|

市場調査レポート

商品コード

1686561

高性能断熱材:市場シェア分析、産業動向・統計、成長予測(2025~2030年)High-Performance Insulation Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 高性能断熱材:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 208 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

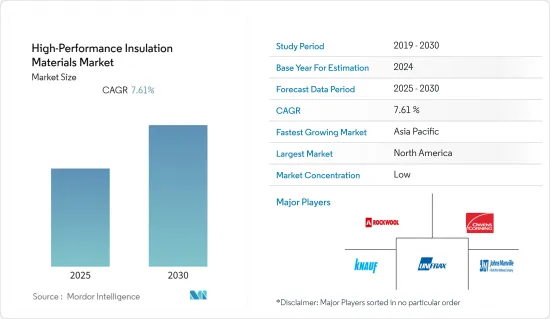

高性能断熱材市場は予測期間中にCAGR 7.61%を記録する見込みです。

主なハイライト

- 石油・ガス産業での使用量の増加と、温室効果ガス排出と省エネルギーに関する意識の高まりが、高性能断熱材市場の成長を促進するとみられます。

- 反面、CFCを含む断熱材やフォーム製品では、設置やメンテナンスのコストが高く、耐用年数が比較的短く、可燃性が高いことが市場の成長を妨げると予想されます。

- アジア太平洋地域におけるインフラ活動への投資の増加は、調査対象の市場にとって新たな機会をもたらすと予想されます。

高性能断熱材の市場動向

石油・ガス産業からの需要増加

- 高温の石油・ガス組成物は坑口で上昇し、XMT、マニホールド、さまざまな重要機器、スプール、フローラインを通って輸送され、ライザーが石油を地表に運びます。

- 高性能断熱材は、主に海底パイプライン用途の需要の増加により、石油・ガス分野から大きな需要を目の当たりにしています。

- さらに、これらの材料は、耐火性や耐水性、優れた耐熱性、強化された遮音性、軽量化、薄型化など、石油・ガス分野で求められる特性を備えています。

- 経済産業省によると、2021年の日本の原油生産量は約49万キロリットルで、前年の約51万2,000キロリットルから減少しました。

- StatCanによると、米国における2021年10月の原油および同等製品の生産量は10.8%増の2,440万立方メートルとなり、2019年12月以来の原油生産量となりました。

- 前述の要因により、予測期間中に高性能断熱材の使用量が増加するとみられます。

市場を独占するアジア太平洋地域

- 予測期間中、アジア太平洋地域が高性能断熱材市場を独占すると予想されます。

- 同地域の石油・ガス産業と建設分野の成長が、こうした断熱パネルの需要を大幅に押し上げています。

- アジア太平洋地域の石油・ガス産業は、エネルギーと石油化学製品の需要増加により成長しています。インド、マレーシア、インドネシア、中国、韓国、日本などの国々では、海洋掘削活動が活発化しています。

- 中国の2022年1~2月の原油生産量は3,347万トンと、前年同期比で約4.6%増加しました。中国国家統計局によると、1日の原油生産量はほぼ57万6,000トンです。

- OICAによると、2021年の自動車生産台数は784万6,955台で、2020年の806万7,557台に比べ3%減少しました。しかし、日本における電気自動車の需要は予測期間中に伸びると予測されます。

- 航空宇宙分野では、インドブランドエクイティ財団(IBEF)によると、同国の航空産業は今後4年間で35,000カロールインドルピー(49億9,000万米ドル)の投資が見込まれています。

- 前述の要因により、予測期間中に高性能断熱材の需要が増加する可能性が高いです。

高性能断熱材産業の概要

世界の高性能断熱材市場は非常に細分化されており、調査対象となった市場では上位10社が顕著なシェアを獲得しています。市場の主要企業には、Owens Corning、Knauf Gips KG、Rockwool、Johns Manville、Unifraxなどが含まれます(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 石油・ガス産業における利用の拡大

- 温室効果ガス排出とエネルギー節約に関する意識の高まり

- 抑制要因

- 高い設置・メンテナンスコストと比較的低い耐用年数

- CFCを含む断熱材やフォーム製品の高い燃焼性

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 素材タイプ別

- エアロゲル

- 真空断熱パネル(VIP)

- ガラス繊維

- セラミックファイバー

- 高性能フォーム

- その他

- エンドユーザー産業別

- 石油・ガス

- 産業

- 建築・建設

- 輸送

- 発電

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Aerogel Technologies LLC

- Armacell

- Aspen Aerogels Inc.

- BASF SE

- Cabot Corporation

- IBIDEN

- Isolite Insulating Products Co. Ltd

- Johns Manville

- Knauf Gips KG

- Luyang Energy-Saving Materials Co. Ltd

- Morgan Advanced Materials

- Owens Corning

- Panasonic Corporation

- PAR Group

- Rath Group

- ROCKWOOL Group

- Saint-Gobain

- Unifrax

第7章 市場機会と今後の動向

- アジア太平洋地域におけるインフラ投資の増加

目次

Product Code: 52653

The High-Performance Insulation Materials Market is expected to register a CAGR of 7.61% during the forecast period.

Key Highlights

- The growing usage in the oil and gas industry and rising awareness regarding greenhouse emissions and energy savings are likely to drive the growth of the high-performance insulation materials market.

- On the flip side, high set-up and maintenance costs, relatively low service life, and high flammability with insulated materials and foam products that contain CFC are expected to hinder the market's growth.

- Increasing investments in infrastructural activities in Asia-Pacific are expected to unveil new opportunities for the market studied.

High Performance Insulation Materials Market Trends

Increasing Demand from the Oil and Gas Industry

- The hot oil and gas composition flows up at the wellhead and is transported through XMTs, manifolds, various critical instruments, spools, and flow lines before the riser brings the oil to the surface.

- High-performance insulation materials are witnessing a huge demand from the oil and gas sector, primarily owing to the increasing demand for subsea pipeline applications.

- Additionally, these materials offer properties, such as fire and water resistance, excellent thermal resistance, enhanced acoustic insulation, lightweight, and reduced thickness, that are required in the oil and gas sector.

- According to the Ministry of Economy, Trade, and Industry (METI), in 2021, approximately 490 thousand kiloliters of crude oil were produced in Japan, down from about 512 thousand kiloliters in the previous year.

- According to StatCan, the production of crude oil and equivalent products in the United States rose 10.8% in October 2021 to 24.4 million cubic meters, the highest crude production level since December 2019.

- The aforementioned factors are likely to result in an increase in the usage of high-performance insulation materials during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate the market for high-performance insulation materials during the forecast period.

- The growth in the oil and gas and the construction sector in the region has significantly boosted the demand for such insulation panels.

- The oil and gas industry in the Asia-Pacific region is growing due to the increasing demand for energy and petrochemicals. Countries such as India, Malaysia, Indonesia, China, South Korea, and Japan are experiencing increased offshore drilling activities.

- The crude oil output of China has registered at 33.47 million tons in the first two months of 2022, which is about 4.6% up from the same period of the previous year. According to the National Bureau of Statistics China, the daily output of crude oil is nearly 576,000 tons.

- According to OICA, the production of vehicles in 2021 accounted for 78,46,955 units, a fall of 3% compared to 80,67,557 units produced in 2020. However, the demand for electric vehicles in Japan is projected to grow over the forecast period.

- In the aerospace sector, according to the India Brand Equity Foundation (IBEF), the country's aviation industry is expected to witness INR 35,000 crore (USD 4.99 billion) investment in the next four years.

- The aforementioned factors will likely increase the demand for high-performance insulation materials during the forecast period.

High Performance Insulation Materials Industry Overview

The global High-Performance Insulation Materials Market is highly fragmented, with the top 10 players capturing a noticeable share in the market studied. Some of the major players in the market include (not in any particular order) Owens Corning, Knauf Gips KG, Rockwool, Johns Manville, and Unifrax, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in the Oil and Gas Industry

- 4.1.2 Rising Awareness Regarding Greenhouse Emissions and Energy Savings

- 4.2 Restraints

- 4.2.1 High Set-up and Maintenance Costs and Relatively Low Service Life

- 4.2.2 High Flammability with Insulated Materials and Foam Products that Contain CFC

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Material Type

- 5.1.1 Aerogel

- 5.1.2 Vacuum Insulation Panel (VIP)

- 5.1.3 Fiberglass

- 5.1.4 Ceramic Fiber

- 5.1.5 High-performance Foam

- 5.1.6 Other Material Types

- 5.2 End-user Industry

- 5.2.1 Oil and Gas

- 5.2.2 Industrial

- 5.2.3 Building and Construction

- 5.2.4 Transportation

- 5.2.5 Power Generation

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Aerogel Technologies LLC

- 6.4.3 Armacell

- 6.4.4 Aspen Aerogels Inc.

- 6.4.5 BASF SE

- 6.4.6 Cabot Corporation

- 6.4.7 IBIDEN

- 6.4.8 Isolite Insulating Products Co. Ltd

- 6.4.9 Johns Manville

- 6.4.10 Knauf Gips KG

- 6.4.11 Luyang Energy-Saving Materials Co. Ltd

- 6.4.12 Morgan Advanced Materials

- 6.4.13 Owens Corning

- 6.4.14 Panasonic Corporation

- 6.4.15 PAR Group

- 6.4.16 Rath Group

- 6.4.17 ROCKWOOL Group

- 6.4.18 Saint-Gobain

- 6.4.19 Unifrax

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Investments in Infrastructural Activities in Asia-Pacific