|

市場調査レポート

商品コード

1849873

ミリ波技術:市場シェア分析、産業動向、統計、成長予測(2025~2031年)Millimeter Wave Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ミリ波技術:市場シェア分析、産業動向、統計、成長予測(2025~2031年) |

|

出版日: 2025年06月19日

発行: Mordor Intelligence

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

概要

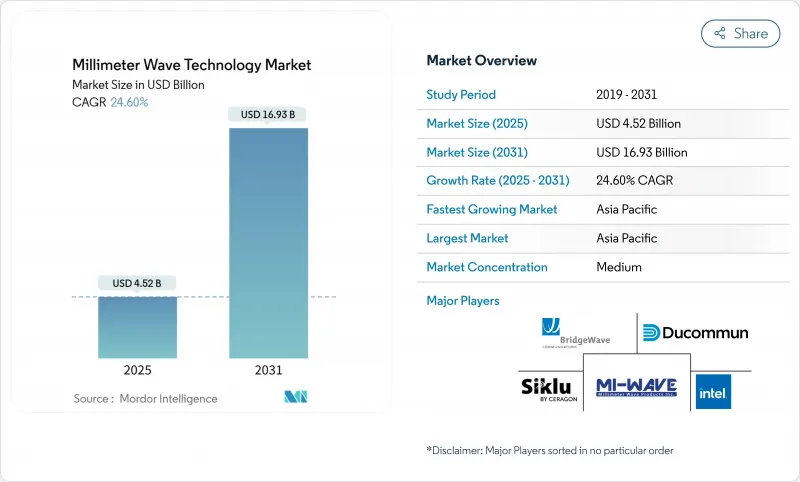

ミリ波技術市場規模は2025年に45億2,000万米ドル、2031年には169億3,000万米ドルに達すると推定・予測され、予測期間(2025-2031年)のCAGRは24.60%です。

ネットワーク事業者は容量緩和のために24GHz以上の周波数に目を向けており、防衛機関はより高解像度のターゲティングのためにレーダーシステムを94GHzにアップグレードしています。5Gの高密度展開と6Gの早期試験から生じる二重需要が設備投資を支える一方、デバイスコストの低下が医療画像、産業オートメーション、自動車ADASでの採用を後押ししています。アジア太平洋は、数百万サイトの5G展開により地域最大の地位を占めるが、北米は周波数自由化とCHIPS-Actに裏打ちされた半導体資金により技術革新を推進します。コンポーネントサプライヤは、特許で保護されたRFフロントエンドから恩恵を受けるが、窒化ガリウムウエハーへのサプライチェーン暴露は戦略的リスクをもたらします。

世界のミリ波技術市場動向と洞察

5Gネットワークの高密度化とスモールセルバックホール需要

通信事業者は、スモールセル密度が都市部のゾーニング上限を超えるとファイバーが不経済になることをすぐに発見します。中国、米国、インドでの実地試験では、数ギガビットのスループットが得られ、ミリ波バックホールが高コストの溝掘り作業の代わりになることが確認されました。機器ベンダーは現在、ソフトウェア定義のビームステアリングを統合してアライメント時間を短縮し、都市当局は屋上許可を合理化してサイトの活性化を加速させています。資本効率と市場投入までの時間短縮により、ワイヤレス・バックホールはミリ波技術市場の要となっています。

24-100 GHz帯におけるモバイルおよび固定無線データトラフィックの増加

固定ワイヤレスの加入者はモバイル加入者の最大5倍のデータを消費するため、通信事業者は連続した28GHzブロックを住宅用ゲートウェイに割り当てざるを得ないです。規制機関は、70/80/90 GHzの規則を調和させ、より広いチャンネルを可能にすることで対応し、チップセットメーカーはリンク最適化のためのAIを統合した第2世代CPEプラットフォームを発表しました。これらの進歩は地方のブロードバンド・プログラムをサポートし、ミリ波技術市場全体の需要を刺激します。

100 GHzを超えるRFフロントエンドの熱管理限界

周波数が高くなるにつれて熱集中が不均衡に上昇し、窒化ガリウム・デバイスを信頼性を低下させる接合温度へと押し上げます。ダイヤモンド基板やマイクロ流体冷却を使用した先進パッケージングが評価されていますが、これらのアプローチは材料コストを増加させ、認定サイクルを長引かせます。スケーラブルなサーマルソリューションが登場するまでは、短期的な導入は100GHz以下に集中し、ミリ波技術市場のアッパーバンド成長が抑制されます。

セグメント分析

2030年までのCAGRが最も速いのはイメージング・センサで、これはテラヘルツイメージングが腫瘍学や火傷評価においてラベルフリーの組織診断を可能にするためです。これとは対照的に、アンテナとトランシーバは、モバイル基地局用の無線フロントエンドを供給することで、2024年に38%の最大シェアを維持します。イメージング・センサーのミリ波技術市場規模は、病院が非電離診断ツールを採用することにより、2030年までに30億米ドルを超えると予想されます。通信・ネットワークICはマクロセルの高密度化によって補完的に成長し、インターフェイス・制御ICはレーダー・オン・チップ統合の動向に乗る。

NTTの300GHzでの280Gbps信号生成のような研究開発のブレークスルーは、リンクバジェットを改善し、周波数アジャイルシンセサイザーの需要を刺激します。一方、インテグレーターがより高い電力密度を求めるにつれて、先端基板やサーマルインターフェイス材料を中心とするその他コンポーネントの存在感が増しています。その結果、ミリ波技術市場を支えるコンポーネント・スタックが拡大しています。

完全または部分的にライセンシングされた周波数帯は、2024年の売上高の78%を占め、これは電気通信のマクロセルや防衛ネットワークにおける干渉のない運用にプレミアムがついていることを反映しています。しかし、規制当局が最小限の事務処理で済む産業用プレゼンス・センシング・ルールを策定したため、95GHz以上の免許不要の割り当てがCAGR 26.43%で増加しました。中小企業は、この簡素化された制度を利用して、ロボット工学や品質検査用の工場床レーダーを導入し、ミリ波技術市場に新たな収益源を加えています。

ベンダーは現在、規制環境を自動検出してEIRP設定をリアルタイムで調整するデュアルモード・チップセットを導入しており、主要な採用障壁を取り除いています。ライセンス・スペクトラムはミッション・クリティカルなリンクに不可欠であることに変わりはないが、アンライセンス・スペクトラムの急増により、アドレス可能なベース全体が広がっています。

ミリ波技術市場レポートは、コンポーネント(アンテナおよびトランシーバ、通信およびネットワーキングIC、インタフェースおよび制御IC、周波数生成およびフィルタなど)、ライセンスモデル(フル/パートライセンスおよびアンライセンス)、周波数帯(24-57GHz、57-95GHz、95-300GHz)、アプリケーション(通信インフラ、モバイルおよびコンシューマ機器、固定無線アクセスなど)、地域別に分類されています。

地域分析

アジア太平洋地域は2024年の収益の42%を占め、2030年まで28.02%のCAGRで成長すると予測されます。これは中国の440万台の5G基地局とインドの急速なFWA普及が後押ししています。地方政府は5G-Advanced研究に公的資金を割り当て、委託製造業者は窒化ガリウムウエハーラインに投資して供給を現地化します。日本の民間5Gモデルでは、用地取得の複雑さからmmWaveの普及が遅れているが、企業のキャンパスではARトレーニング用に60GHzの屋内ネットワークが試験的に導入されています。

北米では周波数政策が産業革新と整合し、37GHz帯と70/80/90GHz帯が解放される一方、CHIPS-Actのインセンティブが国内工場に向けられます。国防レーダーのアップグレードや固定ワイヤレスの配備が回復力のある顧客基盤を支え、Nokia-T-Mobileのようなパートナーシップが複数年の機器パイプラインを確保します。カナダは地方でのブロードバンド試験運用にミリ波を採用し、ミリ波技術市場をさらに拡大します。

欧州は自らを技術研究所として位置づけています。ドイツは6Gテストベッドとマイクロエレクトロニクスクラスターを支援し、規制当局は製造イノベーションを優先する42GHzオークション条件を策定します。ドイツのOEMメーカーによる自動車用レーダーの需要は、専門チップメーカーとの協力関係を促進し、英国は60GHzの輸送インフラリンクを模索しています。中東はスマートシティの実証実験に投資し、南アフリカは28GHz FWAを試験的に導入し、ブラジルはmmWave CPEの組み立てに的を絞った税制優遇措置を導入しています。これらの新興市場からの収益貢献は1桁台にとどまるもの、成長率は成熟地域を上回り、市場力学にダイナミズムを与えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 5Gネットワークの高密度化とスモールセルバックホールの需要

- 24~100GHz帯におけるモバイルおよび固定無線データトラフィックの増加

- 40GHz以上の周波数帯の自由化と新たなオークション

- 低遅延ターゲティングのため防衛レーダーを94GHzにアップグレード

- 最後の50メートルの光ファイバー代替のための屋内ミリ波FWA

- 122 GHz産業用プレゼンスセンシング規制の出現

- 市場抑制要因

- 100 GHzを超えるRFフロントエンドの熱管理限界

- 大量生産における高コストのフェーズドアレイ校正

- 密集地における自治体の「街路家具」ゾーニングの障害

- 窒化ガリウムウエハーサプライチェーンの集中リスク

- バリューチェーン/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ミリ波アプリケーションにおけるGaNの重要性

- mmWave基板の情勢:LCP、PI、PTFEが5G HWに与える影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- COVID-19の影響評価

第5章 市場規模と成長予測

- コンポーネント別

- アンテナとトランシーバー

- 通信およびネットワークIC

- インターフェースおよび制御IC

- 周波数生成とフィルタ

- イメージングセンサー

- その他のコンポーネント

- ライセンシングモデル別

- 完全/部分ライセンス

- 無免許

- 周波数帯域別

- 24~57GHz

- 57~95GHz

- 95~300GHz

- 用途別

- 通信インフラストラクチャ(RANおよびバックホール)

- モバイルおよびコンシューマーデバイス

- 固定無線アクセス(FWA)

- レーダーとセキュリティ画像

- 自動車向けADASとV2X

- 産業オートメーションとIIoT

- 医療およびライフサイエンスイメージング

- 航空宇宙および防衛通信

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- ナイジェリア

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Anokiwave Inc.

- Aviat Networks

- Broadcom Inc.

- BridgeWave Communications(REMEC)

- Ducommun Incorporated

- Eravant(SAGE Millimeter)

- Farran Technology

- Huawei Technologies

- Intel Corporation

- Keysight Technologies

- L3Harris Technologies

- Millimeter Wave Products Inc.

- NEC Corporation

- Nokia Corporation

- NXP Semiconductors

- Qualcomm Technologies

- Samsung Electronics

- Sivers Semiconductors

- Siklu Communication(Ceragon)

- Smiths Interconnect

- Vubiq Networks