|

市場調査レポート

商品コード

1907212

インドの水処理薬品市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)India Water Treatment Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの水処理薬品市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

概要

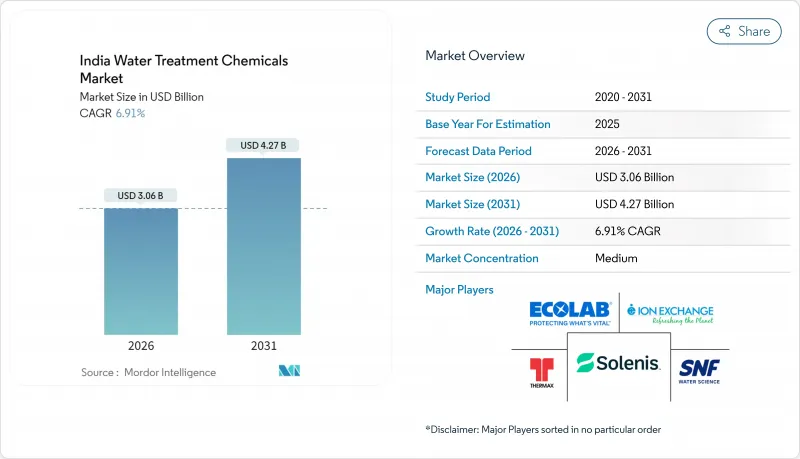

2026年のインド水処理薬品市場規模は30億6,000万米ドルと推定され、2025年の28億6,000万米ドルから成長し、2031年には42億7,000万米ドルに達すると予測されています。

2026年から2031年にかけての年間平均成長率(CAGR)は6.91%となる見込みです。

ジャル・ジーヴァン・ミッションの迅速な実施、ゼロ液体排出(ZLD)義務の拡大、産業用水リサイクルの推進が相まって、自治体および産業ユーザー双方からの化学薬品需要が高まっています。すでに9,930万世帯に供給されている農村部の水道接続数の急増により、自治体の調達需要は堅調に推移しています。一方、繊維・製薬・発電プラントでは、凝集剤・スケール防止剤・腐食防止剤を基盤とする高度処理システムの導入が拡大し、効率性向上を図っております。特殊原料の価格変動に伴う供給リスクは継続するもの、国内生産能力の増強と地元供給業者への優先調達政策により、価格急騰は抑制されております。顧客がライフサイクルコスト削減と規制順守の確実性を重視する中、酵素系化学品やデジタル投与制御技術といった技術的差別化が、利益率拡大の決定的要因となっております。

インド水処理薬品市場の動向と洞察

処理済み工業用水・上水への需要増加

産業生産量の拡大と排出基準の厳格化により、工場では処理水1リットル当たりの処理薬品消費量が増加しています。火力発電所では高温で稼働する凝縮水ライン保護のため高性能腐食防止剤に依存し、化学プラントでは特注スケール防止剤・洗浄剤を必要とする膜バイオリアクターを導入しています。都市水道事業者は老朽化した配管と一人当たり需要の増加に直面し、長距離配水網全体での水質維持のため塩素処理負荷の強化と二次消毒を実施しています。企業の環境管理プログラムが市場機会を拡大しています。ITC社の「水資源に積極的な」事業活動(147万エーカーの流域プロジェクトをカバー)では、複数の拠点で凝集剤やpH調整剤の持続的な採用が実証されました。これらの動向が相まって、インドの水処理薬品市場は、水インフラ容量の基盤的拡大を上回る成長を遂げています。

政府主導の設備投資(ジャル・ジーヴァン計画およびナマミ・ガンジ計画)

605億3,000万米ドルのジャル・ジーヴァン予算により、化学薬品供給を長期運営パッケージに組み込んだ567件の稼働プロジェクトが創出されました。チャンバル・アルワル・バラトプル計画などのハイブリッド年金方式入札では、複数年にわたる薬剤供給契約が組み込まれており、ミョウバン、塩素、特殊ポリマーの安定した需要が保証されています。ナマミ・ガンジ計画に基づく並行施策では三次栄養塩除去が要求され、残留リンをより厳密に制御する凝集剤の販売を促進しています。入札評価において国内供給業者を優遇する優先条項により、インドのメーカーは生産拡大、キャッシュフローの安定化、研究開発投資の余地を得ています。新規プラントは稼働開始後24時間365日稼働するため、各配分は年金のような収益源を創出し、インドの水処理薬品市場の長期的な拡大を加速させます。

従来の殺菌剤をめぐる環境・健康上の懸念

規制当局は、受水域に持続性副生成物を形成する塩素系消毒剤の使用を段階的に削減しています。中央公害管理局(CPCB)のガイドライン草案では、遊離残留塩素の制限を推奨し、生分解性代替品の採用を促すことで、水道事業者を過酢酸または二酸化塩素混合物への移行へと導いています。この移行により、処理水1リットルあたりのコストが15~20%上昇し、供給業者には再配合が迫られ、切り替え期間中の性能不安定性が生じます。製品接触リスクに敏感な食品・飲料加工業者は低残留オプションの早期採用者ですが、その厳格な品質プロトコルが検証サイクルを延長し、切り替え決定を遅らせています。結果として、全体的な成長にもかかわらず、代替化学物質が規制適合性と費用対効果の両方を証明するまで事業者が設備投資を遅らせるため、インドの水処理薬品市場は一部の上昇余地を失っています。

セグメント分析

2025年時点で、腐食・スケール防止剤はインド水処理薬品市場の31.72%を占め、過酷な水質に晒される資本集約型資産を保護する役割を強調しています。火力発電所では軟鋼製凝縮器を保護するため、皮膜形成アミンやリン酸塩混合物を添加し、都市水道局では旧式配管からの鉛溶出を抑制するため正リン酸塩を注入しています。プログラムが有効性が確認されると、運用者がサイクル途中で薬剤を変更することは稀であるため、需要の見通しが良好です。このセグメントにおけるインド水処理薬品市場規模は、高い塩化物攻撃率に直面し、高品質合金保護剤を必要とする新規沿岸海水淡水化プラントの増加に伴い拡大が見込まれます。

凝集剤および凝集助剤は、ベースは小さいもの、2031年までにCAGR7.58%を記録しており、製品カテゴリー内で最速の成長を示しています。清澄装置-UF-ROラインを導入する繊維工場では、連続投与が推奨されています:濁度低減のためのPAC投与後、カチオン性ポリアクリルアミドでマイクロンサイズの微粒子を凝集させます。自治体による汚泥削減プログラムも追い風となり、処理量を削減する高電荷ポリエレクトロライトが好まれています。予測期間中、シリカ含有量の高い水向けに設計された膜洗浄剤および特殊スケール防止剤は、ニッチながら高利益率のサブセグメントとして台頭し、インド水処理薬品市場におけるプロセス特化型カスタマイズの深化を反映しています。

インド水処理薬品レポートは、製品タイプ別(殺菌剤・消毒剤、凝集剤・凝集助剤、腐食・スケール防止剤、消泡剤・消泡助剤など)、エンドユーザー産業別(電力、石油・ガス、化学製造、鉱業・鉱物加工、自治体、食品・飲料、パルプ・製紙、その他エンドユーザー産業)に分類されています。市場予測は金額ベース(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 処理済み工業用水および上水に対する需要の増加

- 政府主導の設備投資(ジャル・ジーヴァン計画及びナマミ・ガンジ計画)

- 繊維・製薬業界におけるより厳格なゼロ液体排出(ZLD)規制

- 地下水採取抑制に向けた産業用水リサイクルの拡大

- 高度酸化処理および酵素ベース化学技術の導入

- 市場抑制要因

- 従来の殺菌剤に関する環境・健康上の懸念

- 中小規模の公益事業体および中小零細企業向け排水処理プラントにおける高い運用コスト

- 特殊化学品原料価格の変動性(中国供給源のシフト)

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の激しさ

第5章 市場規模と成長予測

- 製品タイプ別

- 殺菌剤および消毒剤

- 凝集剤および凝集助剤

- 腐食・スケール防止剤

- 消泡剤および消泡剤(アンチフォーム)

- pH調整剤

- その他の製品タイプ

- エンドユーザー業界別

- 電力

- 石油・ガス

- 化学製造

- 鉱業および鉱物加工

- 自治体

- 食品・飲料

- パルプ・製紙

- その他のエンドユーザー産業

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- Accepta Water Treatment

- Atul Ltd

- Aquatech

- Chembond Water Technologies Limited

- Dow

- Ecolab Inc.(Nalco Water)

- IEI

- Kemira

- Kurita Water Industries Ltd.

- Nouryon

- Pentair

- SicagenChem

- SNF

- Solenis

- Syensqo

- Thermax Limited

- VASU CHEMICALS LLP

- Veolia