|

市場調査レポート

商品コード

1686577

スペインのペットフード:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Spain Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スペインのペットフード:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 290 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

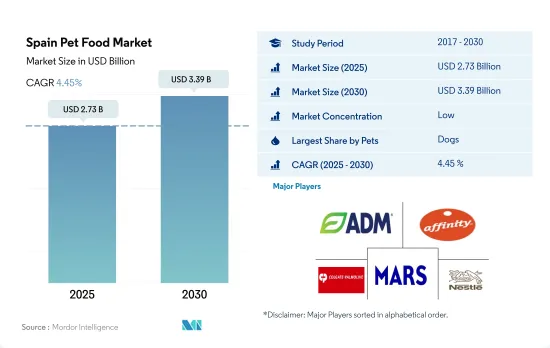

スペインのペットフード市場規模は2025年に27億3,000万米ドルと推定され、2030年には33億9,000万米ドルに達し、予測期間(2025~2030年)のCAGRは4.45%で成長すると予測されています。

犬部門がスペインのペットフード市場を独占

- 2022年、スペインのペットフード市場では犬が圧倒的なシェアを占め、市場規模は12億3,000万米ドルでした。この優位性は、同国のペット総数の約36%(1,010万頭)を占める犬の数の多さに起因しています。ペットの人間化が進むにつれ、ペットの飼い主はグレインフリーやビーガンのドッグフードを含むプレミアムペット製品を好むようになっています。この動向は、予測期間中にCAGR 5.8%でドッグフード市場を押し上げると予想され、国内で最も急成長している分野となっています。

- 猫はスペインのペットフード市場で第2位の市場シェアを占め、2022年の市場規模は6億600万米ドルでした。しかし、猫の市場規模が犬よりも比較的小さい主な理由は、その数の少なさです。スペインにおける猫のペット数はペット数全体の22.5%(630万人)を占め、これは同年の犬よりも37.8%少ないです。さらに、キャットフードの消費量はドッグフードの消費量を大きく下回っています。

- 鳥類、魚類、爬虫類、げっ歯類を含むその他のペット動物は、スペインのペット数全体の約41.3%を占めましたが、2022年のペットフード市場総額の21.4%を占めるに過ぎませんでした。これは、これらのペットが一般的に小型であるため、比較的少量の餌しか必要としないことに起因しています。

- パンデミック時のペット飼育の増加、ペットの健康のためのプレミアムペットフードや特殊食への需要の高まり、またオーガニックペットフードやおやつなどの新製品を導入する企業の努力により、ペットフード市場は予測期間中に拡大すると予想されます。

スペインのペットフード市場動向

アニマルシェルターや認可を受けたブリーダーからコンパニオンとして猫を飼うケースが増えていることに加え、猫を飼うことのメリットに対する意識が高まっていることが、同国の猫市場を牽引しています。

- スペインは猫の数よりも犬の数が多いです。この動向は欧州とは逆です。人々は、無条件の友情と一人で家にいる間の安心感から犬をより快適に感じ、その結果、同国では2022年に犬の数が猫の数を390万上回りました。しかし、2020~2022年にかけては、ロックダウンで家に閉じこもる人が増え、猫は室内で長時間生活できるため、猫の数が増加しました。猫の平均寿命は20年以上であることから、パンデミック時の猫の飼育動向は、ペットフード市場により長い時間的影響を及ぼすと予想されました。

- 国内では、家庭で猫をペットとして飼う世帯が増加しました。例えば、猫を飼っている世帯の割合は2019年の11%から2021年には16%に増加しました。ペットの人間化の高まりにより、猫をペットとして所有する世帯が増加していること、猫は犬よりも狭い場所でも生活できることから、2019~2021年にかけて猫の数が55.2%増加しました。

- ペットの入手は、一般的に国内の動物保護施設や認可ブリーダーを通じて行われます。ペットショップでは猫の販売が禁止されているなどペット取引に規制があり、国内では認可ブリーダーの数が少ないため、人々は動物保護施設からペットを飼うことを好みます。猫をペットとして飼う世帯の増加、ペットの人間化の進展、狭い場所にも適応できるなどの利点が、同国における猫の飼育数の増加に役立っていると予想され、このことも予測期間中の猫用ペットフード市場の成長に貢献すると思われます。

高品質でプレミアムなペットフードへの動向とそれに関連する意識の高まりによるペットフードへの支出の増加

- 欧州では、スペインはペットの総数で第4位の地位を占めています。スペインにおけるペットへの支出は一貫して上昇しており、2019~2022年の間に約16.6%増加しました。この上昇は主にペットの人間化とプレミアム化の2つの理由によるものです。スペインでは、2020年の時点で、37.0%の世帯が最低1匹のペットを飼っており、ペットの飼い主は、ペットを家族の重要な一員と認識するようになっており、ペットの人間化の傾向が強まっていることを示しています。

- 2019~2022年にかけて、ペットオーナーが犬用ペットフードにかける年間支出は約21.8%増加し、猫用は約22.3%増加、その他のペット用は約9.0%増加しました。また、犬用ペットフードの売上高は2016~2020年にかけてCAGR 5.9%を記録しましたが、猫用ペットフードの売上高はCAGR 3.9%と伸び悩みました。さらに、ペットの飼い主は自然で的を絞った栄養への関心を高めており、"Royal Canin"のようなプレミアムブランドへの需要の急増につながっています。同ブランドの小売売上高は、2016年の5,020万米ドルから2022年には7,940万米ドルに増加し、CAGRは7.9%を記録しました。

- 同国のペットオーナーは、様々なペットショップ、ハイパーマーケット、eコマースからペット用品を購入しています。同国では、オフラインの店舗がペット用品の購入先として上位を占めています。スペインのペットフード価格は、2022年のロシアとウクライナの政治紛争の影響を受け、原材料の調達に課題が生じ、同国のペット支出への影響につながりました。このような状況にもかかわらず、高品質でプレミアムなペットフードを求める傾向が強まっており、その利点に対する認識も高まっていることから、予測期間中のペット支出額の伸びは維持されると予測されます。

スペインのペットフード産業概要

スペインのペットフード市場は断片化されており、上位5社で38.82%を占めています。この市場の主要企業はADM、Affinity Petcare SA、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、Mars Incorporated、Nestle(Purina)などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他のペット

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブ製品別

- ドライペットフード

- キブル

- その他のドライフード

- ウェットペットフード

- ペット用栄養補助食品・サプリメント

- サブ製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質・ペプチド

- ビタミン・ミネラル

- その他

- ペット用おやつ

- サブ製品別

- カリカリおやつ

- デンタルおやつ

- フリーズドライ・ジャーキーおやつ

- ソフト・チューイーおやつ

- その他

- ペット用獣医療食

- サブ製品別

- 糖尿病

- 消化器過敏症用

- オーラルケア

- 腎臓

- 尿路疾患

- その他

- フード

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Affinity Petcare SA

- Alltech

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- Dechra Pharmaceuticals PLC

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- Schell & Kampeter Inc.(Diamond Pet Foods)

- Virbac

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 52816

The Spain Pet Food Market size is estimated at 2.73 billion USD in 2025, and is expected to reach 3.39 billion USD by 2030, growing at a CAGR of 4.45% during the forecast period (2025-2030).

Dogs dominate the Spanish pet food market as they are highly owned pets in the country

- In 2022, dogs were the dominant players in the pet food market in Spain, with a market value of USD 1.23 billion. This dominance can be attributed to their large population in the country, accounting for approximately 36% (10.1 million) of the total pet population. As pet humanization continues to increase, pet owners are increasingly favoring premium pet products, including grain-free and vegan dog food. This trend is expected to boost the dog food market at a CAGR of 5.8% during the forecast period, making it the fastest-growing segment in the country.

- Cats held the second-largest market share in the Spanish pet food market, valued at USD 606 million in 2022. However, the main reason for cats holding a comparatively smaller market size than dogs was their lower population. The pet cat population in Spain accounted for 22.5% (6.3 million) of the total pet population, which was 37.8% less than that of dogs in the same year. Additionally, the consumption of cat food is significantly lower than that of dog food.

- Although other pet animals, including birds, fish, reptiles, and rodents, made up around 41.3% of the overall pet population in Spain, they only accounted for 21.4% of the total pet food market value in 2022. This can be attributed to the fact that these pets are typically small in size and, therefore, require relatively small amounts of food.

- With the rise in pet ownership during the pandemic and growing demand for premium pet food and specialized diets for pets' health, as well as the efforts of companies to introduce new products like organic pet foods and treats, the pet food market is expected to expand during the forecast period.

Spain Pet Food Market Trends

The growing adoption of cats as companions from animal shelters and licensed breeders, along with increasing awareness about the benefits of owning a cat, is driving the cat market in the country

- Spain has a larger dog population than a cat population. This trend is opposite to the trend in Europe. People feel more comfortable with dogs due to their unconditional friendship and security while at home alone, which helped the population of dogs to more than the population of cats in the country by 3.9 million in 2022. However, between 2020 and 2022, there was an increase in the cat population as people were confined to their homes because of the lockdowns, and cats could live for a long time indoors without being cooped up. This trend of adoption of cats during the pandemic was expected to have a wider time effect on the pet food market as the average lifespan of cats is more than 20 years.

- There was a rise in the number of households owning a cat as a pet in their homes in the country. For instance, the share of households owing a cat increased from 11% in 2019 to 16% in 2021. An increasing share of households own a cat as a pet due to the rise in pet humanization, and cats can live in smaller places than dogs, which led to an increase of 55.2% in the cat population between 2019 and 2021.

- The acquisition of pets is generally through animal shelters and licensed breeders in the country. People prefer to adopt pets from animal shelters because there are regulations on the pet trade, as pet shops are banned from selling cats, and less number of licensed breeders are present in the country. The increasing number of households owing a cat as a pet, the rise in pet humanization, and benefits such as the ability to adapt to smaller places are anticipated to have helped in increasing the adoption of the cat population in the country, and this will also help the pet food market for cats to witness growth during the forecast period.

The trend toward high-quality and premium pet food and related growing awareness is increasing expenditure on the pet food

- In Europe, Spain holds the fourth position in terms of the total number of pets. The expenditure on pets in Spain is consistently rising, which increased by about 16.6% between 2019 and 2022. This upsurge is primarily due to two reasons: pet humanization and premiumization. In Spain, as of 2020, 37.0% of households possessed a minimum of one pet, and pet owners increasingly perceive their pets as integral members of their families, signifying the growing trend of pet humanization.

- Between 2019 and 2022, pet owners' annual spending on pet food for dogs increased by around 21.8%, while spending on cats increased by about 22.3%, and other pets saw an increase of about 9.0%. Additionally, sales of dog pet food registered a CAGR of 5.9% from 2016 to 2020, while cat food sales increased at a slower CAGR of 3.9%. Additionally, pet owners are increasingly interested in natural and targeted nutrition, leading to a surge in demand for premium brands like "Royal Canin." The brand's retail sales increased from USD 50.2 million in 2016 to USD 79.4 million in 2022, registering a CAGR of 7.9%.

- Pet owners in the country bought pet supplies from various pet shops, hypermarkets, and e-commerce. Offline stores were the top preference for pet supplies in the country. Pet food prices in Spain were affected by the political conflict between Russia and Ukraine in 2022, causing challenges in procuring raw materials and leading to an impact on pet expenditure in the country. Despite this, the increasing trend toward high-quality and premium pet food, as well as the growing awareness of its benefits, is projected to sustain the growth of pet expenditure during the forecast period.

Spain Pet Food Industry Overview

The Spain Pet Food Market is fragmented, with the top five companies occupying 38.82%. The major players in this market are ADM, Affinity Petcare SA, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), Mars Incorporated and Nestle (Purina) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Sub Dry Pet Food

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Affinity Petcare SA

- 6.4.3 Alltech

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 Dechra Pharmaceuticals PLC

- 6.4.6 General Mills Inc.

- 6.4.7 Mars Incorporated

- 6.4.8 Nestle (Purina)

- 6.4.9 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms