|

市場調査レポート

商品コード

1852144

グリース:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Grease - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| グリース:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年09月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

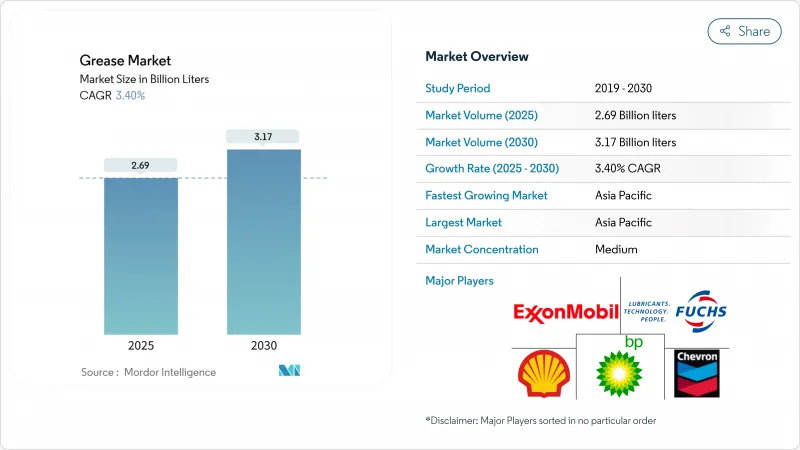

グリース市場規模は2025年に26億9,000万リットルと推計され、2030年には31億7,000万リットルに達すると予測され、予測期間中(2025~2030年)のCAGRは3.40%です。

増粘剤ミックスの変化はよりダイナミックで、カルシウムベースの製品がCAGR 9.10%で拡大し、リチウムの長年の支配力を削ぎ始めています。炭酸リチウムの価格変動、環境規制の強化、電気自動車(EV)の技術的ニーズは、同時にバイヤーの優先順位とサプライヤーのポートフォリオを再構築しています。アジア太平洋地域は、建設機械の活況と世界で最も急成長しているEV生産基盤に後押しされ、需要の支点としての役割を維持しています。高温・極圧グレードは、機械の設計がベアリング、ギヤ、シールを従来の使用範囲をはるかに超えて押し進めるにつれて、ますます注目を集めています。

世界のグリース市場の動向と洞察

EUと北米の加工ラインにおける衛生食品グレード潤滑油の普及

加工業者がFDA 21 CFR 178.3570およびISO 21469規格に適合するにつれ、NSF H1登録グリースへの需要が加速しています。施設はクロスコンタミネーションのリスクを排除するために「オールH1」プログラムに移行しており、合成基油はより高い温度耐性(500°Fまで連続使用可能)と長い再潤滑間隔を達成するために鉱物油に取って代わりつつあります。この動向は、2024年以降コンプライアンスチェックが厳しくなっている欧州のベーカリー、酪農場、飲料工場で最も顕著です。製品組成と工場衛生の両方を認証できるサプライヤーは、経常的な数量を確保する複数サイト契約を獲得しています。

EV用e-パワートレイン・ベアリング、APACでリチウムコンプレックス&カルシウムスルホネートグリースにシフト

中国、韓国、インドにおける急速なEV生産は、配合要件を再構築しています。かつて10,000 rpmで回転していたベアリングは、現在では20,000 rpmを超え、150 °Cを超える熱負荷がかかっています。実験室でのテストによると、カルシウムスルホネートグリースは600°F付近の降下点でも安定性を維持し、リチウムコンプレックスの代替品よりも20%高いマージンを示し、同時に低い電気インピーダンスを示しています。2024年に発表されたOEMの仕様書には、すでにいくつかの量販モデルのフロントとリアのe-アクスルベアリングのデフォルトとしてカルシウムスルホネートが記載されています。安全なスルホン酸カルシウムのサプライチェーンを持つグリースメーカーは、この機会を利用して複数年の数量契約を締結しています。

電池セクターの競合による炭酸リチウムのコスト変動

炭酸リチウムのスポット価格は2021年から2024年にかけて上昇しました。調査データによると、リチウム濃縮剤は2年間で世界生産量の70%から60%に減少し、生産者は現在、利幅を守るためにポリウレアまたはカルシウム技術でヘッジしています。グリース四半期ごとの価格リセットの影響を受けるバイヤーは、スポット不足を緩和するためにサプライヤーを多様化しています。一部の自動車メーカーは、リチウムのベンチマークに連動する契約途中の課徴金を回避するため、カルシウムスルホネートグリースを事前承認しています。

セグメント分析

リチウムベースの製品は2024年のグリース市場の66%を占めているが、カルシウムベースの量はCAGR 9.10%で増加しています。この再編成は、リチウム価格の高騰とカルシウム化学が提供する優れた高温耐性という2つの力学に根ざしています。メーカー各社は、リチウムとカルシウムのバッチ間で融通を利かせるためにリアクターラインを再調整しており、顧客が承認した製品コードを維持しながら原料リスクを軽減しています。アルミニウム・コンプレックス・グリースは、船舶用や製紙工場用の耐水性ニッチで重要性を維持しています。ポリウレアグレードは、金属石鹸を使用しないことで電気インピーダンスを低減し、騒音に敏感なEVベアリング用途で支持を集めています。エンドユーザーは、従来のリチウムグリースとの非互換性を理由に、ポリウレアの広範な採用には慎重な姿勢を崩していないが、OEM充填ユニットは数量増加への早道となります。

中国の風力タービンの主軸受の再潤滑間隔が30%延長されたことを示す現場証拠が、カルシウムスルホネートの受容をさらに後押ししています。リチウムコンプレックスのライバルと比較したベンチマークテストでは、油分離が少なく、ドロップポイント性能が優れていることが確認されました。これは、ナセル温度が-20℃以下でありながら、70℃を超える太陽光にさらされるピークで運転されるタービンにおいて重要な利点です。生産者は、カルシウムの自然な洗浄力が添加剤の処理速度を下げ、スルホン酸コストの上昇を部分的に相殺するコスト削減をもたらすことを強調しています。結局のところ、増粘剤の状況は、リチウム、カルシウム、アルミニウム、ポリウレアが、それぞれグリース市場内で明確な性能のニッチを守るマルチケミストリー・ポートフォリオに細分化されつつあります。

鉱物油グリースは2024年のグリース市場シェアの75%を占め、合成グレードはCAGR 4.90%で上昇すると予測されています。ポリアルファオレフィン(PAO)ベースは、酸化安定性と幅広い温度範囲により、合成プールを支配しています。Mobil AviationグリースSHC 100は、-54 °Cから177 °Cまで使用可能で、航空宇宙OEMが認める性能の優位性を示しています。バイオベース・オイルは、EAL指令や自主的なESGプログラムによる法規制の追い風を享受しています。酸化防止剤を配合した植物由来のエステルは、標準的なASTM試験において、酸化寿命でグループIIIの鉱物油に匹敵するようになりました。

鉱物油グリースは、シャーシの潤滑や工業用オープンギアドライブなど、価格に敏感な用途をNLGI推奨の慣行に沿ったものにしています。しかし、最新の高速生産ラインで要求される作動温度の変化により、購買者は中級の用途であっても合成油や半合成油を指定するようになってきています。PAOやエステルパッケージへの複雑な添加剤の溶解性を熟知しているサプライヤーは、グリース市場の特殊グレードと食品グレードの分野で平均を上回るマージンを獲得できる立場にあります。

地域分析

アジア太平洋地域は2024年に世界販売量の49%を占め、CAGR 4.32%と欧州の2倍のペースで拡大しています。中国の製造コンビナート、インドのインフラ急増、東南アジアのEV部品集積が高い稼働率を維持しています。シェルがタイのグリース工場の生産能力を年産1万5,000トンに3倍増することを決定したことは、この地域の牽引力を裏付けています。グリース市場規模における同地域のシェアは、2030年までに52%に達すると予想され、同地域の構造的リーダーシップは確固たるものとなります。

北米は、堅調な食品加工と活況を呈している再生可能エネルギーのパイプラインに支えられ、総量の大きなシェアを占めています。風力発電所の建設は、100mを超えるハブの高さで5年間のメンテナンスサイクルが可能な合成油への需要を高めています。環境的に許容される潤滑油への規制の重視は、五大湖や沿岸航路の船舶オペレーターに貨物ウィンチポイントをEAL認証グリースに変更するよう促しています。

欧州は販売量の大きなシェアを占めているが、最も厳しい規制課題に直面しています。PFAS規制は、自動車、航空宇宙、機械OEMのサプライヤー監査を引き起こしました。信頼性を犠牲にすることなくPFASフリーの代替品を示すサプライヤーは、シェアを維持する態勢を整えています。南米と中東・アフリカは、2024年の需要に占める割合が小さいです。自動潤滑システムの普及率が低いため、単位当たりの消費量は増加するが、資本制約により技術のアップグレードは遅れています。レトロフィット・ソリューションを提供するサービスプロバイダーは、グリース市場のこれらのフロンティアセグメントにおいて、量の不均衡を利用して成長を加速させることができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EUと北米の加工ラインにおける食品用衛生潤滑油の普及

- EV用e-パワートレイン軸受のリチウム複合グリースとカルシウムスルホネートグリースへの移行

- 深海掘削における耐水性グリースの活用

- インドとASEANの建設機械ブームが極圧グリースを牽引

- 発電セクターへの投資の堅調な伸び

- 市場抑制要因

- 電池セクターの競争による炭酸リチウムのコスト変動

- PFASと窒化ホウ素添加剤に対するEUのREACH規制強化

- アフリカと南米における自動潤滑システムの普及率の低さ

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測(金額および数量)

- 増粘剤別

- リチウムベース

- カルシウムベース

- アルミベース

- ポリウレア

- その他の増粘剤

- 製品タイプ別

- 鉱物油

- 合成油

- バイオベース・オイル

- 性能グレード別

- 高温グリース

- 低温および極地グレードグリース

- 極圧・高負荷グリース

- エンドユーザー業界別

- 自動車・その他輸送

- 発電(風力、水力、火力)

- 重機

- 食品・飲料

- 冶金・金属加工

- 化学製造

- その他の業界

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- エジプト

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Ampol Limited

- Axel Christiernsson AB

- BECHEM Lubrication Technology LLC

- BP p.l.c.

- Chevron Corporation

- China Petrochemical Corporation

- DuPont

- ENEOS Corporation

- ETS Oil & Gas Ltd.

- Exxon Mobil Corporation

- FUCHS

- Gazprom

- Gulf Oil International Ltd

- Idemitsu Kosan Co.,Ltd.

- Kluber Lubrication SE

- LUKOIL

- Morris Lubricants

- Orlen Oil

- Penrite Oi

- Petromin

- Petronas Lubricants International

- Saudi Arabian Oil Co.

- Shell Plc

- TotalEnergies