集光型太陽熱発電(CSP)-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Concentrated Solar Power (CSP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685930

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

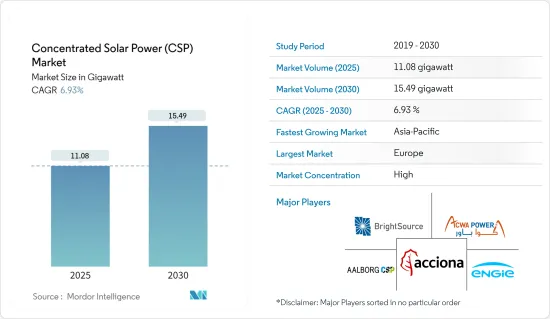

集光型太陽光発電市場規模は2025年に11.08ギガワットと推定され、予測期間(2025年~2030年)のCAGRは6.93%で、2030年には15.49ギガワットに達すると予測されます。

主なハイライト

- 長期的には、集光型太陽光発電技術のコスト低下が市場を牽引すると予想されます。

- 一方、太陽光発電やその他の再生可能技術の採用が増加していることが、予測期間中の市場成長の妨げになると予想されます。

- とはいえ、技術の改善やハイブリッド発電所への集光型太陽光発電の統合は、環境にプラスの影響を与えます。これは環境にプラスの影響を与え、気候変動は将来的に集光型太陽光発電市場にいくつかの機会を生み出すと予想されます。

- 同地域の太陽電池セクターでは、電力需要の増加に伴い新規プロジェクトが立ち上がり、汚染レベルを抑制するために再生可能エネルギー源の利用に注力しているため、予測期間中にCSPの需要が増加することになり、欧州が市場を独占すると予想されます。

集光型太陽熱発電(CSP)市場動向

パラボリックトラフ型が市場を独占

- パラボリックトラフ型集光装置(PTC)は、直線軸追尾式の長いU字型ミラーで構成されています。ミラーは焦点線に沿って直射日光を反射し、そこに吸収管が配置されます。レシーバー/アブソーバー・チューブはスチール製です。太陽スペクトルの波長域では高い吸光度を維持し、赤外スペクトルの波長域では高い反射率を維持する(i.i.は可能な限り放出しない)選択コーティングが施されています。

- 最も一般的に使用される流体はサーマルオイルだが、水/蒸気や溶融塩もこの構成に使用されます。これらは、CSPとして最も広く導入されている構成です。

- パラボラトラフ型集熱器は、世界中で最も一般的に導入されているCSPのひとつであり、家庭用暖房、海水淡水化、冷凍システム、産業用熱、発電所、灌漑用水の揚水などに導入されています。米国国立再生可能エネルギー研究所(NREL)によると、2022年6月現在、パラボリック・トラフは世界のCSP設備容量の63.5%を占めています。

- パラボリック・トラフ・コレクター(PTC)の運転・保守部分は、同種のものと比べてやや複雑です。ソーラーフィールドの運用とメンテナンスに関する最も頻繁な活動は、ミラーの反射率の定期的な測定と洗浄です。ミラーの反射率は、ソーラーコレクターが供給する貴重な熱エネルギーの量に直接影響します。また、定期的な洗浄やメンテナンスを行うには、背の高い車やクレーンが必要になることもあります。

- 例えば2020年、インド工科大学マドラス校の研究者は、海水淡水化、空間暖房、空間冷房などの産業用途の太陽エネルギーを集光するための低コストのソーラー・パラボラトル・トラフ・コレクター(PTC)装置を開発しました。インドで開発されたこのシステムは軽量で、さまざまな気候や負荷状況下で高い効率を発揮します。

- したがって、予測期間中はパラボラトラフが集光型太陽熱発電市場を独占すると予想されます。

市場を独占する欧州

- 欧州では、電力部門が温室効果ガス排出量の75%以上を占めています。再生可能エネルギーの割合を増やすことは、気候変動に対処するための潜在的な選択肢となっています。

- ソーラー部門は、電力需要の増加に伴い新規プロジェクトを立ち上げ、地域全体の汚染レベルを抑制するために再生可能エネルギー源の利用に注力しています。2022年、欧州のCSP設備容量は約230万kWでした。IRENAによれば、2030年までに欧州では400万kWの集光型太陽光発電(CSP)が設置される見込みです。

- 欧州では、MUSTEC(太陽熱発電の市場導入)のようなエネルギー協力が、EUの2030年の気候・エネルギー枠組みを踏まえ、同地域におけるCSPプロジェクトの共同開拓に重点を置くことを意図しています。MUSTECは、中欧・北欧諸国の電力需要を満たすために、南欧でCSPプロジェクトを展開することを目指しています。

- 同様に、CSP/太陽熱エネルギーのための欧州研究基盤であるEUソラリスERICは、CSPの研究関連活動と応用開発を目的としています。ツールや技術の開発、新たな能力、ソリューション、日常的な基準、プロトコルを開発し、この地域のCSP技術を強化します。

- さらに2022年、ドイツ政府は産業用途のグリーン暖房へのクリーンエネルギー転換を加速させるため、CSP設置に55%の補助金を導入しました。また、CSP技術の投資回収期間を3年以下に引き下げることも想定しています。これは、ドイツにおけるCSP導入の増加に大きく貢献すると思われます。

- 同様に、スペインは2002年に欧州で初めてCSPの固定価格買取制度を導入し、CSPの導入拡大に貢献しました。さらにスペインは2007年、タワー技術を用いた世界初の商用CSPプラントとして、PS10太陽光発電タワーを稼働させました。

- さらに2022年、スペインのエコロジー移行省は、同国におけるCSPプロジェクトの開発につながるオークション・メカニズムを通じて、CSP設置容量220MWを獲得しました。スペイン政府はまた、2025年までにCSP容量600MWの入札を実施すると発表しました。

- 従って、設置容量の増加に伴い、予測期間中は欧州がCSP市場を独占すると予想されます。

集光型太陽熱発電(CSP)産業の概要

集光型太陽熱発電(CSP)市場は適度に統合されています。この市場の主要企業(順不同)には、Aalborg CSP、Acciona SA、ACWA Power、Brightsource Energy Inc.、Engie SAなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測

- 2028年までのCSP設置容量と予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 集光型太陽熱発電技術のコスト低下

- 抑制要因

- 他の再生可能エネルギー源に対する政府の支援政策

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 技術分野

- パラボラトラフ

- リニアフレネル

- パワータワー

- ディッシュ/スターリング

- 熱媒体

- 溶融塩

- 水性

- 油性

- その他の熱媒体

- 地域

- 北米

- 米国

- メキシコ

- その他北米

- 欧州

- ドイツ

- イタリア

- フランス

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 韓国

- その他のアジア太平洋

- 南米

- ブラジル

- チリ

- その他の南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競争情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Nextera Energy Inc.

- Acciona SA

- ACWA Power

- Brightsource Energy Inc.

- Engie

- SR Energy

- Aalborg CSP

- Chiyoda Corporation

第7章 市場機会と今後の動向

- 技術の向上とハイブリッド発電所における集光型太陽光発電の統合

目次

Product Code: 49456

The Concentrated Solar Power Market size is estimated at 11.08 gigawatt in 2025, and is expected to reach 15.49 gigawatt by 2030, at a CAGR of 6.93% during the forecast period (2025-2030).

Key Highlights

- Over the long term, the declining cost of concentrated solar power technologies is expected to drive the market.

- On the other hand, the increasing adoption of solar photovoltaics and other renewable technologies is expected to hinder the market growth during the forecast period.

- Nevertheless, technology improvements and integration of concentrated solar power in hybrid power plants. This will positively impact the environment, and climate change is expected to create several opportunities for Concentrating the solar power market in the future.

- Europe is expected to dominate the market as the solar sector in the region is witnessing new projects at the outset of growing electricity demand and focusing on using renewable energy sources to curb pollution levels, therefore resulting in increasing demand for CSP during the forecast period.

Concentrated Solar Power (CSP) Market Trends

Parabolic Trough Segment to Dominate the Market

- Parabolic-trough collectors (PTCs) consist of long U-shaped mirrors with a linear axis tracking system. The mirrors reflect direct solar radiation along their focal line, where an absorber tube is located. The receiver/absorber tube is made of steel. It has a selective coating that maintains high absorbance in the solar spectrum wavelength range but high reflectance in the infrared spectrum (i.e., it emits as little as possible).

- The most commonly used fluid is thermal oil, although water/steam or molten salt are also used for this configuration. These are some of the most widely deployed configurations for CSPs.

- Parabolic trough collectors are one of the most commonly deployed CSPs around the globe; they can be deployed in domestic heating, desalination, refrigeration systems, industrial heat, power plants, pumping irrigation water, etc. According to the National Renewable Energy Laboratory (NREL), as of June 2022, Parabolic trough accounts for a share of 63.5% of total global CSP installed capacity.

- The Parabolic Trough Collector (PTC) 's operations and maintenance part is slightly complicated compared to its counterparts. The most frequent activities related to solar field operations and maintenance are the periodic measurement of mirror reflectivity and washing. Mirror reflectivity directly affects the amount of valuable thermal energy solar collectors deliver. It may also require tall vehicles or cranes to perform routine cleaning and maintenance.

- For instance, in 2020, researchers from the Indian Institute of Technology Madras created a low-cost Solar Parabolic Trough Collector (PTC) device for concentrating solar energy for industrial uses such as desalination, space heating, and space cooling. This system, created and developed in India, is lightweight and highly efficient under various climate and load circumstances.

- Hence, the parabolic trough is expected to dominate the market for concentrated solar power during the forecast period.

Europe to Dominate the Market

- In Europe, the power sector accounts for more than 75% of greenhouse gas emissions in the region. Increasing the share of renewable energy has become a potential option for the region to tackle climate change.

- The solar sector is witnessing new projects at the outset of growing electricity demand and focusing on using renewable energy sources to curb pollution levels across the region. In 2022, Europe had about 2.3 GW of installed CSP capacity. As per IRENA, by 2030, Europe will likely install 4 GW of concentrated solar power (CSP)

- In Europe, Energy cooperation such as MUSTEC or Market Uptake of Solar Thermal Electricity intends to focus on the collaborative development of CSP projects in the region, given the EU 2030 climate and energy framework. MUSTEC aims to deploy CSP projects in Southern Europe to meet the electricity demand of Central and North European countries.

- Likewise, the EU Solaris ERIC, the European Research Infrastructure for CSP/Solar thermal energy, aims to develop CSP research-related activities and applications. The development of tools and techniques, new capacities, solutions, everyday standards, and protocols to ramp up CSP technology in the region.

- Further, in 2022, the German government introduced a 55% subsidy to install CSP to speed up the clean energy transition to green heating for industrial applications. It also envisages lowering payback time to below three years for CSP technology. This would significantly help CSP installations to increase in Germany.

- Similarly, Spain was the first European country to initiate feed-in-tariff mechanisms for CSP in 2002, which helped ramp up CSP deployment. Moreover, in 2007, Spain commissioned the PS10 solar power tower as the first commercial CSP plant to use tower technology worldwide.

- Further, in 2022, the Ministry of Ecological Transition, Spain, awarded 220 MW capacity for CSP installation through an auction mechanism that would give rise to the development of CSP projects in the country. Spain's government also announced to float tenders for 600 MW of CSP capacity by 2025.

- Hence, with the increasing installed capacities, Europe is expected to dominate the CSP market during the forecast period.

Concentrated Solar Power (CSP) Industry Overview

The concentrated solar power (CSP) market is moderately consolidated. Some of the key players in this market (in no particular order) include Aalborg CSP, Acciona SA, ACWA Power, Brightsource Energy Inc., and Engie SA., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Installed CSP Capacity and Forecast in MW, till 2028

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Declining Cost of Concentrated Solar Power Technologies

- 4.6.2 Restraints

- 4.6.2.1 Supportive Government Policies for Other Renewable Energy Sources

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Parabolic Trough

- 5.1.2 Linear Fresnel

- 5.1.3 Power Tower

- 5.1.4 Dish/Stirling

- 5.2 Heat Transfer Fluid

- 5.2.1 Molten Salt

- 5.2.2 Water-based

- 5.2.3 Oil-based

- 5.2.4 Other Heat Transfer Fluids

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Mexico

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 Italy

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 South Korea

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Chile

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Nextera Energy Inc.

- 6.3.2 Acciona SA

- 6.3.3 ACWA Power

- 6.3.4 Brightsource Energy Inc.

- 6.3.5 Engie

- 6.3.6 SR Energy

- 6.3.7 Aalborg CSP

- 6.3.8 Chiyoda Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technology Improvements and Integration of Concentrated Solar Power in Hybrid Power Plants

集光型太陽熱発電(CSP)-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日