|

市場調査レポート

商品コード

1801942

同期発電機市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Synchronous Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 同期発電機市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年08月05日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

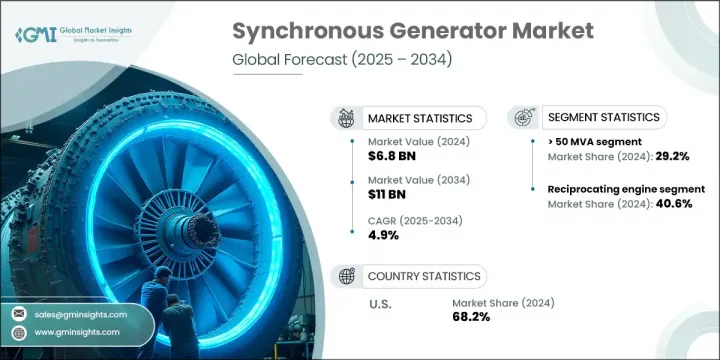

同期発電機の世界市場規模は、2024年に68億米ドルとなり、CAGR 4.9%で成長し、2034年には110億米ドルに達すると推定されます。

エネルギー効率の高い技術が重視されるようになり、高性能で信頼性の高い電力インフラへのニーズが高まっていることが、市場拡大の主な要因となっています。再生可能エネルギー・プロジェクトの成長は、断熱材や材料科学の進歩と相まって、この分野の進化を形成し続けています。同期発電機は現代の電力システムに不可欠なもので、安定した電圧と周波数を提供し、電力網の安定性を支えています。その用途はよりダイナミックになり、従来のバックアップ的役割から、分散型エネルギーシステムやピーク負荷エネルギーシステムのアクティブ・コンポーネントへと拡大しています。

世界の電力需要の急増に伴い、IoT機能を備えたインテリジェント発電機システムの統合は、運用モデルを変革しつつあります。これらの次世代発電機は、遠隔診断、予知保全、エネルギー最適化など、現代のエネルギーフレームワークに不可欠な機能をサポートしています。老朽化したインフラのアップグレードや、送電網の寸断頻度の増大と相まって、エネルギーの信頼性に対する懸念が高まっていることも、こうしたシステムの採用を加速させています。持続可能性と規制遵守の重視の高まりは、設計、制御機能、スマート・コネクティビティの技術革新を後押しし、これらの機械をより幅広い産業と用途で不可欠なものにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 68億米ドル |

| 予測金額 | 110億米ドル |

| CAGR | 4.9% |

発電機セグメントは2024年に40.6%のシェアを占め、2034年までにCAGR 4.5%以上で成長すると予測されています。強力な性能、メンテナンスの容易さ、信頼性の高い出力により、さまざまな運用シナリオに最適です。このセグメントの継続的な関連性は、多様なエンドユーザー要件への適応性と費用対効果にあります。

定格出力5MVA未満のユニットは、分散型電源セットアップ、バックアップシステム、中小規模の産業用アプリケーションでの使用の増加により、2034年までCAGR 5%で成長すると予想されます。インテリジェント制御システム、アップグレードされた冷却機能、遠隔監視インターフェイスなどの機能強化が、現代の電力エコシステムにおける役割の拡大を後押ししています。

アジア太平洋同期発電機市場は、2024年に37.5%のシェアを占める。産業活動の加速とエネルギー発電インフラへの大規模投資が、同地域の成長を促進しています。分散型発電やスマートマイクログリッドへのシフトは、特に地方自治体が需要対応プログラムを展開し、送電網の回復力に投資していることから、さらに勢いを増しています。

同期発電機市場の主要企業は、スマートコネクティビティとIoT対応システムによるデジタルトランスフォーメーションをターゲットに、先進的な製品開拓に多額の投資を行っています。多くの企業は、特に高成長市場において、現地生産能力とサービスネットワークを強化することにより、地理的な足跡を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 原材料の入手可能性と調達分析

- 製造能力評価

- サプライチェーンのレジリエンスとリスク要因

- 配電網分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

- 同期発電機のコスト構造分析

- 新たな機会と動向

- IoTテクノロジーによるデジタル変革

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略的ダッシュボード

- 戦略的取り組み

- 主要なパートナーシップとコラボレーション

- 主要なM&A活動

- 製品の革新と発売

- 市場拡大戦略

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:原動機別、2021年~2034年

- 主要動向

- ガスタービン

- 蒸気タービン

- 往復エンジン

- その他

第6章 市場規模・予測:フェーズ別、2021年~2034年

- 主要動向

- 単相

- 三相

第7章 市場規模・予測:出力別、2021年~2034年

- 主要動向

- 5 MVA未満

- 5 MVA~15 MVA以上

- 15MVA~30MVA以上

- 30MVA~50MVA以上

- 50MVA以上

第8章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 産業

- ユーティリティ

第9章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- ニュージーランド

- マレーシア

- インドネシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- ナイジェリア

- トルコ

- ヨルダン

- ラテンアメリカ

- ブラジル

- ペルー

- チリ

- アルゼンチン

第10章 企業プロファイル

- ABB

- Alconza

- ANDRITZ

- Ansaldo Energia

- CG Power &Industrial Solutions

- Elin Motoren

- EvoTec Power Generation

- GE Vernova

- Ingeteam

- Jeumont Electric

- Koncar

- Marelli Motori

- Mecc Alte

- Meidensha Corporation

- MENZEL ELEKTROMOTOREN

- Nidec

- PARTZSCH Group

- POWERTEC GENERATOR SYSTEM

- Schneider Electric

- Siemens Energy

- TD Power Systems

- TMEIC

- WEG

- Wolong Electric Group

The Global Synchronous Generator Market was valued at USD 6.8 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 11 billion by 2034. Increasing emphasis on energy-efficient technologies and the rising need for high-performance, reliable power infrastructure are key factors fueling market expansion. Growth in renewable energy projects, combined with advancements in insulation and material science, continues to shape the evolution of this sector. Synchronous generators are integral to modern power systems, offering consistent voltage and frequency that support the stability of electrical grids. Their use is becoming more dynamic, extending from conventional backup roles to active components in distributed and peak-load energy systems.

As global power demands surge, the integration of intelligent generator systems equipped with IoT features is transforming operational models. These next-generation generators support remote diagnostics, predictive maintenance, and energy optimization-all crucial in modern energy frameworks. Escalating concerns over energy reliability, coupled with upgrades to aging infrastructure and greater frequency of grid disruptions, are also accelerating the adoption of these systems. Growing emphasis on sustainability and regulatory compliance is pushing innovation in design, control features, and smart connectivity, making these machines indispensable across a wider range of industries and applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.8 Billion |

| Forecast Value | $11 Billion |

| CAGR | 4.9% |

The generators segment accounted for a 40.6% share in 2024 and is projected to grow at over 4.5% CAGR by 2034. Their strong performance, ease of maintenance, and dependable output make them ideal for a range of operational scenarios. The segment's continued relevance lies in its adaptability and cost-effectiveness for diverse end-user requirements.

The Units with a power rating of <= 5 MVA are expected to grow at a CAGR of 5% through 2034, driven by their increasing use in decentralized power setups, backup systems, and small to mid-sized industrial applications. Enhancements such as intelligent control systems, upgraded cooling features, and remote monitoring interfaces are helping to expand their role in modern power ecosystems.

Asia Pacific Synchronous Generator Market held a 37.5% share in 2024. Accelerating industrial activity, together with large-scale investment in energy generation infrastructure, is fostering growth in the region. The shift toward distributed generation and smart microgrids is adding further momentum, especially as local governments roll out demand-response programs and invest in power grid resilience.

Key players in the Global Synchronous Generator Market include TMEIC, POWERTEC GENERATOR SYSTEM, Siemens Energy, Meidensha Corporation, Wolong Electric Group, ABB, Alconz, PARTZSCH Group, Schneider Electric, WEG, TD Power Systems, EvoTec Power Generation, Ingeteam, Marelli Motori, Elin Motoren, GE Vernova, Nidec, Jeumont Electric, ANDRITZ, MENZEL ELEKTROMOTOREN, Ansaldo Energia, Koncar, CG Power & Industrial Solutions, and Mecc Alte. Leading companies in the synchronous generator market are investing heavily in advanced product development, targeting digital transformation with smart connectivity and IoT-enabled systems. Many firms are expanding their geographic footprint by strengthening local production capabilities and service networks, especially in high-growth markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1.1 Raw material availability & sourcing analysis

- 3.1.1.2 Manufacturing capacity assessment

- 3.1.1.3 Supply chain resilience & risk factors

- 3.1.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of synchronous generator

- 3.8 Emerging opportunities & trends

- 3.9 Digital transformation with IoT technologies

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Prime Mover, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Gas turbine

- 5.3 Steam turbine

- 5.4 Reciprocating engine

- 5.5 Others

Chapter 6 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Single phase

- 6.3 Three phase

Chapter 7 Market Size and Forecast, By Power Rating, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 ≤ 5 MVA

- 7.3 > 5 MVA - 15 MVA

- 7.4 > 15 MVA - 30 MVA

- 7.5 > 30 MVA - 50 MVA

- 7.6 > 50 MVA

Chapter 8 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Industrial

- 8.3 Utility

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 Russia

- 9.3.4 UK

- 9.3.5 Italy

- 9.3.6 Spain

- 9.3.7 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.4.6 New Zealand

- 9.4.7 Malaysia

- 9.4.8 Indonesia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Egypt

- 9.5.5 South Africa

- 9.5.6 Nigeria

- 9.5.7 Turkey

- 9.5.8 Jordan

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Peru

- 9.6.3 Chile

- 9.6.4 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Alconza

- 10.3 ANDRITZ

- 10.4 Ansaldo Energia

- 10.5 CG Power & Industrial Solutions

- 10.6 Elin Motoren

- 10.7 EvoTec Power Generation

- 10.8 GE Vernova

- 10.9 Ingeteam

- 10.10 Jeumont Electric

- 10.11 Koncar

- 10.12 Marelli Motori

- 10.13 Mecc Alte

- 10.14 Meidensha Corporation

- 10.15 MENZEL ELEKTROMOTOREN

- 10.16 Nidec

- 10.17 PARTZSCH Group

- 10.18 POWERTEC GENERATOR SYSTEM

- 10.19 Schneider Electric

- 10.20 Siemens Energy

- 10.21 TD Power Systems

- 10.22 TMEIC

- 10.23 WEG

- 10.24 Wolong Electric Group