|

市場調査レポート

商品コード

1684693

通信ミリ波技術市場の機会、成長促進要因、産業動向分析、2025~2034年予測Telecom Millimeter Wave Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 通信ミリ波技術市場の機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年01月16日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

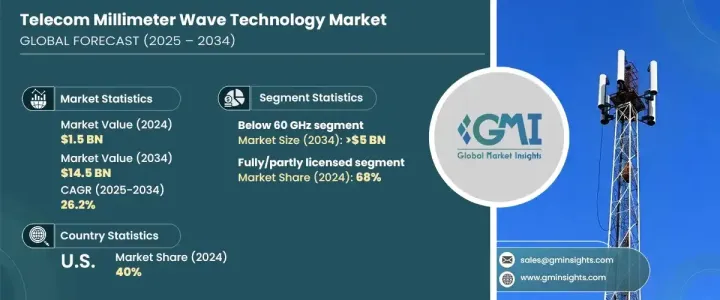

世界の通信ミリ波技術市場は、2024年に15億米ドルに達し、2025年から2034年にかけて26.2%という驚異的なCAGRで成長しようとしています。

世界各国政府は、次世代通信ネットワークの整備に向けた取り組みを加速しており、高速接続に対する需要の高まりに対応するためにデジタルインフラを強化しています。ミリ波技術に大きく依存する5Gの急速な導入は、官民のパートナーシップによって通信への戦略的投資が推進される中、勢いを増し続けています。これらの大規模なイニシアチブは、堅牢な接続性を確保し、待ち時間を短縮し、ネットワーク全体のパフォーマンスを向上させることを目的としています。

ミリ波技術は、ブロードバンドの拡大、スマートシティの開発、産業オートメーションに革命をもたらし、世界通信の将来におけるその役割を確固たるものにしています。セキュアで高速な接続は、産業、政府機関、消費者向けアプリケーションにおいて絶対的な必要条件となりつつあり、ミリ波対応ソリューションへの需要を押し上げています。通信事業者は、ネットワークの混雑を緩和しながら接続性を高めるイノベーションを優先しています。研究開発の進展に伴い、信号トランスミッション、スペクトラム効率、ハードウェアの小型化における新たな進歩により、ミリ波通信の能力が大幅に強化されることが期待されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 15億米ドル |

| 予測金額 | 145億米ドル |

| CAGR | 26.2% |

IoT、AI主導のアプリケーション、クラウドベースのソリューションの採用が急増するなか、企業は超高速で安定した接続を確保するため、ミリ波技術を積極的にネットワークに組み込んでいます。この技術は、自律型輸送、遠隔医療、防衛通信などのミッションクリティカルなアプリケーションを急速に変革し、比類のないデータ転送速度と信頼性を提供しています。この変革は、ミリ波対応システムの広範な展開をサポートするために、インフラの継続的なアップグレードと規制の適応の必要性を強調しています。

周波数帯による市場セグメンテーションには、60GHz未満、60~100GHz、100GHz以上があります。60GHz未満セグメントは2024年の市場シェアの40%を占め、2034年には50億米ドルを超えると予想されています。この周波数帯域は、高価な周波数帯域に比べ、価格が手ごろでアクセスしやすいことから広く支持されています。ネットワーク事業者にとっては、この周波数帯の周波数ライセンスを確保するのが容易であるため、展開の費用対効果が高くなります。規制上の課題が軽減され、運用コストが下がることも、通信事業者がこれらの周波数帯をネットワークに統合することを後押ししています。

同市場はまた、免許モデル別にも分類されており、完全免許/一部免許の周波数帯と免許なしの周波数帯があります。2024年のシェアは、フルライセンス/パートライセンスセグメントが68%を占めています。ライセンシングされた周波数帯は、ネットワーク事業者に独占的な権利を提供し、干渉のない運用とネットワーク容量の拡大を保証します。このような独占的権利は、セキュリティと安定性を高め、事業者が中断のない高速サービスを提供することを可能にします。パフォーマンスを最適化し、信号の乱れを最小限に抑えることを目指すモバイル・サービス・プロバイダーにとって、専用周波数帯域を確保する能力は極めて重要です。拡張現実(AR)、仮想現実(VR)、リアルタイム・データ・ストリーミングなど、広帯域アプリケーションのニーズが高まる中、免許取得済み周波数帯に対する需要はさらに高まると思われます。

米国の通信ミリ波技術市場は、固定無線アクセス(FWA)ソリューションの広範な採用が原動力となり、2024年には40%の圧倒的シェアを占めています。これらのソリューションは、従来のブロードバンドに代わる有力な選択肢として急速に普及しており、通信会社はコストのかかるファイバー敷設を必要とせずに接続性を拡大できます。ミリ波周波数は、最小限のアクセス制限でシームレスな無線カバレッジを提供するため、都市部や郊外でのブロードバンド拡大に理想的な選択肢となります。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 一次情報

- データマイニングソース

- 市場範囲と定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- コンポーネントプロバイダー

- サービスプロバイダー

- 技術プロバイダー

- 最終顧客

- サプライヤーの状況

- 利益率分析

- 技術革新の状況

- 特許分析

- 主要ニュース&イニシアチブ

- 規制状況

- 親子市場分析

- 影響要因

- 促進要因

- データ・トラフィックと接続ニーズの増加

- デジタルインフラへの政府投資

- スマートシティとIoTアプリケーションの増加

- 5Gネットワークの急速な展開

- 業界の潜在的リスク&課題

- 既存の通信インフラとの複雑な統合

- 高いインフラコスト

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- アンテナ&トランシーバー

- 通信機器

- 処理装置

- 周波数ソース

- その他

第6章 市場推計・予測:周波数別、2021年~2034年

- 主要動向

- 60GHz未満

- 60-100 GHz

- 100GHz以上

第7章 市場推計・予測:免許モデル別、2021年~2034年

- 主要動向

- フル/パートライセンシング

- 非ライセンス

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 電気通信事業者

- 政府・防衛

- 企業

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Analog Devices

- Anokiwave

- AT&T

- Broadcom

- Ciena

- Ericsson

- Huawei

- Keysight

- L3Harris

- MediaTek

- Millimeter Wave Products

- NEC

- Nokia

- Qorvo

- Qualcomm

- Samsung

- Siklu Communication

- Skyworks

- Verizon

- ZTE

The Global Telecom Millimeter Wave Technology Market reached USD 1.5 billion in 2024 and is on track to grow at an impressive CAGR of 26.2% between 2025 and 2034. Governments worldwide are accelerating efforts to roll out next-generation communication networks, enhancing digital infrastructure to support the growing demand for high-speed connectivity. The rapid adoption of 5G, which relies heavily on millimeter wave technology, continues to gain momentum as public and private sector partnerships drive strategic investments in telecommunications. These large-scale initiatives aim to ensure robust connectivity, reduce latency, and improve overall network performance.

Millimeter wave technology is revolutionizing broadband expansion, smart city development, and industrial automation, cementing its role in the future of global communications. Secure, high-speed connections are becoming an absolute necessity across industries, government institutions, and consumer applications, pushing demand for millimeter wave-enabled solutions. Telecom operators are prioritizing innovations that enhance connectivity while alleviating network congestion. As research and development efforts progress, new advancements in signal transmission, spectrum efficiency, and hardware miniaturization are expected to significantly enhance the capabilities of millimeter wave communication.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $14.5 Billion |

| CAGR | 26.2% |

With the surging adoption of IoT, AI-driven applications, and cloud-based solutions, enterprises are actively integrating millimeter wave technology into their networks to ensure ultra-fast and stable connections. The technology is rapidly transforming mission-critical applications, including autonomous transportation, telemedicine, and defense communications, offering unparalleled data transfer speeds and reliability. This transformation underscores the need for continued infrastructure upgrades and regulatory adaptations to support the widespread deployment of millimeter wave-enabled systems.

Market segmentation by frequency band includes below 60 GHz, 60-100 GHz, and above 100 GHz. The below 60 GHz segment accounted for 40% of the market share in 2024 and is expected to exceed USD 5 billion by 2034. This frequency band is widely favored for its affordability and broader accessibility compared to higher bands. Network operators find it more convenient to secure spectrum licenses for these frequencies, making deployment more cost-effective. Reduced regulatory challenges and lower operational costs further encourage telecom companies to integrate these bands into their networks.

The market is also categorized by licensing models, including fully/partly licensed and unlicensed spectrum. The fully/partly licensed segment dominated with a 68% share in 2024. Licensed spectrum offers network operators exclusive rights, ensuring interference-free operations and greater network capacity. These exclusive rights provide enhanced security and stability, allowing operators to deliver uninterrupted, high-speed services. The ability to secure dedicated frequency bands is crucial for mobile service providers aiming to optimize performance and minimize signal disruptions. With the increasing need for high-bandwidth applications such as augmented reality, virtual reality, and real-time data streaming, the demand for licensed spectrum is set to strengthen further.

The US telecom millimeter wave technology market held a commanding 40% share in 2024, driven by the widespread adoption of Fixed Wireless Access (FWA) solutions. These solutions are rapidly gaining traction as a viable alternative to traditional broadband, enabling telecom companies to expand connectivity without the need for costly fiber installations. Millimeter wave frequencies provide seamless wireless coverage with minimal access restrictions, making them an ideal choice for broadband expansion in urban and suburban areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Component providers

- 3.1.2 Service providers

- 3.1.3 Technology providers

- 3.1.4 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Parent and child market analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing data traffic and connectivity needs

- 3.9.1.2 Government investments in digital infrastructure

- 3.9.1.3 Rise in smart city and IoT applications

- 3.9.1.4 Rapid 5G network deployment

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Complex integration with existing telecom infrastructure

- 3.9.2.2 High infrastructure costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Antennas & transceivers

- 5.3 Communication equipment

- 5.4 Processing units

- 5.5 Frequency sources

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Frequency, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Below 60 GHz

- 6.3 60-100 GHz

- 6.4 Above 100 GHz

Chapter 7 Market Estimates & Forecast, By Licensing Model, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Fully/partly licensed

- 7.3 Unlicensed

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Telecom providers

- 8.3 Government and defense

- 8.4 Enterprises

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Russia

- 9.2.7 Nordics

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 South Korea

- 9.3.6 Southeast Asia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 UAE

- 9.5.2 South Africa

- 9.5.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Analog Devices

- 10.2 Anokiwave

- 10.3 AT&T

- 10.4 Broadcom

- 10.5 Ciena

- 10.6 Ericsson

- 10.7 Huawei

- 10.8 Keysight

- 10.9 L3Harris

- 10.10 MediaTek

- 10.11 Millimeter Wave Products

- 10.12 NEC

- 10.13 Nokia

- 10.14 Qorvo

- 10.15 Qualcomm

- 10.16 Samsung

- 10.17 Siklu Communication

- 10.18 Skyworks

- 10.19 Verizon

- 10.20 ZTE