|

市場調査レポート

商品コード

1685812

ベリリウム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Beryllium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ベリリウム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

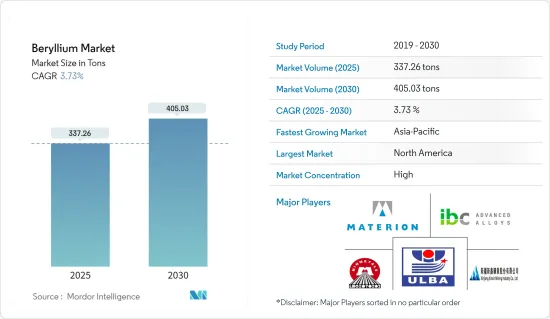

ベリリウム市場規模は2025年に337.26トンと推定され、予測期間(2025-2030年)のCAGRは3.73%で、2030年には405.03トンに達すると予測されています。

ベリリウム市場はCOVID-19による挫折に直面しました。世界の操業停止と厳しい政府規制により、生産拠点は広範囲にわたって操業停止に追い込まれました。しかし、市場は2021年に回復し、今後数年間は大幅な成長が見込まれます。

主なハイライト

- 短期的には、エレクトロニクスと通信インフラの需要拡大と、航空宇宙と軍事用途でのベリリウム合金の広範な使用が市場の需要を牽引します。

- しかし、潜在的な代替品との競合が市場成長の妨げになると予想されます。

- とはいえ、原子力発電における酸化ベリリウムの将来的な需要や、ベリリウムミラーの新たな用途は、調査対象の市場に新たな機会を生み出すと予想されます。

- 北米が世界市場を独占すると予想され、需要の大部分は米国とカナダからもたらされます。

ベリリウム市場の動向

エレクトロニクスと通信セグメントが市場を独占する

- ベリリウムの主要なエンドユーザー産業として、家電と通信が際立っています。ベリリウムは主に銅と合金化され、銅-ベリリウム合金を形成します。これらの合金は、ケーブル、高精細テレビ、電気接点、携帯電話やコンピューターのコネクター、コンピューター・チップのヒートシンク、水中光ファイバー・ケーブル、ソケット、サーモスタット、ベローズなど、さまざまな製品に使われています。

- ベリリウムの優れた熱伝導性は放熱性を高め、過熱のリスクを軽減し、電子部品の信頼性を強化します。

- センサー、アンテナ、コンデンサー、抵抗器などの電子部品が小型化・高性能化するにつれて、この進化する状況におけるベリリウムの重要性はさらに顕著になっています。

- エレクトロニクス産業は、世界最大かつ最も急速に成長している産業のひとつです。現在のデジタル時代において、電子機器は人々の生活に大きな影響を及ぼしています。電子ガジェットの需要は継続的に増加し、世界的に重要な経済牽引役であり続けると予測されています。

- 電子情報技術産業協会(JEITA)のデータによると、2023年の世界の電子機器・IT産業は前年比3%減の3兆3,826億米ドルとなりました。しかし、2024年には9%成長し、3兆6,868億米ドルに達すると予測されており、回復が見込まれています。

- インドは中国に次ぐスマートフォン生産国です。Invest Indiaによると、同国は2025-26年までに1,260億米ドル相当の携帯電話を製造することを目指しています。世界的に、スマートフォンの需要は著しく増加しています。Telefonaktiebolaget LM Ericssonによると、スマートフォンの契約数は2027年までに76億9,000万台に達する見込みで、エレクトロニクス・アプリケーションから調査された市場の利用が拡大しています。

- 米国では、迅速な技術進歩と活発な研究開発活動が最先端のエレクトロニクス製品への需要を促進しています。同産業は継続的かつ著しい発展を遂げています。Consumer Technology Associationの報告によると、米国の家電製品販売による小売収入は2023年に4,850億米ドルに達し、2024年の予測は5,120億米ドルです。

- ドイツは欧州最大のエレクトロニクス産業を誇る。ドイツ電気電子工業会(ZVEI)のデータによると、2023年の同セクターの総売上高は2,381億ユーロ(約2,580億6,000万米ドル)に達しました。世界の家庭用電化製品市場の主な促進要因には、技術の進歩、急速な都市化、活況を呈する住宅部門、1人当たり所得の増加、生活水準の向上、家事における快適さの重視の高まり、消費者のライフスタイルの進化、小規模世帯の増加などがあります。

- こうした動きから、電子機器と通信の需要は増加し、ベリリウムの需要も増加するとみられます。

市場を独占する北米

- 北米はベリリウム市場をリードし、予測期間中に最も急成長する地域となります。この急成長は主に、自動車、ヘルスケア、航空宇宙・防衛、石油・ガス、エレクトロニクス・通信など、さまざまなセクター、特に米国とカナダにおける需要の増加が背景にあります。

- 米国地質調査所によると、米国は世界最大のベリリウム鉱山生産国で、2023年の生産量は190トンに達し、2022年の175トンから増加しました。

- ベリリウム資源の約60%は米国にあり、主にユタ州のスポールマウンテン地域に存在し、そこには大規模なベルトランダイト源を含むエピサーメンタル鉱床があります。ユタ州におけるベルトランダイトの確認埋蔵量および推定埋蔵量は、含有ベリリウム量で約2万トンと推定されています。

- ベリリウムは、熱伝導性、強度、耐食性に優れ、ブレーキディスク、イグニッションスイッチ、エアバッグセンサー、パワートレイン部品、電気部品など、さまざまな用途に理想的な材料であるため、自動車産業で使用されています。この地域で自動車生産台数が増加するにつれて、ベリリウムの需要も増加すると予想されます。

- 米国は、中国に次ぐ世界第2位の自動車産業を誇り、地域および世界市場において極めて重要な役割を果たしています。OICA(Organisation Internationale des Constructeurs Automobiles)のデータによると、米国の自動車生産台数は2023年に1,061万1,555台に達し、2022年から5.56%増加し、ベリリウムの需要を強化します。

- カナダ自動車工業会の報告によると、自動車部門はカナダのGDPに190億米ドル以上貢献しています。予測によると、この貢献は2024年には401億米ドルに増加し、ベリリウム市場に成長機会をもたらします。OICAのデータによると、カナダの2023年の自動車生産台数は155万3,026台で、前年比25.92%増です。

- ベリリウムの高い熱伝導性と卓越した強度対重量比は、航空宇宙と防衛において極めて重要です。高速航空機、ミサイル、ロケットエンジンのノズルに採用されています。同地域では航空宇宙・防衛セクターが拡大しており、ベリリウムの需要は増加するとみられます。

- 米国は北米最大の航空市場を有し、世界有数の保有機数を誇る。フランス、中国、ドイツといった国々への航空宇宙部品の輸出が好調で、この産業の製造活動を後押しし、ベリリウム市場にプラスの影響を与えています。

- 連邦航空局(FAA)によると、航空旅行と貨物需要の急回復に後押しされ、民間航空機の機体数は2022-23年に0.2%増加しました。さらに、米国の航空会社の搭乗者数は、今後20年間で年率2.4%成長し、2023年の9,220億米ドルに対し、2044年には1兆3,200億米ドルに達すると推定され、米国の主力ジェット機保有数は2023年の4,832機から2044年には6,894機に増加すると予測しています。

- エレクトロニクス分野では、ベリリウムの高い熱伝導性と非磁性は、電気接点、半導体、通信に不可欠です。同地域でエレクトロニクス・セクターが成長するにつれて、ベリリウムの需要も今後数年間は伸びると予想されます。

- 米国のエレクトロニクス部門は、先端技術製品に対する需要の急増と、活発な研究開発活動によって拍車がかかった急速な技術革新によって、緩やかな成長軌道に乗っています。

- エネルギー省(DOE)は2024年4月、バイデン大統領の超党派インフラ法に基づき、組合員の労働力を優先して新しい送電線に最大3億3,100万米ドルを投資する計画を発表しました。さらに同政権は、今後5年間で10万マイルの送電線を改良することを目標に、官民のリーダーたちと協力して全米の送電網を強化するイニシアチブを主導しています。

- 高い強度と導電性を持つベリリウムは、ダウンホール・チュービングからコンプレッサーや発電機に至るまで、石油・ガス分野での用途を見出しています。この地域の石油・ガスセクターの拡大に伴い、ベリリウムの需要は今後数年で増加するとみられます。

- カナダ統計局によると、2023年のカナダの原油生産量は3年連続で増加し、前年比1.4%増の2億8,640万立方メートルを記録しました。さらに、カナダ・エネルギー請負業者協会の予測によると、2024年に掘削される油井は6,229本で、2023年から481本増加すると予想されており、オイルサンド生産者が拡大局面にあることは明らかです。

- こうした動きを考えると、北米は予測期間中にベリリウム需要が急増する構えです。

ベリリウム産業のセグメンテーション

ベリリウム市場は高度に統合されています。主なプレーヤーは、Materion Corporation、Ulba Metallurgical Plant(Kazatomprom)、Hunan Shuikoushan Nonferrous Metals Group、IBC Advanced Alloys、Xinjiang Xinxin Mining Industryなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- エレクトロニクスおよび通信インフラからの需要拡大

- 優れた特性による医療機器での使用増加

- その他の促進要因

- 抑制要因

- 代替品との競合

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ

- 合金

- 金属

- セラミックス

- その他の製品タイプ

- エンドユーザー産業

- 産業用コンポーネント

- 自動車

- ヘルスケア

- 航空宇宙・防衛

- 石油・ガス

- エレクトロニクスと通信

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- American Beryllia Inc.

- American Elements

- Belmont Metals

- Hunan Shuikoushan Nonferrous Metals Group Co. Ltd

- IBC Advanced Alloys

- Materion Corporation

- NGK Metals

- Texas Mineral Resources Corp.

- Tropag Oscar H. Ritter Nachf GmbH

- Ulba Metallurgical Plant(kazatomprom)

- Xiamen Beryllium Copper Technologies Co. Ltd

- Xinjiang Xinxin Mining Industry Co. Ltd

第7章 市場機会と今後の動向

- 原子力発電における酸化ベリリウムの将来需要

- ベリリウムミラーの新たな用途

- その他の機会

The Beryllium Market size is estimated at 337.26 tons in 2025, and is expected to reach 405.03 tons by 2030, at a CAGR of 3.73% during the forecast period (2025-2030).

The beryllium market faced setbacks due to COVID-19. Global lockdowns and stringent government regulations led to widespread shutdowns of production hubs. However, the market rebounded in 2021, and it is estimated to witness significant growth in the upcoming years.

Key Highlights

- Over the short term, the growing demand from electronics and telecommunication infrastructure and extensive usage of beryllium alloys in aerospace and military applications drive the market's demand.

- However, competition from potential alternatives is expected to hinder the market's growth.

- Nevertheless, future demand for beryllium oxide in nuclear power generation and emerging applications of beryllium mirrors are expected to create new opportunities for the market studied.

- North America is expected to dominate the global market, with the majority of demand coming from the United States and Canada.

Beryllium Market Trends

Electronics and Telecommunications Segment to Dominate the Market

- Consumer electronics and telecommunications stand out as key end-user industries for beryllium. Beryllium is predominantly alloyed with copper in these applications, forming copper-beryllium alloys. These alloys find their way into various products, including cables, high-definition televisions, electrical contacts, cell phone and computer connectors, computer chip heat sinks, underwater fiber optic cables, sockets, thermostats, and bellows.

- Beryllium's excellent thermal conductivity enhances heat dissipation, mitigating overheating risks and bolstering the reliability of electronic components.

- As electronic components like sensors, antennas, capacitors, and resistors shrink and gain capabilities, beryllium's significance in this evolving landscape becomes even more pronounced.

- The electronics industry is one of the world's largest and fastest growing. In the current digital era, electronic items significantly impact people's lives. The demand for electronic gadgets is projected to rise continuously and remain a significant economic driver globally.

- As per data from the Japan Electronics and Information Technology Industries Association (JEITA), the global electronics and IT industry saw a 3% year-over-year decline in 2023, totaling USD 3,382.6 billion. However, a rebound is anticipated, with projections of a 9% growth in 2024, reaching USD 3,686.8 billion.

- India is the second largest smartphone producer after China. As per Invest India, the country aims to manufacture cell phones worth USD 126 billion by 2025-26. Globally, the demand for smartphones is increasing at a significant rate. According to the Telefonaktiebolaget LM Ericsson, the subscription is likely to reach 7,690 million by 2027, enhancing the usage of the market studied from electronics applications.

- In the United States, swift technological advancements and robust R&D activities fuel a demand for cutting-edge electronic products. The industry is witnessing continuous and significant progress. The Consumer Technology Association reports that retail revenue from US consumer electronics sales reached an impressive USD 485 billion in 2023, with projections for 2024 set at USD 512 billion.

- Germany boasts the largest electronics industry in Europe. Data from the Germany Electrical and Electronics Association (ZVEI) indicates that the sector achieved an aggregated turnover of EUR 238.1 billion (approximately USD 258.06 billion) in 2023. Key drivers for the global household appliances market include technological advancements, rapid urbanization, a booming housing sector, rising per capita income, enhanced living standards, a growing emphasis on comfort in household chores, evolving consumer lifestyles, and an increasing number of smaller households.

- Given these dynamics, the demand for electronics and telecommunications is set to rise, subsequently fueling the demand for beryllium.

North America to Dominate the Market

- North America is poised to lead the beryllium market, emerging as the region with the fastest growth during the forecast period. This surge is primarily fueled by increasing demands across various sectors, including automotive, healthcare, aerospace and defense, oil and gas, and electronics and telecommunications, particularly in the United States and Canada.

- As per the US Geological Survey, the United States was the world's largest beryllium mine producer, with production amounting to 190 metric tons in 2023, growing from 175 tons in 2022.

- About 60% of beryllium resources are in the United States, mainly in the Spor Mountain area in Utah, where the epithermal deposit contains a large bertrandite source. Proven and probable bertrandite reserves in Utah are estimated at about 20,000 tons of contained beryllium.

- Beryllium is used in the automotive industry due to its high thermal conductivity, strength, and resistance to corrosion, making it an ideal material for various applications, including brake discs, ignition switches, airbag sensors, powertrain components, and electrical components. As vehicle production rises in the region, the demand for beryllium is expected to bolster.

- The United States boasts the world's second-largest automotive industry, trailing only China, and plays a pivotal role in regional and global markets. Data from the Organisation Internationale des Constructeurs Automobiles (OICA) indicates that the US automotive production reached 10,611,555 units in 2023, marking a 5.56% increase from 2022, bolstering the demand for beryllium.

- As reported by the Automotive Industries Association of Canada, the automotive sector contributes over USD 19 billion to Canada's GDP. Projections suggest this contribution will rise to USD 40.1 billion in 2024, presenting growth opportunities for the beryllium market. OICA data shows Canada produced 1,553,026 vehicles in 2023, a 25.92% increase from the prior year.

- Beryllium's high thermal conductivity and exceptional strength-to-weight ratio render it crucial in aerospace and defense. It is employed in high-speed aircraft, missiles, and rocket engine nozzles. With the aerospace and defense sector expanding in the region, the demand for beryllium is set to rise.

- The United States has the largest aviation market in North America and boasts one of the world's most extensive fleet sizes. Strong exports of aerospace components to nations like France, China, and Germany are propelling the industry's manufacturing activities, positively influencing the beryllium market.

- According to the Federal Aviation Administration (FAA), boosted by the sharp recovery in demand for air travel and cargo, the number of aircraft in the commercial fleet grew by 0.2% in 2022-23. Additionally, US airline enplanements are estimated to grow 2.4% per year over the next 20 years to USD 1.32 trillion in 2044 compared to USD 922 billion in 2023, and projects the US mainline jet fleet to grow from 4,832 in 2023 to 6,894 in 2044.

- In electronics, beryllium's high thermal conductivity and non-magnetic properties are essential for electrical contacts, semiconductors, and telecommunications. As the electronics sector grows in the region, the demand for beryllium is expected to grow in the coming years.

- The US electronics sector is on a moderate growth trajectory, driven by a surge in demand for advanced technological products and rapid innovation spurred by robust R&D activities.

- The Department of Energy (DOE), in April 2024, announced plans to invest up to USD 331 million in a new transmission line, prioritizing union labor, under President Biden's Bipartisan Infrastructure Law. Additionally, the administration is leading an initiative by collaborating with public and private sector leaders to enhance the nation's transmission network, aiming to upgrade 100,000 miles of transmission lines in the next five years.

- With its high strength and conductivity, beryllium finds applications in the oil and gas sector, from down-hole tubing to compressors and generators. With the expanding oil and gas sector in the region, the demand for beryllium is set to rise in the coming years.

- Statistique Canada reports that Canada's crude oil production rose for the third consecutive year in 2023, hitting 286.4 million cubic meters, a 1.4% increase from the previous year. Moreover, with projections from the Canadian Association of Energy Contractors anticipating 6,229 wells to be drilled in 2024, up 481 from 2023, it is evident that oil sand producers are in an expansion phase.

- Given these dynamics, North America is poised for a surge in beryllium demand during the forecast period.

Beryllium Industry Segmentation

The beryllium market is highly consolidated. The major players include Materion Corporation, Ulba Metallurgical Plant (Kazatomprom), Hunan Shuikoushan Nonferrous Metals Group Co. Ltd, IBC Advanced Alloys, and Xinjiang Xinxin Mining Industry Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Electronics and Telecommunication Infrastructure

- 4.1.2 Increasing Usage in Medical Equipment Owing to its Superior Properties

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Competition from Potential Alternatives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Alloys

- 5.1.2 Metals

- 5.1.3 Ceramics

- 5.1.4 Other Product Types

- 5.2 End-user Industry

- 5.2.1 Industrial Components

- 5.2.2 Automotive

- 5.2.3 Healthcare

- 5.2.4 Aerospace and Defense

- 5.2.5 Oil and Gas

- 5.2.6 Electronics and Telecommunication

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 American Beryllia Inc.

- 6.4.2 American Elements

- 6.4.3 Belmont Metals

- 6.4.4 Hunan Shuikoushan Nonferrous Metals Group Co. Ltd

- 6.4.5 IBC Advanced Alloys

- 6.4.6 Materion Corporation

- 6.4.7 NGK Metals

- 6.4.8 Texas Mineral Resources Corp.

- 6.4.9 Tropag Oscar H. Ritter Nachf GmbH

- 6.4.10 Ulba Metallurgical Plant (kazatomprom)

- 6.4.11 Xiamen Beryllium Copper Technologies Co. Ltd

- 6.4.12 Xinjiang Xinxin Mining Industry Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Demand for Beryllium Oxide in Nuclear Power Generation

- 7.2 Emerging Applications of Beryllium Mirrors

- 7.3 Other Opportunities