(NRC)は、後続ライセンス更新(SLR)プログラムにより、60年から80年を超えて運転ライセンスを延長する申請を検討しています。しかし、最近、45~50年での早期引退を選択した原発所有者もいます。

低コストのシェールガスを利用した発電との激しい競合が、国内の原子力産業の競争力を傷つけた。記録的な低い卸電力価格と、高コストの延命(PLEX)アップグレードが相まって、原子力発電所の早期引退に追い打ちをかけた。

長年にわたり、カナダは原子力の研究と技術におけるリーダーであり、カナダで開発された原子炉システムを輸出してきました。2021年、カナダの原子力発電所による発電量は92.6TWhで、総発電量の約15%を占めました。オンタリオ州では、運転可能な原子炉19基(合計容量13,624MW)および原子炉6基(合計容量214万kW)が2022年8月に停止しました。

2022年8月現在、カナダには使用されなくなり停止したさまざまな研究用原子炉や原型炉があります。これらの原子炉は安全な保管状態にあり、最終的な廃炉を待っています。これらの原子炉には、WR-1、チョークリバー研究所(CRL)のNRX原子炉、CRLのMAPLE-1およびMAPLE-2(多目的応用物理格子実験)原子炉、QC州ベカンクールのジェンティリー1原子力発電所、ON州ロルフトンの原子力発電実証(NPD)原子炉、ON州キンカーダインのダグラス・ポイント原子力発電所などがあります。これらは予測期間中、カナダの原子炉廃止措置市場の需要を牽引すると予想されます。

したがって、北米は予測期間中に原子炉廃止措置市場で大きな成長を示すことが期待されています。

原子炉廃止措置業界の概要

原子炉廃止措置市場は適度に断片化されています。同市場の主要企業(順不同)には、Babcock International Group PLC、Fluor Corporation、GE日立ニュークリア・サービス、AECOM、Westinghouse Electric Companyなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 調査の前提条件

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2027年までの市場規模および需要予測

- 原子力発電量の予測

- 最近の動向と開発

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 原子炉タイプ別

- 加圧水型原子炉

- 加圧水型重水炉

- 沸騰水型原子炉

- 高温ガス炉

- 液体金属高速増殖炉

- その他の原子炉

- 用途別

- 商業用動力炉

- 試作炉

- 研究炉

- 容量別

- 100MW以下

- 100-1000 MW

- 1000MW以上

- 地域別

- 北米

- アジア太平洋

- 欧州

- 南米

- 中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Babcock International Group PLC

- James Fisher & Sons PLC

- NorthStar Group Services Inc.

- Fluor Corporation

- GE Hitachi Nuclear Services

- Studsvik AB

- Enercon Services Inc.

- Orano Group

- Aecom

- Bechtel Group Inc.

- Westinghouse Electric Company

第7章 市場機会と今後の動向

The Nuclear Power Reactor Decommissioning Market is expected to register a CAGR of 13.8% during the forecast period.

Although the market studied was moderately impacted by the COVID-19 pandemic in 2020, it has been recovering and reached pre-pandemic levels.

The major factors driving the market's growth are the increasing number of nuclear reactors reaching operational retirement, declining prices of renewable power generation sources (i.e., wind and solar), and growing sensitivity toward environmental issues.

However, the lifetime extension of nuclear power plants with favorable government policies is expected to hinder the market's growth.

Nuclear phase-out policies in several countries, such as Germany, the United Kingdom, and South Korea, are expected to create opportunities for foreign and domestic players to provide the necessary expertise for the country's needs to develop their decommissioning market.

North America is expected to be the fastest-growing market for nuclear power reactor decommissioning, with the United States being one of the significant decommissioning hotspots in the region.

Nuclear Power Reactor Decommissioning Market Trends

Commercial Reactors Segment is Expected to Dominate the Market

As of October 2022, 437 commercial nuclear power plants were in operation across 32 countries. The United States had the largest nuclear electricity generation capacity and generated more nuclear electricity than any other country. France has the second-largest nuclear electricity generation capacity and second-highest nuclear electricity generation.

Several factors are responsible for the shutdown and decommissioning of commercial nuclear power plants, including economic, regulatory, and social factors. Some primary factors, such as the end of operational life and the fall in the cost of alternative energy generation sources, like solar and wind, made nuclear energy less cost-competitive. Following the Fukushima disaster of 2011, nuclear safety protocols have been upgraded across the world, which levied additional costs for the upgradation of infrastructure and increased operations and maintenance costs. Due to this, operators of many older commercial reactors, which have an operating life of 40 years and can be extended by 20 more years with infrastructural upgrades, are opting to decommission older units.

The policy-level initiatives from governments across the world have also led to the shutdown of nuclear power plants. The governments in many countries planned to reduce nuclear power in the energy mix of their countries. Such regulatory policies are prevalent among Western European states with a strong renewable portfolio and serious concerns about the environmental footprint and potential risk of operating commercial nuclear power plants.

As per its national policy, Germany plans to shut down all its reactors by the end of 2022. In 2017, Switzerland voted to phase-out nuclear power plants from the country. In September 2020, the Belgian government signed an agreement reaffirming its commitment to phasing-out nuclear power by 2025. Spain declared that it will close four of its seven operating commercial reactors by 2030 and close the rest three reactors within the next five years, completely phasing out nuclear generation by 2035.

The development of renewable energy technologies and increasing economic viability have led to its massive development. Countries across the world are creating huge infrastructures pertaining to renewable power, which has offset the requirement for nuclear reactors. Nuclear power generation is being replaced by renewable energy sources, which led to the closure of nuclear reactors. Therefore, the surge in the development of renewable energy sources is a big boost for the global nuclear reactor decommissioning market.

Therefore, due to the aforementioned factors, commercial rectors are expected to dominate the market studied during the forecast period.

North America is Expected to Witness Significant Growth

North America is one of the largest regions in terms of operable reactors worldwide. The nuclear power reactor decommissioning market is expected to witness significant growth due to the demand from the United States, Canada, and Mexico.

The United States is one of the largest nuclear power producers, accounting for 30% of the global nuclear power generated in 2021. The country's nuclear reactors produced 778.15 TWh of electricity in 2021, representing a slight decline of 1.48% from 2020.

As of August 2022, the United States has 92 operating nuclear power reactors with a combined capacity of 94.7 GWe in 30 states, used by 30 different power companies. Two reactors are under construction with a total of 2.23 GWe.

As the era of nuclear power winds down in the United States, the decommissioning of nuclear power plants is becoming a significant industry. Private companies are acquiring these plants, taking over their licenses, liability, decommissioning funds, and waste contracts. Around 41 reactors with a combined capacity of 19.97 GW were shut down, the latest being the Palisades nuclear plant in Michigan shut down in May 2022. In December 2021, HoltecInternational received approval from the Nuclear Regulatory Commission to acquire the Palisades plant in Covert, Michigan, to decommission and dismantle the plant. Around 198 reactors are expected to shut down by 2030.

The nuclear reactor fleet of the United States is aging. The United States Nuclear Regulatory Commission (NRC) is considering applications for extending operating licenses beyond 60 to 80 years with its subsequent license renewal (SLR) program. However, some plant owners recently opted for early retirement of their nuclear units at 45 to 50 years old.

Intense competition from electricity generation using low-cost shale gas hurt the competitiveness of the nuclear power industry in the country. Record low wholesale electricity prices and the high cost of life extension (PLEX) upgrades have together driven early nuclear plant retirements.

For many years, Canada has been a leader in nuclear research and technology, exporting reactor systems developed in Canada. In 2021, Canada generated 92.6 TWh of electricity from nuclear power plants, accounting for about 15% of the total electricity generation mix. In Ontario, 19 operable reactors with a combined capacity of 13,624 MW and around six reactors with a combined capacity of 2.14 GW were shut down in August 2022.

As of August 2022, Canada has a variety of research and prototype power reactors that are no longer in use and have been shut down. These reactors are in a safe storage state and awaiting final decommissioning. Some of these reactors include the WR-1, the NRX reactor at Chalk River Laboratories (CRL), the MAPLE-1 and MAPLE-2 (Multipurpose Applied Physics Lattice Experiment) reactors at CRL, the Gentilly-1 nuclear generating station in Becancour, QC, the Nuclear Power Demonstration (NPD) reactor in Rolphton, ON, and the Douglas Point nuclear-generating station in Kincardine, ON. These are expected to drive the demand for the Canadian nuclear power reactor decommissioning market during the forecast period.

Therefore, North America is expected to witness significant growth in the nuclear power reactor decommissioning market during the forecast period.

Nuclear Power Reactor Decommissioning Industry Overview

The nuclear power reactor decommissioning market is moderately fragmented. Some of the major players in the market (in no particular order) are Babcock International Group PLC, Fluor Corporation, GE Hitachi Nuclear Services, AECOM, and Westinghouse Electric Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of Study

- 1.2 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD million, till 2027

- 4.3 Nuclear Power Generation Forecast in TWh, till 2027

- 4.4 Recent Trends and Developments

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Reactor Type

- 5.1.1 Pressurized Water Reactor

- 5.1.2 Pressurized Heavy Water Reactor

- 5.1.3 Boiling Water Reactor

- 5.1.4 High-temperature Gas-cooled Reactor

- 5.1.5 Liquid Metal Fast Breeder Reactor

- 5.1.6 Other Reactor Types

- 5.2 By Application

- 5.2.1 Commercial Power Reactor

- 5.2.2 Prototype Power Reactor

- 5.2.3 Research Reactor

- 5.3 By Capacity

- 5.3.1 Below 100 MW

- 5.3.2 100-1000 MW

- 5.3.3 Above 1000 MW

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Asia-Pacific

- 5.4.3 Europe

- 5.4.4 South America

- 5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Babcock International Group PLC

- 6.3.2 James Fisher & Sons PLC

- 6.3.3 NorthStar Group Services Inc.

- 6.3.4 Fluor Corporation

- 6.3.5 GE Hitachi Nuclear Services

- 6.3.6 Studsvik AB

- 6.3.7 Enercon Services Inc.

- 6.3.8 Orano Group

- 6.3.9 Aecom

- 6.3.10 Bechtel Group Inc.

- 6.3.11 Westinghouse Electric Company