|

市場調査レポート

商品コード

1851380

メタノール:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Methanol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| メタノール:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月28日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

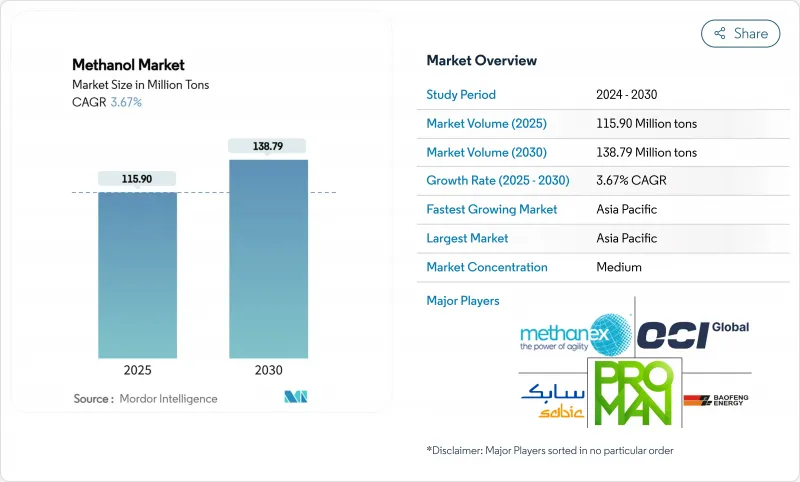

メタノール市場規模は2025年に1億1,590万トンと推定され、2030年には1億3,879万トンに達すると予測され、予測期間(2025-2030年)のCAGRは3.67%です。

大まかな数字には、地域的なコントラストが隠されている:大西洋流域の価格は計画外の停電を経て堅調に推移したが、アジアのスポット価格は軟化し、トレーダーの裁定取引の窓を広げました。中国の対オレフィン(MTO)生産能力の拡大、北米の「メガ・メガ」プラント、海洋燃料需要の急増が、成長シナリオの軸となっています。再生可能なメタノールプロジェクトは、大きなアップサイドをもたらすが、認証の遅れとインフラのギャップが、当面の供給構築を制限します。しかし、低炭素生産と海運転換への持続的投資が、メタノール市場の中期的な安定軌道を支えています。

世界のメタノール市場の動向と洞察

中国、米国、新興アジアにおける石油化学生産能力の拡大

2024年に中国の総合コンビナートで1,480万B/Dという記録的な原油処理能力を達成することで、精製業者が化学原料に軸足を移しているため、メタノールの需要が高まっています。同時に、米国の「メガ・メガ」メタノールプラントは、中国のMTOユニットに供給されるように設計されており、従来の貿易の流れを変える太平洋横断バリューチェーンを形成しています。アジアの新興生産者はこのモデルを模倣しており、石炭からメタノールへの投資がいくつか建設中です。これらのプロジェクトは総体として地域の自給率を引き上げるが、同時に、需要の増加をメタノール市場のファンダメンタルズにしっかりと結びつけておきます。このダイナミックな動きは、2030年までに約800万トンの新たな消費を追加し、アジア太平洋の世界収支における中心性を確固たるものにすると予想されます。

海洋セクターの低炭素燃料への移行

2023年には、メタノール対応船138隻が発注され、LNG対応船130隻を上回りました。2025年初頭には、発注隻数はさらに23隻増加し、マースクなどの大手輸送会社は、2027年までに25隻のデュアル燃料コンテナ船の就航を目標としており、毎年150万トンのCO2を削減できる可能性があります。再生可能なメタノールは、ライフサイクルの温室効果ガス排出量を最大95%削減することができ、IMOの2024年ライフサイクル原単位ガイドラインに適合しています。船舶の急速な採用ペースは、実現した燃料供給を上回っており、堅調な需要期待を下支えし、メタノール市場への長期的な牽引力を強めています。

原料価格の変動

地政学的緊張が欧州とアジアのLNGベンチマークに影響を与え、輸入に依存する地域のメタノール生産コストが上昇したため、天然ガス価格は2024年に大きく変動しました。特に欧州では、ガス供給が確保されていない生産者は、北米や中東のプラントと比較してマージンが圧縮される事態に直面しました。メタノール市場は、天然ガスが依然として原料の65%を占めているため、こうした変動にさらされています。ボラティリティはまた、新規設備の投資決定を複雑にし、川下バイヤーの価格透明性を阻害しています。ヘッジ戦略や統合戦略によってリスクは一部相殺されるもの、不安定な状況が続くと、短期的な成長見通しが弱まることになります。

セグメント分析

2024年には天然ガスが全原料の65%を占める。ヘインズビル地域とパーミアン地域での堅調なシェール生産がコスト競争力のある生産を支え、メタノール市場規模の信頼できる供給を保証しています。バイオメタノールとe-メタノールを合わせた再生可能な経路は、2030年までに3,570万トンの潜在容量を持つ210のプロジェクトが発表されており、メタノール産業における転換の兆しを示しています。

天然ガスは、2030年まで主要な供給原料であり続けると予測されるが、認証されたグリーンな代替原料が海運や化学の顧客からプレミアムを獲得するにつれて、そのシェアは徐々に縮小していきます。メタノール市場は、この2つの成長軌道から利益を得ています。従来型の企業は原料の優位性を生かし、再生可能技術をいち早く採用した企業はより高いマージンとブランド差別化を獲得しています。

MTO、ガソリン混合燃料、船舶用燃料を含むエネルギー関連用途は、2024年の消費量の54%を占め、メタノール市場力学への影響力を際立たせています。中国におけるメタノールからオレフィンへのブームだけで、2024年には400万トンが追加的に吸収され、この地域の世界貿易への影響力が強化されます。

現在、トン数では控えめだが、船舶用燃料需要は大きなシェアを占めています。デュアルフューエルの発注トン数は、2030年までに年間700万トンのバンカー需要が追加されることを示唆しており、海洋用途のメタノール市場規模が既存のエネルギー用途に匹敵する可能性があることを示しています。メタノールは燃料や化学品に汎用性があるため、周期的な変動をスムーズにし、この分野の回復力を高めています。

地域分析

アジア太平洋地域は、2024年のメタノール消費量の78%(約90,400キロトン)を占める。中国の石炭からオレフィンへの転換、インドネシアのバイオディーゼルB40の展開、東南アジアの生産能力増強計画により、この地域のリーダーシップは確固たるものとなります。アジア太平洋のメタノール市場規模は、海運と再生可能燃料による新たな需要ノードが石油化学の必要量を増加させるため、2030年までCAGR 3.86%で成長すると予測されます。アジア太平洋地域の価格は依然として中国の輸入平価と密接に結びついており、この地域は世界的なセンチメントの指標となっています。

メタノール市場における北米の役割は変容しつつあります。豊富なシェールガスは、ルイジアナ州にあるレイクチャールズメタノールの32億米ドルの複合施設に代表される輸出志向のプロジェクトの波を支えています。かつては主に国内のホルムアルデヒド向けであった米国の生産量は、現在ではアジアのMTOバイヤーに向けられ、貿易回廊が再編成され、裁定取引のオプション性が提供されています。

欧州と中東では、戦略が異なっています。欧州は、「Fit for 55」目標を達成するためにe-メタノールに投資を行い、Forestal del Atlanticoのスペイン工場のようなプロジェクトは、船舶用バンカーをターゲットとしています。逆に中東は、従来の天然ガスベースの施設を倍増させ、アジアに供給するための原料の優位性を活用しています。これらの地域が一体となって、低炭素化プレミアムを追い求める側と、コスト・リーダーシップを最大限に発揮する側という、ますます二分化されたメタノール市場を形成しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 中国、米国、新興アジアで拡大する石油化学生産能力

- 海洋セクターの低炭素燃料への移行ーグローバル船社によるグリーンメタノールの採用

- ASEANとLATAMにおける混合燃料に関する政府の義務化メタノールガソリンとDMEの促進

- オレフィン生産におけるメタノールの利用拡大

- プロピレンの供給不足が中東のメタノールベースの需要を強化

- 市場抑制要因

- 原料価格の変動

- グリーンメタノールの認証枠組みの遅れがオフテイク契約を制限

- 健康への有害影響

- バリューチェーン分析

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 主要原料別生産能力分析

- 貿易フロー分析

- 価格動向と予測

第5章 市場規模と成長予測

- 原料別

- 天然ガス

- 石炭

- 再生可能原料(バイオマス、固形廃棄物)

- その他(CO2、グリーン水素、石油残渣、ナフサ)

- 誘導体別/用途別

- 伝統的化学品

- ホルムアルデヒド

- 酢酸

- 溶剤

- メチルアミン

- その他の伝統的化学品

- エネルギー関連

- メタノールーオレフィン(MTO)

- メチルtert-ブチルエーテル(MTBE)

- ガソリン混合

- ジメチルエーテル(DME)

- バイオディーゼル

- 伝統的化学品

- 最終用途産業別

- 自動車・運輸

- 化学品

- 海上燃料

- その他(電子・家電、発電)

- グレード別

- 化学グレード

- 燃料グレード

- その他(ウルトラクリーン/バッテリーグレード、再生可能燃料(バイオ/Eメタノール))

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ベトナム

- タイ

- インドネシア

- マレーシア

- オーストラリア

- ニュージーランド

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- トルコ

- ロシア

- 北欧諸国

- スペイン

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- イラン

- 南アフリカ

- ナイジェリア

- エジプト

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Atlantic Methanol

- BASF SE

- Carbon Recycling International(CRI)

- Celanese Corporation

- China National Chemical Corporation(ChemChina)

- Coogee

- Enerkem

- Eni S.p.A.

- Gujarat State Fertilizers & Chemicals Limited(GSFC)

- INEOS

- Kaveh Methanol Company

- Kingboard Holdings Limited

- LyondellBasell Industries Holdings B.V.

- Methanex Corporation

- MITSUBISHI GAS CHEMICAL COMPANY, INC

- Natgasoline

- Ningxia Baofeng Energy Group

- OCI

- Petroliam Nasional Berhad(PETRONAS)

- Proman

- SABIC

- Yankuang Energy

- ZPC Integrated Refining & Petrochemical(Zhejiang)