|

市場調査レポート

商品コード

1686274

大口径弾薬:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Large Caliber Ammunition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 大口径弾薬:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

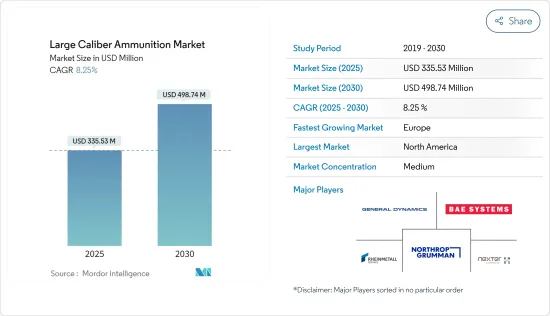

大口径弾薬市場規模は2025年に3億3,553万米ドルと推定され、予測期間(2025年~2030年)のCAGRは8.25%で、2030年には4億9,874万米ドルに達すると予測されます。

COVID-19のパンデミックが市場に与えた影響はごくわずかでした。これは主に、世界の主要国の国防費が増加したことに起因します。2021年時点の軍事費は2兆1,000億米ドルと評価され、米国の支出が最も高く、中国とインドがこれに続きます。さらに、ロシアとウクライナの間で進行中の戦争は、武器と弾薬の使用の増加につながり、NATO諸国からの防衛支出の増加は、欧州全体の市場成長を推進しています。このように、この地域の国々間の地政学的紛争の増加は、大口径武器・弾薬への防衛支出を促進し、市場を牽引する上で大きな役割を果たしました。

世界各国の政府は、陸海空の国境警備、民間人保護、軍隊の殺傷力を強化するため、野砲、迫撃砲、艦砲などの兵器への投資を行っています。これらの兵器は、地上攻撃作戦に使用される高価なミサイルやロケットよりも費用対効果の高い選択肢です。こうした要因が大口径弾薬の需要を世界的に押し上げています。

高速発射、レーザー誘導システム、敵味方識別や精密照準技術に対するニーズの高まりなどの大幅な技術進歩が、GPS対応砲弾および迫撃砲弾の市場成長を後押ししています。政治的紛争、テロリズム、国境を越えた紛争の増加により、部隊の迅速な展開の必要性が高まり、同時に戦場での火力支援の需要が高まり、大口径弾薬の市場成長を促進しています。

大口径弾薬市場の動向

地上軍セグメントは予測期間中に最も高いCAGRで成長すると予測される

国際戦略情勢の大きな変化に伴い、国際安全保障システムの構成は、覇権主義、単独主義、パワーポリティクスの高まりによって損なわれ、現在進行中のいくつかの国際紛争に拍車をかけています。領土権の不確実性、政治的緊張、軍事大国間の普遍的優位の追求が、地政学的シナリオを乱す主な原因です。

この点で、各国政府の最も一般的な反応は、自国の安全保障を向上させるために軍事費を増やすことです。COVID-19パンデミックの経済的影響にもかかわらず、世界の国防支出は2020年と2021年も伸び続けた。SIPRIによると、2021年の世界の軍事費は2020年から7%増の2兆1,130億米ドルに達しました。2021年の世界の支出は2012年より19%増加しました。2021年の5大軍事支出国は米国、中国、インド、英国、ロシアで、世界の軍事支出の62%を占めました。米国、英国、中国、インドなどの軍事大国は、軍事火力と防衛力の増強に注力してきました。膨大な予算はまた、敵対勢力と交戦し脅威を無力化するための新しい武器・弾薬システムの研究開発を促進します。

いくつかの軍隊は、車両搭載兵器、艦砲システム、迫撃砲、榴弾砲の購入など、軍事火力能力のアップグレードに多大な資源を投入しています。このため、関連弾薬の需要が世界的に高まっています。例えば、2021年9月、エストニア国防軍は、今後数年間で8,000万ユーロ相当の大口径・小口径弾薬を受領すると発表しました。この調達計画では、国防軍は今後4~8年間で8つのサプライヤーから3,000万ユーロ相当の大口径弾薬を受け取ることになります。

予測期間中、北米が市場をリードする見通し

米国は世界最大の国防支出国です。米国の国防費は、2020年の7,782億3,000万米ドルから2021年には8,010億米ドルに達し、ほぼ2.9%増加しました。米国は2021年も最大の国防支出国であり続け、世界の支出額の38%を占めました。2022年度の国防総省の予算権限は、2020年の7,050億米ドルから170億米ドル増の約7,220億米ドルであり、2023年度の大統領予算要求は7,730億米ドルでした。この予算は主に、空、海、陸の戦闘領域における能力の近代化と、国の競争優位性を強化するための技術革新を目的としています。

2022年の国防次官報告では、米国軍は2023年度にミサイルと軍需品に247億米ドルの予算を要求しています。その主な目的は、ハイエンドの戦闘に不可欠な需要の高い武器と軍需品について、利用可能な産業能力を十分に活用し、高い生産率で調達することによって、部隊の全体的な殺傷力を高めることです。さらに2023年度には、防衛予算の9%をミサイルと弾薬に配分することが要求されています。弾薬のポートフォリオには、弾丸、カートリッジ、迫撃砲、爆薬、砲弾など、主に地上部隊が必要とするものが含まれます。このような防衛プラットフォームと関連弾薬の調達計画は、予測期間中に北米で調査された市場を牽引すると予想されます。例えば、米国はウクライナに提供するために韓国の兵器メーカーから10万発の155mm榴弾砲弾薬を購入する予定です。

大口径弾薬産業の概要

大口径弾薬市場は、さまざまな軍に供給される弾薬の少数の既存企業と現地メーカーで適度に統合されています。著名な市場企業には、ゼネラル・ダイナミクス、BAEシステムズ、ノースロップ・グラマン、ラインメタルAG、ネクスター・グループKNDSなどがあります。設計、材料、殺傷力などにおける革新が市場を牽引しています。非公開会社は、現地の民間・政府系弾薬会社の強化に力を入れています。サウジアラビア、アラブ首長国連邦、中国、インドなどの国々は、それぞれの軍隊の必要性に応えるため、地元の製造会社を奨励しており、それによって地元企業の市場シェア拡大に貢献しています。

例えば、2022年5月、米国陸軍は120mm戦車訓練弾薬を調達するための2つの契約を発表しました。陸軍は、120 mm M1002多目的戦車訓練弾、120 mm M865A1新製造運動エネルギー弾、M1002弾薬について、6,670万米ドル相当の契約をノースロップ・グラマンに発注しました。また、米国陸軍は、120mm M865A1新製造運動エネルギー弾および120mm M1002新製造多目的戦車訓練弾について、5,080万米ドルの契約をジェネラル・ダイナミクス・コーポレーションに発注しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 口径タイプ別

- 40~60mm

- 60mm以上

- エンドユーザー別

- 海軍

- 地上軍(空軍、陸軍、特殊部隊、国境警備、連邦政府機関など)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- General Dynamics Corporation

- BAE Systems PLC

- Rheinmetall AG

- Nexter group KNDS

- Northrop Grumman

- ST Engineering

- Saab AB

- Ukroboronprom

- Denel SOC Ltd

- Nammo AS

- Global Ordnance

- Diehl Stiftung & Co. KG

- Leonardo SpA

- Raytheon Technologies Corporation

第7章 市場機会と今後の動向

The Large Caliber Ammunition Market size is estimated at USD 335.53 million in 2025, and is expected to reach USD 498.74 million by 2030, at a CAGR of 8.25% during the forecast period (2025-2030).

The COVID-19 pandemic had a negligible impact on the market. This is mainly attributed to the increase in defense expenditure across major world powers. The military expenditure as of 2021 was valued at USD 2.1 trillion, with the United States spending the highest, followed by China and India. Furthermore, the ongoing war between Russia and Ukraine leads to the rising use of weapons and ammunition, and growing defense expenditure from NATO countries drives market growth across Europe. Thus, the growth in geopolitical conflicts among the countries of the region played a major role in driving defense spending toward large-caliber weapons and ammunition, driving the market.

Governments across the world are making investments in weapons, such as field artillery, mortars, naval guns, etc., to strengthen the land and maritime border security, civilian protection, and lethality of armed forces. These weapons are a cost-effective option over costly missiles and rockets used for ground attack operations. These factors are driving the demand for large-caliber ammunition globally.

Significant technological advancements, such as high-speed projectile firing, laser guidance systems, and the increasing need for friend or foe identification and precision targeting technology, drive the market growth for GPS-enabled artillery and mortar shells. Due to increased political disputes, terrorism, and cross-border conflicts, the need for rapid deployment of forces has increased, simultaneously increasing the demand for firepower support on the battlefield, driving the market growth for large-caliber ammunition.

Large Caliber Ammunition Market Trends

Ground Forces Segment is Projected to Grow with Highest CAGR During the Forecast Period

Owing to profound changes in the international strategic landscape, the configuration of international security systems has been undermined by the growing hegemonism, unilateralism, and power politics, which have fuelled several ongoing global conflicts. Uncertainties in territorial rights, political tensions, and the quest for universal dominance among the military powerhouses are the major causes disturbing the geopolitical scenario.

In this regard, the most common reaction of the governments is to increase their military spending to improve security in their respective countries. Despite the economic impact of the COVID-19 pandemic, global defense expenditure continued to grow in 2020 and 2021. According to SIPRI, the global military expenditure in 2021 rose to USD 2113 billion, an increase of 7% from 2020. billion. Global spending in 2021 was 19% higher than in 2012. The five largest military spenders in 2021 were the United States, China, India, the United Kingdom, and Russia, which accounted for 62% of world military spending. Military powerhouses, such as the United States, United Kingdom, China, and India, have been focused on augmenting their military firepower and defensive capabilities. The colossal budgets also facilitate the R&D of new weapon and ammunition systems to engage hostile forces and neutralize threats.

Several armed forces have invested significant resources in upgrading their military firepower capabilities, including purchasing vehicle-mounted weapons, naval gun systems, mortars, and howitzers. This has been increasing the demand for related ammunition globally. For instance, in September 2021, the Estonian Defense Forces announced that it would receive large and small caliber ammunition worth EUR 80 million in the next few years. Under the procurement plan, the defense forces would receive large caliber ammunition worth EUR 30 million from eight suppliers over the next four to eight years.

North America is Expected to Lead the Market During the Forecast Period

The United States is the largest defense spender in the world. The US defense expenditure increased by almost 2.9% in 2021 to reach USD 801 billion from USD 778.23 billion in 2020. The United States remained the largest defense-spending country in 2021 and represented 38% of global spending. For FY 2022, the Department of Defense's budget authority is approximately USD 722 billion, an increase of USD 17 billion from USD 705 billion in 2020, while the FY 2023 President's budget request was USD 773 billion for the DoD. The budget primarily aims at modernizing capabilities in the air, maritime, and land warfighting domains and on innovations to strengthen the country's competitive advantage.

In the 2022 report of the Under Secretary of Defense, the United States military has requested a budget of USD 24.7 Billion in FY 2023 for missiles and munitions with a prime objective to increase the overall lethality of the force by procuring at high rates of production, fully utilizing the available industrial capacity for high demand weapons and munitions that are essential for the high-end combat. Furthermore, in FY 2023, 9% of the defense budget is requested to allocate toward missiles and munitions. The ammunition portfolio includes bullets, cartridges, mortars, explosives, and artillery projectiles needed mostly by ground forces. Such procurement plans for defense platforms and related ammunition are anticipated to drive the market studied in North America during the forecast period. For instance, the United States plans to buy 100,000 rounds of 155mm howitzer ammunition from South Korean arms manufacturers to provide to Ukraine.

Large Caliber Ammunition Industry Overview

The market for large-caliber ammunition is moderately consolidated with few established players and local manufacturers of the ammunition supplied to various armed forces. Some prominent market players are General Dynamics, BAE Systems, Northrop Grumman, Rheinmetall AG, and Nexter group KNDS. Innovations in design, materials, lethality, etc., drive the market. Several companies are focusing on strengthening their local private and government-owned ammunition companies. Countries like Saudi Arabia, the United Arab Emirates, China, and India, are encouraging local manufacturing companies to cater to the need of their respective armed forces, thereby helping the local companies to increase their share in the market studied.

For instance, in May 2022, the United States army announced two contracts to procure 120 mm tank training ammunition. The Army awarded a contract worth USD 66.7 million to Northrop Grumman for 120 mm M1002 multi-purpose tank training rounds, 120 mm M865A1 new production kinetic energy rounds, and M1002 ammunition. Also, the US Army awarded another contract worth USD 50.8 million to General Dynamics Corporation for 120mm M865A1 new production kinetic energy rounds and 120 mm M1002 new production multi-purpose tank training rounds.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Caliber Type

- 5.1.1 40-60 mm

- 5.1.2 Above 60 mm

- 5.2 By End User

- 5.2.1 Naval Forces

- 5.2.2 Ground Forces (Air Force, Army, Special Forces, Border Security, Federal Agencies, etc.)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 General Dynamics Corporation

- 6.2.2 BAE Systems PLC

- 6.2.3 Rheinmetall AG

- 6.2.4 Nexter group KNDS

- 6.2.5 Northrop Grumman

- 6.2.6 ST Engineering

- 6.2.7 Saab AB

- 6.2.8 Ukroboronprom

- 6.2.9 Denel SOC Ltd

- 6.2.10 Nammo AS

- 6.2.11 Global Ordnance

- 6.2.12 Diehl Stiftung & Co. KG

- 6.2.13 Leonardo SpA

- 6.2.14 Raytheon Technologies Corporation