アジア太平洋地域の飼料用カビ毒除去剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Asia-Pacific Feed Mycotoxin Detoxifiers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 229 Pages

- 納期

- 2~3営業日

- 商品コード

- 1686290

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

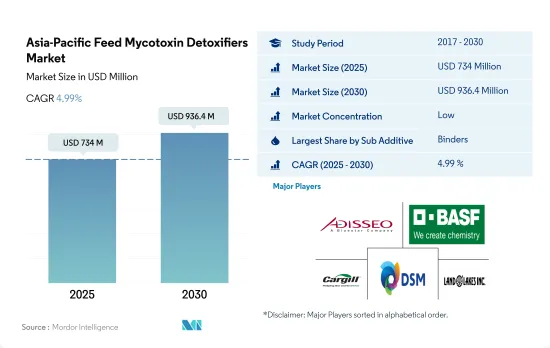

アジア太平洋地域の飼料用カビ毒除去剤市場規模は2025年に7億3,400万米ドルと推定され、2030年には9億3,640万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは4.99%で成長する見込みです。

- 2022年、アジア太平洋地域の飼料添加物市場では、カビ毒除去剤のシェアが6.1%、結合剤のシェアが4.1%、バイオトランスフォーマーのシェアが2.1%となっています。カビ毒除去剤は主に病気を予防するために動物栄養学で必要とされ、結合剤は主要な要件として浮上しました。中国はアジア太平洋地域の飼料用カビ毒除去剤市場をリードし、金額ベースで44.2%のシェアを占めているが、これは2022年の飼料生産量が2億4,320万トンと多く、2017年から2022年にかけて20.1%増加したことに起因しています。

- 動物の種類の中では、家禽がアジア太平洋地域の飼料用カビ毒除去剤市場で最も大きなシェアを占め、2022年には市場全体の47.3%を占め、予測期間(2023~2029年)のCAGRは5.6%と予想されます。この成長は、2017年から2022年にかけて家禽の頭数が6.5%増加したことによるものです。

- 2022年に4億2,130万米ドルと評価された結合剤セグメントは、カビ毒が動物の血流に入るのを防ぎ、病気や神経障害を予防する能力があるため、カビ毒除去剤に高度に消費されています。予測期間中(2023-2029年)のCAGRは4.9%と予測されています。バイオトランスフォーマーは2022年に2億1,450万米ドルを占めました。

- アジア太平洋地域の飼料用カビ毒除去剤市場は、予測期間中にCAGR 5.0%を記録すると予測されています。これは主に、マイコトキシンが飼料の内容物を損傷する潜在的なリスクと、カビ毒除去剤市場を拡大段階へと押し上げている同地域の一貫した人口増加によるものです。

- アジア太平洋地域の飼料用カビ毒除去剤市場は、中国、インド、日本の3カ国によって支配されています。これらの国を合わせると、この地域の2022年の市場シェア値の約59.3%を占めています。

- 中国は、2022年の市場価値が2億8,140万米ドルで、アジア太平洋地域の家禽人口の39.7%を占め、畜産と飼料生産が盛んなため、この地域で最大の飼料用カビ毒除去剤の消費国です。飼料用カビ毒除去剤の市場価値は、予測期間中のCAGRが4.9%で、2029年には3億9,400万米ドルに増加すると予想されます。

- インドはこの地域で2番目に大きな飼料用マイコトキシン消費国であり、家禽セグメントが全動物種の中で市場シェアの66.9%を占めています。家禽の市場価値は2017年から2022年の間に46.6%増加し、これは同期間の頭数の6.2%増加によるものです。

- 日本とタイは、アジア太平洋地域の飼料用カビ毒除去剤市場で最も急速に成長している国であり、予測期間中のCAGRは5.8%です。この動向は、これらの国々における飼料生産の増加によるものです。例えば日本では、総飼料生産量は2017年の2,190万トンから2029年には2,400万トンに増加すると予測されています。

- したがって、アジア太平洋地域の飼料用カビ毒除去剤市場は、予測期間中にCAGR 5.0%を記録すると予測されます。この成長は、食肉と乳製品の需要の増加に加え、動物の健康に対する意識の高まりと、商業畜産業におけるマイコトキシン感染管理の必要性に起因しています。

アジア太平洋地域の飼料用カビ毒除去剤の市場動向

アジア太平洋地域の開発途上国における可処分所得の増加、養鶏業に対する政府の支援制度、中国は鶏卵の最大生産国であることが、同地域における養鶏人口の増加に寄与しています。

- アジア太平洋地域は世界の農業セクターを支配しており、中でも家禽類は最大のセグメントであり、2022年の世界の家禽類生産量の42.4%を占めています。この鶏肉消費の増加は、インドやベトナムなどの新興諸国における人気の上昇、急速な都市化、可処分所得の増加によってもたらされ、2021年には2017年から37.3%の鶏肉人口の増加を記録しました。

- 2021年には、中国、インドネシア、インドがこの地域の鶏肉市場で大きなシェアを占めており、市場シェアはそれぞれ39.7%、25.3%、5.7%です。このような鶏肉製品需要の伸びは、卵、食肉需要の増加、鶏肉産業を支援する政府制度に起因しています。例えば、インドの畜産・酪農省は、養鶏事業を支援するための資本基金制度を導入し、農家に収量の質を向上させる方法を教育しています。中国は世界最大の鶏卵生産国で、消費量と生産量は世界生産の40%以上を占める。9億羽を超える採卵鶏と、年間6,000万羽のヒナをふ化させる国内最大のレイヤー養鶏センターを擁し、同国のレイヤー養鶏は著しい成長を記録しました。

- この地域のブロイラー生産も、鶏肉に対する消費者需要の増加により急速に増加しています。フィリピンの2021年の鶏肉生産量は2017年から2.2%の増加を記録しました。このように、この地域の鶏肉生産は、鶏肉への消費者の嗜好の変化と鶏肉産業の急速な開発により、さらに増加すると予想されます。こうした鶏肉生産の伸びは、飼料添加物の需要増につながると予想されます。

養殖技術の向上、飼料工場の拡大、インド政府の取り組みが養殖用飼料の増産に役立っています。

- アジア太平洋地域は世界の養殖飼料生産市場の主要企業であり、魚とエビが主な生産品目です。2021年、この地域は3,760万トンの養殖飼料を生産し、地域全体の飼料生産量の8.7%を占めました。この地域のいくつかの国々は、需要の増加に対応するため、技術の進歩や飼料の使用量の増加を通じて、養殖生産の拡大や集約化に力を入れています。インドは、漁業省への予算配分を増やし、生産を促進しています。

- 養殖用飼料は魚類が大きなシェアを占めており、2022年には3,110万トンと、2017年比で66%から増加しました。この増加は、農地の養殖池への転換、魚類養殖技術の向上、生産の集約化によるものです。エビ飼料の生産は、2022年の同地域の水産飼料生産の4.2%を占めました。この地域のいくつかの国は、認証された持続可能な水産物の生産を増やすために、いくつかの政府の取り組みを通じて自給自足の養殖システムを導入し始めているため、予測期間中に急速に増加すると予想されます。

- 中国がアジア太平洋地域の水産飼料市場を独占しており、より高い能力を持つ飼料工場の増加により、2022年には市場シェアの51.2%を占めました。例えば、AB Agriは中国で9番目の飼料工場を開設し、年産24万トンの能力を持つ工場となりました。水産養殖生産の増加、水産養殖の拡大、飼料消費の増加などの要因が、予測期間中にこの地域における水産飼料生産の成長を促進すると予想されます。

アジア太平洋地域の飼料用カビ毒除去剤産業の概要

アジア太平洋地域の飼料用カビ毒除去剤市場は断片化されており、上位5社で34.73%を占めています。この市場の主要企業は以下の通りです。Adisseo, BASF SE, Cargill Inc., DSM Nutritional Products AG and Land O'Lakes(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 養豚

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- フィリピン

- 韓国

- タイ

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ添加剤

- 結合剤

- バイオトランスフォーマー

- その他のマイコトキシン解毒剤

- 動物

- 水産養殖

- サブアニマル別

- 魚類

- エビ

- その他の養殖種

- 家禽類

- サブ動物別

- ブロイラー

- レイヤー

- その他の鳥類

- 反芻動物

- サブ動物別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- フィリピン

- 韓国

- タイ

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Adisseo

- Alltech, Inc.

- BASF SE

- Brenntag SE

- Cargill Inc.

- DSM Nutritional Products AG

- EW Nutrition

- Kemin Industries

- Land O'Lakes

- SHV(Nutreco NV)

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 51674

The Asia-Pacific Feed Mycotoxin Detoxifiers Market size is estimated at 734 million USD in 2025, and is expected to reach 936.4 million USD by 2030, growing at a CAGR of 4.99% during the forecast period (2025-2030).

- In 2022, the Asia-Pacific feed additives market witnessed a 6.1% share of mycotoxin detoxifiers, with binders accounting for a significant 4.1% share, and biotransformers, a 2.1% share in terms of value. Mycotoxin detoxifiers are primarily required in animal nutrition to prevent diseases, and binders emerged as a major requirement. China leads the market in the Asia-Pacific region for feed mycotoxin detoxifiers, holding a 44.2% share in terms of value, which was attributed to its higher feed production of 243.2 million metric tons in 2022, with a 20.1% increase from 2017 to 2022.

- Among animal types, poultry held the most significant share in the Asia-Pacific feed mycotoxin detoxifiers market, accounting for 47.3% of the overall market value in 2022, with an expected CAGR of 5.6% during the forecast period (2023-2029). This growth is due to the increased headcount of poultry by 6.5% from 2017 to 2022.

- The binder segment, valued at USD 421.3 million in 2022, is highly consumed in mycotoxin detoxifiers due to its ability to prevent mycotoxins from entering the animal's bloodstream and preventing diseases and neurological disorders. It is projected to register a CAGR of 4.9% during the forecast period (2023-2029). Biotransformers accounted for USD 214.5 million in 2022.

- The Asia-Pacific feed mycotoxin detoxifiers market is expected to register a CAGR of 5.0% during the forecast period, mainly due to the potential risks of mycotoxins damaging the feed content and the consistently increasing population in the region, which has pushed the mycotoxin detoxifier market toward the expansion phase.

- The feed mycotoxin detoxifiers market in the Asia-Pacific region is dominated by three countries, which include China, India, and Japan. Together, these countries held about 59.3% of the market share value in 2022 in the region.

- China, with a market value of USD 281.4 million in 2022, is the largest feed mycotoxin detoxifier consumer in the region due to the country's high livestock and feed production, accounting for 39.7% of the Asia-Pacific poultry population. The market value for feed mycotoxin detoxifiers is expected to increase to USD 394.0 million in 2029, with a CAGR of 4.9% during the forecast period.

- India is the second-largest feed mycotoxin consumer in the region where the poultry segment is dominant, accounting for 66.9% of the market share among all animal types. The market value of poultry increased by 46.6% between 2017 and 2022, owing to a 6.2% increase in the headcount during the same period.

- Japan and Thailand are the fastest-growing countries in the Asia-Pacific feed mycotoxin detoxifiers market, with a CAGR of 5.8% during the forecast period. This trend is due to increased feed production in these countries. For instance, in Japan, the total feed production is expected to increase from 21.9 million metric tons in 2017 to 24.0 million metric tons in 2029.

- Therefore, the Asia-Pacific feed mycotoxin detoxifiers market is anticipated to register a CAGR of 5.0% during the forecast period. This growth is attributed to the increasing demand for meat and dairy products, along with the rising awareness of animal health and the need for managing mycotoxin infection in the commercial animal industry.

Asia-Pacific Feed Mycotoxin Detoxifiers Market Trends

The growing disposable income in developing countries of Asia-Pacific and government support schemes for poultry industry, and China is largest producer of eggs are helping in growth of poultry population in the region

- Asia-Pacific dominates the global agricultural sector, with poultry being the largest segment, which accounted for 42.4% of global poultry production in 2022. This increase in poultry consumption is driven by a rise in popularity, rapid urbanization, and growing disposable incomes in developing countries, such as India and Vietnam, which recorded a 37.3% increase in poultry population in 2021 from 2017.

- In 2021, China, Indonesia, and India held a significant share of the poultry market in the region, with market shares of 39.7%, 25.3%, and 5.7%, respectively. This growth in demand for poultry products can be attributed to the increase in demand for eggs, meat, and government schemes that support the poultry industry. For instance, the Department of Animal Husbandry & Dairy in India is introducing capital fund schemes to support poultry businesses, educating farmers on how to improve their yield quality, which is expected to boost the growth of the market. China is the largest producer of eggs in the world, with consumption and production accounting for over 40% of global production. With over 900 million stock-laying hens and the country's largest layer poultry farming center hatching 60 million chicks per year, the country's layer farming recorded significant growth.

- Broiler production in the region is also rapidly increasing due to the increased consumer demand for chicken meat. The Philippines recorded a 2.2% increase in chicken meat production in 2021 from 2017. As such, the region's poultry production is expected to increase further, driven by a shift in consumer preferences toward poultry meat and the rapid development of the poultry industry. This growth in poultry production is expected to lead to an increase in demand for feed additives.

Improvement in fish farming technologies, expansion in number of feed mills and Indian government initiatives are helping in increasing the aquaculture feed production

- Asia-Pacific is a major player in the global aquaculture feed production market, with fish and shrimp being the primary products. In 2021, the region produced 37.6 million metric tons of aquaculture feed, which accounted for 8.7% of the region's total feed production. Several countries in the region are focusing on expanding their aquaculture production and intensification through technological advancement and increased use of feed to meet the increasing demand. India increased its budget allocation to the Department of Fisheries to boost production.

- Fish has a significant share of aquaculture feed, which accounted for 31.1 million metric tons in 2022, an increase from 66% compared to 2017. This growth was due to the conversion of agricultural land to aquaculture ponds, the improvement of fish farming technologies, and the intensification of production. Shrimp feed production accounted for 4.2% of the aquafeed production in the region in 2022. It is expected to increase rapidly during the forecast period as some countries in the region have started implementing a self-sufficient aquaculture system through several government initiatives to increase the production of certified sustainable seafood.

- China dominates the aquafeed market in the Asia-Pacific region, which accounted for 51.2% of the market share in 2022 due to an increase in the number of feed mills with higher capacities. For instance, AB Agri opened its ninth feed mill in China, a plant with an annual capacity of 240,000 tons. Factors such as an increase in aquaculture production, expansion of aqua farming, and rise in consumption of feed are expected to drive the growth of aquafeed production in the region during the forecast period.

Asia-Pacific Feed Mycotoxin Detoxifiers Industry Overview

The Asia-Pacific Feed Mycotoxin Detoxifiers Market is fragmented, with the top five companies occupying 34.73%. The major players in this market are Adisseo, BASF SE, Cargill Inc., DSM Nutritional Products AG and Land O'Lakes (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Philippines

- 4.3.7 South Korea

- 4.3.8 Thailand

- 4.3.9 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Binders

- 5.1.2 Biotransformers

- 5.1.3 Other Mycotoxin Detoxifiers

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Philippines

- 5.3.7 South Korea

- 5.3.8 Thailand

- 5.3.9 Vietnam

- 5.3.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Alltech, Inc.

- 6.4.3 BASF SE

- 6.4.4 Brenntag SE

- 6.4.5 Cargill Inc.

- 6.4.6 DSM Nutritional Products AG

- 6.4.7 EW Nutrition

- 6.4.8 Kemin Industries

- 6.4.9 Land O'Lakes

- 6.4.10 SHV (Nutreco NV)

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

アジア太平洋地域の飼料用カビ毒除去剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 229 Pages

- 納期

- 2~3営業日