|

市場調査レポート

商品コード

1685786

ボディアーマー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Body Armor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ボディアーマー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

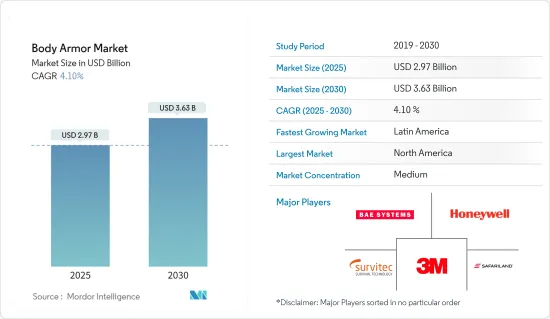

ボディアーマーの市場規模は2025年に29億7,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは4.1%で、2030年には36億3,000万米ドルに達すると予測されています。

地政学的緊張と暴力やテロの急増は、軍や法執行機関にとってボディアーマーの重要性を強調し、多様なシナリオで人員を保護しています。しかし、防護のレベルは、特定の脅威評価に合わせて変化します。

対反乱、対テロリズムおよびゲリラ戦に及ぶ軍の交戦は、潜在的に傷害か死亡者をもたらす重要な危険を、もたらします。同様に、法の執行では、警官は個人的なボディアーマーへの投資を必要とする犯罪者および重罪犯からの脅威に直面します。

ボディアーマーの市場の成長はもっぱら軍の要求によってしかし法の執行および民間部門によってますます運転されないです。ケブラーベースのソフトアーマーを含む柔軟で軽量なボディアーマーのような革新は、保護と着用者の快適さを優先しています。この需要は、特に安全保障上の課題が高まっている地域で、市場の拡大に拍車をかけています。DuPontやPoint-Blank EnterprisesのKevlar EXOのような注目すべき進歩は、市場の成長をさらに促進します。

超高分子量ポリエチレン(UHMWPE)やアドバンスト・セラミックスなどの先端材料の統合コストが生産コストを大幅に引き上げているため、普及が制限されているのです。

近年、主に需給ギャップを埋めることを目的とする政府によって、先端ボディアーマーへの投資が顕著に増加しています。その結果、市場は調達と開発活動の高まりを目の当たりにし、力強い成長の舞台を整えています。しかし、厳しい政府規制、特に民間部門では、市場の潜在力を十分に発揮することを妨げる、カウンターバランスとして機能します。

ボディアーマー市場の動向

予測期間中、ソフトアーマーとハードアーマーが市場シェアを独占

ボディアーマー市場において最も堅調な成長を遂げようとしているセグメントは、ソフトアーマーとハードアーマーの両方を包含しています。この急成長は、素材の進歩、個人保護ニーズの高まり、NATOや他の防衛組織のような組織からの多額の投資に起因しています。

NATOは最先端のボディアーマーの需要を推進する極めて重要な力です。その加盟国は一貫して高度の柔らかく、堅いボディアーマーに改善することの顕著な焦点の進化する脅威に、抗するために彼らの防衛兵器を増強します。これらの投資は部隊の安全性と有効性を強化するというNATOのコミットメントを強調するものです。特筆すべきは、NATOの進行中の近代化構想が軽量高性能装甲システムの採用を強調し、ボディアーマー市場の成長にさらに拍車をかけていることです。この動向は北米や欧州など国防支出が旺盛な地域で特に顕著です。例えば、2024年4月、サンディエゴの防衛ソリューション・プロバイダーであるBlack Box Safety Inc.は、Point Blank EnterprisesからCHP、Fish and Wildlife、State Parks、Forestry and Fire Protectionを含む様々なカリフォルニア州の法執行機関に最先端の弾道防護ギアを供給するための3,500万米ドルに相当する重要な5年契約を締結し、それによって州全体の役員の安全性を強化しました。

予測期間中、北米が市場シェアを独占

米国は世界最大の国防支出国であり、2024年度には国防予算に8,420億米ドルが割り当てられると予想されています。この予算は、軍隊の戦闘能力を維持・向上させるための幅広いプログラムに資金を提供します。重要なのは、防護具や高度で強化されたボディアーマーの研究、開発、試験、調達に必要な資金です。中国やロシアを含む戦略的敵対国から発せられる脅威に関する主要な焦点として、統合抑止が予算内で強調されており、兵士のためのPPEを含む軍装を継続的に近代化します。

材料科学と製造技術革新は、北米のボディアーマー市場を加速させています。超高分子量ポリエチレン(UHMWPE)、先端セラミック、最新の複合材料の進歩により、より軽く、より強く、より効果的なボディアーマーが誕生しました。素材は、兵士が着用する防具の重量を大幅に軽減しながら、より優れた耐弾性を提供し、機動性と快適性を大幅に向上させています。ショットショー2024のような展示会は、これらの進歩を実証し、現代の戦闘シナリオの厳しさを満たすために、次世代のボディアーマーを開発する業界の献身を展示しました。

米国国防総省は、新しいボディアーマーシステムを作成するためにいくつかのプログラムを開始しました。これらの中には、超軽量、高性能ボディアーマーの開発に集中するTorso &Extremities Protection(TEP)とWarrior Web Program(WWP)があります。さらに、デュポンやポイント・ブランク・エンタープライズのような重要な企業間の協力により、ケブラーEXOアラミド繊維を使用した最新のボディアーマーソリューションが市場に投入され、前例のない柔軟性と保護が可能になり、法執行機関や軍関係者の新たな要件を満たす最新のNIJ基準を満たしています。

最近の戦略的提携や買収により、北米はボディアーマー市場で最強のプレーヤーとなりました。例えばデュポンは、ポイント・ブランク・エンタープライズと協力して、快適さと機動性を損なうことなく保護を強化する、最も進歩的なボディアーマーソリューションを法執行機関に提供しています。この取引は、革新的な素材や技術を統合し、効果的で信頼性の高いボディアーマーの増加傾向に対応するためのより重要な傾向を象徴しています。

ボディアーマー業界の概要

ボディアーマー市場は半固定的であり、いくつかのローカルおよび世界プレーヤーが重要なシェアを占めています。市場のいくつかの顕著なプレーヤーはSafariland LLC、3M、Honeywell International Inc.、Survitec Group LimitedおよびBAE Systems PLCです。市場の主なプレーヤーは、軍用の先進的なソリューションの開発に非常に注力しています。

TenCateのようなボディアーマーOEMは、証明書のためのより困難な完了標準手順を持っている攻撃耐性材料および構造のための試験機関協会(VPAM)のような、より広範な防護規格に対応する製品を製造しています。

例えば、サービテック・グループ・リミテッドは2024年1月、特注プラスチックや工業用ファブリック製品の受託製造会社である米国のビニール・テクノロジー社を戦略的に買収しました。この買収により、サバイテックはパイロット用飛行用具の製造能力を強化し、高度な技術を要する縫製能力において有数の雇用主としての地位を確立しました。ビニール・テクノロジー社は、特にアドバンスド・テクノロジー・アンチGスーツなどの複雑な衣服製造に貢献します。この戦略的な動きは、サバイテックの製品ポートフォリオと製造能力を強化・向上させ、信頼されるサバイバル技術ソリューションへのアクセスを合理化し、ボディアーマー市場における存在感を強化します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ

- ソフトアーマーとハードアーマー

- ウェア

- ヘルメット

- アクセサリー

- エンドユーザー

- 軍事

- 民間および法執行機関

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- ELMON SA

- DuPont De Nemours Inc.

- Honeywell International Inc.

- U.S. Armor Corporation

- Point Blank Enterprises Inc.

- BAE Systems PLC

- EnGarde BV

- ArmorSource LLC

- Bluewater Defense Inc.

- Sarkar Tactical

- Survitec Group Limited

- Safariland LLC

- 3M

第7章 市場機会と今後の動向

The Body Armor Market size is estimated at USD 2.97 billion in 2025, and is expected to reach USD 3.63 billion by 2030, at a CAGR of 4.1% during the forecast period (2025-2030).

Geopolitical tensions and a surge in violence and terrorism have underscored the importance of body armor for military and law enforcement agencies, safeguarding their personnel in diverse scenarios. However, the level of protection varies, tailored to the specific threat assessments.

Military engagements, spanning counterinsurgency, counter-terrorism, and guerrilla warfare, pose significant risks, potentially leading to injuries or fatalities. Similarly, in law enforcement, officers face threats from criminals and felons, necessitating investments in personal body armor.

The body armor market's growth is not solely driven by military demand but increasingly by law enforcement and civilian sectors. Innovations like flexible, lightweight body armor, including Kevlar-based soft armor, prioritize protection and wearer comfort. This demand is fueling market expansion, particularly in regions facing heightened security challenges. Noteworthy advancements like DuPont and Point-Blank Enterprises' Kevlar EXO further propel market growth.

However, the market grapples with a significant hurdle: the integration costs of advanced materials, such as ultra-high-molecule weight polyethylene (UHMWPE) and advanced ceramics, significantly elevate production costs, limiting widespread adoption.

In recent years, there has been a notable increase in investments in advanced body armor, spurred mainly by governments aiming to bridge supply-demand gaps. Consequently, the market is witnessing heightened procurement and development activities, setting the stage for robust growth. Yet, stringent government regulations, especially in the civil sector, act as a counterbalance, impeding the market's full potential.

Body Armor Market Trends

Soft and Hard Armors to Dominate Market Share During the Forecast Period

The segment poised for the most robust growth within the body armor market encompasses both soft and hard armor. This surge can be attributed to advancements in materials, a rising need for personal protection, and substantial investments from entities like NATO and other defense organizations.

NATO is a pivotal force propelling the demand for cutting-edge body armor. Its member nations consistently bolster their defense arsenals to counter evolving threats, with a notable focus on upgrading to advanced soft and hard body armor. These investments underscore NATO's commitment to bolstering troop safety and effectiveness. Notably, NATO's ongoing modernization initiatives emphasize the adoption of lightweight, high-performance armor systems, further fueling the body armor market's growth. This trend is particularly pronounced in regions with robust defense expenditures, such as North America and Europe. For example, in April 2024, San Diego's Black Box Safety Inc., a defense solutions provider, clinched a significant 5-year contract worth USD 35 million for supplying cutting-edge ballistic protection gear from Point Blank Enterprises to various California law enforcement agencies, including CHP, Fish and Wildlife, State Parks, and Forestry and Fire Protection, thereby bolstering officer safety statewide.

North America to Dominate Market Share During the Forecast Period

The United States is the world's largest defense spender and is expected to allocate USD 842 billion for its defense budget in FY2024. This budget funds a wide array of programs designed to sustain and improve the combat capabilities of the armed forces. Crucial funding will be needed to research, develop, test, and procure protective gear and advanced and enhanced body armor. Integrated deterrence is highlighted within the budget as the primary focus regarding threats emanating from its strategic adversaries, which include China and Russia, and to continuously modernize the military gear, including PPE, for soldiers.

Materials science and manufacturing innovations have accelerated North America's body armor market. Advances in ultra-high-molecular-weight polyethylene (UHMWPE), advanced ceramics, and the latest composite materials have created lighter, stronger, and more effective body armor. Materials provide better ballistic resistance while substantially reducing the weight of armor worn by a soldier, greatly enhancing mobility and comfort. Exhibitions such as the Shot Show 2024 demonstrated these advancements and showcased the industry's dedication to developing next-generation body armor to meet the rigors of contemporary combat scenarios.

The US Department of Defense has initiated several programs to create new body armor systems. Among these are the Torso & Extremities Protection (TEP) and Warrior Web Program (WWP), concentrating on developing ultra-lightweight, high-performance body armor. Moreover, the cooperation among significant companies such as DuPont and Point Blank Enterprises has brought into the market the latest body armor solutions using Kevlar EXO aramid fiber, which allows for flexibility and protection without precedent and meets the latest NIJ standards to meet the new requirements of law enforcement and military personnel.

Recent strategic partnerships and acquisitions have further made North America the strongest player in the body armor market. DuPont, for instance, has been working with Point Blank Enterprises to offer law enforcement agencies some of the most progressive body armor solutions, which enhance protection without compromising comfort and mobility. The deal is emblematic of a more significant trend toward integrating innovative materials and technologies to meet growing calls for effective and reliable body armor.

Body Armor Industry Overview

The body armor market is semi-consolidated, with some local and global players holding significant shares. Some prominent players in the market are Safariland LLC, 3M, Honeywell International Inc., Survitec Group Limited, and BAE Systems PLC. The key players in the market are highly focused on developing advanced solutions for military forces.

Body armor OEMs, such as TenCate, manufacture products that cater to a broader spectrum of protective standards, such as the Association of Testing Agencies for Attack-Resistant Materials and Constructions (VPAM), which has a harder completion standard procedure for certificates.

For instance, in January 2024, Survitec Group Limited strategically acquired US-based Vinyl Technology, a contract manufacturer of custom plastic and industrial fabric products. The acquisition enhances Survitec's capabilities in producing pilot flight equipment, positioning it as the leading employer in highly skilled sewing capacity. Vinyl Technology will contribute to complex garment manufacturing, particularly in the Advanced Technology Anti-G Suit. The strategic moves will enhance and increase Survitec's product portfolio and manufacturing capabilities, streamlining access to trusted survival technology solutions and bolstering its market presence in the body armor market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Soft and Hard Armors

- 5.1.2 Clothing

- 5.1.3 Helmets

- 5.1.4 Accessories

- 5.2 End User

- 5.2.1 Military

- 5.2.2 Civil and Law Enforcement

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 ELMON SA

- 6.1.2 DuPont De Nemours Inc.

- 6.1.3 Honeywell International Inc.

- 6.1.4 U.S. Armor Corporation

- 6.1.5 Point Blank Enterprises Inc.

- 6.1.6 BAE Systems PLC

- 6.1.7 EnGarde BV

- 6.1.8 ArmorSource LLC

- 6.1.9 Bluewater Defense Inc.

- 6.1.10 Sarkar Tactical

- 6.1.11 Survitec Group Limited

- 6.1.12 Safariland LLC

- 6.1.13 3M