|

市場調査レポート

商品コード

1685773

南米のペットフード:市場シェア分析、産業動向、成長予測(2025年~2030年)South America Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米のペットフード:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 310 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

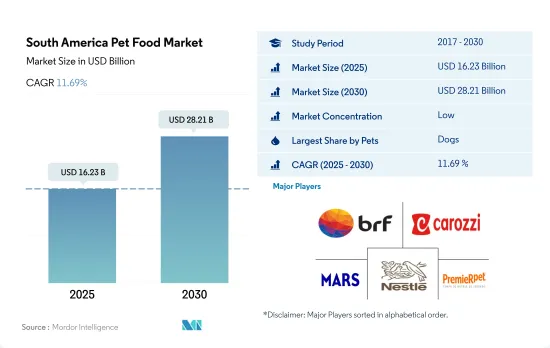

南米のペットフード市場規模は2025年に162億3,000万米ドルと推定され、2030年には282億1,000万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは11.69%で成長する見込みです。

犬への支出の増加とともに、家庭料理から市販フードへの移行が著しいため、犬が主要シェアを占める。

- 南米のペットフード市場は2017年から2022年にかけて80.7%増加しました。同市場の成長は、同地域の経済・社会情勢の変化と関連しており、中産階級の所得水準の急速な上昇により、ペットの飼育が急増し、ペットの人間化の動向がペットフード市場の需要を牽引しています。

- 南米のペットフード市場ではドッグフード部門が最大のシェアを占めており、2022年の市場規模は79億7,000万米ドルです。この優位性は、2017年から2022年の間に33.8%増加した犬への支出の増加とともに、同地域で家庭料理から市販のペットフードに移行するペットの飼い主が相当数いることと関連しており、2017年から2022年の間にこのセグメントの約84.9%の成長につながりました。

- 南米のペットフード市場では、キャットフード部門が最も高い成長率を示すと予想され、予測期間中のCAGRは12.7%と予測されます。これは、2017年から2022年の間に18.7%成長した猫の飼育数の大幅な増加によるものです。この猫数の増加により、キャットフード製品の消費者層が拡大しています。猫は他のペットと比べ、メンテナンスの必要性が低く、費用対効果が高いため、ペットとして人気を集めています。

- その他の動物には、鳥類、小型哺乳類、げっ歯類などが含まれます。これらの動物には特有の栄養要求があり、特殊なペットフード製品を通じてそれを満たす必要があります。この要因により、その他の動物用のペットフード分野は2017年から2022年の間に5億4,950万増加しました。

- ペット所有者の意識の高まりと地域におけるペット数の増加が、予測期間中のペットフード市場を牽引すると予想されます。

ペットの飼育増加とペットの栄養に関する意識の高まりが市場を牽引、ブラジルが優位国

- 南米のペットフード市場は、ペットの飼育数の増加、消費者の嗜好の変化、ペットの健康と栄養に関する意識の高まりといった様々な要因によって、近年大きな成長を遂げています。同市場は2022年には金額ベースで世界のペットフード市場の約7.1%を占めました。

- ブラジルは南米最大のペットフード市場であり、2022年には市場の63.6%を占めました。ブラジルの独占は主にペット数の多さによるものです。2022年現在、ブラジルのペット数は1億5,640万人で、南米のペット数の約58.5%を占めています。このようにペット数が多いことから、ブラジルのペットフード市場は予測期間中に13.3%のCAGRで推移すると予想されています。

- アルゼンチンは南米におけるペットフードの主要市場の一つであり、2022年の市場規模は11億3,000万米ドルでした。同国のペットフード市場はプレミアム化にシフトしています。同国におけるペット数の増加は、予測期間中にCAGR 15.9%で市場を牽引すると予測されており、そのため同地域の他の国々の中で最も急成長している市場となっています。

- その他南米は、2022年に市場の約26.5%を占めました。その他南米ではペット数が増加しており、その他南米のペットフード市場は予測期間中にCAGR 7.0%を記録すると予測されています。

- ペット数の増加、プレミアムフードへの需要の高まり、ペットの健康懸念に対する意識の高まりが、予測期間中の南米ペットフード市場の成長を後押しすると予想されます。

南米のペットフード市場動向

狭い居住空間への適応性とメンテナンスの手間の少なさから、ブラジルがこの地域で最大の猫飼育数を占める

- 南米のペット猫の飼育数は着実に増加しており、2019年から2022年の間に13.3%増加しました。この増加動向は、パンデミックによってもたらされた長期の自宅監禁期間中に、コンパニオンとしての猫の採用率が高まったことに起因すると考えられます。この地域の国々の中では、ブラジルが最も猫の数が多く、2022年時点で猫の総個体数の約55.5%を占めていました。南米では、2022年のペット数全体に占める猫の割合は19.3%でした。このように猫の割合が相対的に低いのは、犬がより実用的で価値のあるペットであるという文化的認識に起因している可能性があります。その結果、猫の数は同地域の犬の総個体数の50.0%に過ぎませんでした。

- しかし、猫は狭い居住空間でも窮屈さを感じることなく適応できること、犬に比べて維持費が安いことが、猫飼育への嗜好を高める一因となりました。この動向により、この地域全体で猫のペット数が大幅に増加しました。ブラジルだけでも、2020年時点で約1,430万世帯が猫をペットとして飼っています。同様にアルゼンチンでも猫の飼育率は高く、31.4%、460万世帯が猫をペットとして飼っています。

- この地域の重要な新たな動向は、猫カフェの設立です。2021年現在、ブラジルには約20の猫カフェがあり、客に快適な環境で猫と触れ合いながら飲み物を楽しむというユニークな機会を提供しています。このような猫カフェの動向の高まりと、猫が小さな居住空間を採用する能力は、この地域で人気のペットとしての猫の採用をさらに促進する可能性があります。

ブラジルは、高所得者とプレミアム化により、この地域で最も高いペット支出で際立っています。

- 南米におけるペット支出は一貫した成長を示し、2019年から2022年の間に約18.1%増加しました。この増加動向は、同地域全体でのペット飼育者数の増加に起因していると考えられます。ブラジルでは、ペットを所有する世帯数は1.3%のCAGRを記録し、アルゼンチンでは2016年から2020年の間に1.4%のCAGRを記録しました。

- 同地域のペットオーナーは、ペットの人間化にますます重点を置くようになっており、高所得者層は天然成分を使用した製品を選ぶことで売上成長を促進し、ペット製品のプレミアム化を推進しています。例えば、ブラジルにおけるプレミアムドライドッグフードの小売販売額は、2016年の3億3,570万米ドルから2020年には5億6,740万米ドルへと大幅に増加し、CAGRは14.7%を記録しました。この需要の急増は、プレミアムペット製品に対する嗜好の高まりを反映しています。2017年から2022年にかけて、ペットフードに支出する飼い主の数は、犬で年間約33.8%、猫で21.7%、その他のペット動物で12.7%増加しました。南米諸国の中ではブラジルが突出して1匹当たりのペット支出額が高く、2022年には455.8米ドルに達し、僅差でアルゼンチンの428.3米ドルが続いた。ブラジルのペット支出額が高いのは、同国のペット数が多いことが主因です。

- 流通チャネルの中では、ペットショップ、動物病院、スーパーマーケットといったオフラインの小売チャネルが、この地域でペットフード製品を購入するのに好まれている流通チャネルです。しかし、パンデミックの間、ペットフードの流通におけるeコマースのシェアは、2019年から2021年の間に約14.2%増加しました。

- プレミアムペットフードの消費量の増加とペットの人間化の進展は、予測期間中に同地域のペット支出を促進すると予測される要因です。

南米のペットフード産業概要

南米のペットフード市場は断片化されており、上位5社で27.62%を占めています。この市場の主要企業は以下の通りです。 BRF Global, Empresas Carozzi SA, Mars Incorporated, Nestle(Purina)and PremieRpet.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他のペット

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ペットフード製品

- フード

- サブプロダクト別

- ドライペットフード

- 製品別

- キブル

- その他ドライフード

- ウェット・ペットフード

- ペット用栄養補助食品・サプリメント

- サブプロダクト別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット用おやつ

- サブプロダクト別

- カリカリおやつ

- デンタル・トリーツ

- フリーズドライ&ジャーキートリーツ

- ソフト&モチートリーツ

- その他のおやつ

- ペット用動物飼料

- サブプロダクト別

- 糖尿病

- 消化器過敏症用

- オーラルケア

- 腎臓

- 尿路疾患

- その他の動物用飼料

- フード

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンライン・チャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- アルゼンチン

- ブラジル

- その他南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Alltech

- BRF Global

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- Empresas Carozzi SA

- Farmina Pet Foods

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- PremieRpet

- Virbac

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 47318

The South America Pet Food Market size is estimated at 16.23 billion USD in 2025, and is expected to reach 28.21 billion USD by 2030, growing at a CAGR of 11.69% during the forecast period (2025-2030).

Dogs held the major share due to significant transitioning from home-cooked food to commercial food along with the growing expenditures on dogs

- The South American pet food market increased by 80.7% between 2017 and 2022. The market's growth is associated with the changing economic and social landscape in the region, and the rapid increase in middle-class income levels has resulted in a surge in pet ownership and pet humanization trends, driving the demand for the pet food market.

- The dog food segment holds the largest share of the South American pet food market, with a market value of USD 7.97 billion in 2022. This dominance was associated with a significant number of pet owners transitioning from home-cooked food to commercial pet food in the region, along with the growing expenditures on dogs that increased by 33.8% between 2017 and 2022, leading to a growth of approximately 84.9% in this segment between 2017 and 2022.

- The cat food segment is expected to experience the highest growth rate in the South American pet food market, with a projected CAGR of 12.7% during the forecast period. This is owing to the significant increase in the cat population, which grew by 18.7% between 2017 and 2022. This rise in the number of cats has created a larger consumer base for cat food products. Cats are gaining popularity as pets due to their low maintenance requirements and cost-effectiveness compared to other pets.

- The other animals include birds, small mammals, rodents, and others. These animals have unique nutritional requirements that need to be fulfilled through specialized pet food products. This factor helped the pet food segment for other animals increased by 549.5 million between 2017 and 2022.

- The increasing awareness among pet owners and the growing population of pets in the region is expected to drive the pet food market during the forecast period.

Increasing pet ownership and rising awareness about pet nutrition are driving the market, with Brazil as a dominant country

- The South American pet food market has experienced significant growth in recent years, driven by various factors such as increasing pet ownership, changing consumer preferences, and rising awareness about pet health and nutrition. The market accounted for about 7.1% of the global pet food market in terms of value in 2022.

- Brazil is the largest pet food market in South America, and it accounted for 63.6% of the market in 2022. The domination of Brazil is mainly due to its large pet population. As of 2022, it had a pet population of 156.4 million, accounting for about 58.5% of the South American pet population. With this large pet population, the Brazilian pet food market is anticipated to record a CAGR of 13.3% during the forecast period.

- Argentina is one of the major markets for pet food in South America, which was valued at USD 1.13 billion in 2022. The country's pet food market is shifting toward premiumization. The increasing pet population in the country is anticipated to drive the market at a CAGR of 15.9% during the forecast period, thus making it the fastest-growing market among other countries in the region.

- The Rest of South America held about 26.5% of the market in 2022. The pet population in the Rest of South America is growing, and the pet food market in the Rest of South America is anticipated to register a CAGR of 7.0% during the forecast period.

- The rising pet population, growing demand for premium foods, and increasing awareness about health concerns in pets are anticipated to boost the growth of the South American pet food market during the forecast period.

South America Pet Food Market Trends

Brazil accounted for the largest cat population in the region owing to their adaptability to smaller living spaces and lower maintenance

- The pet cat population in South America has been steadily increasing, and it increased by 13.3% between 2019 and 2022. This upward trend could be attributed to the higher adoption rates of cats as companions during the extended periods of home confinement brought on by the pandemic. Among the countries in the region, Brazil had the largest cat population, accounting for about 55.5% of the total cat population as of 2022. In South America, cats comprised 19.3% of the overall pet population in 2022. This relatively lower proportion of cats could be attributed to the cultural perception that dogs are more practical and valued pets. As a result, the number of cats represented only 50.0% of the total dog population in the region.

- However, the adaptability of cats to smaller living spaces, without feeling confined, coupled with their lower maintenance costs compared to dogs, contributed to an increased preference for cat ownership. This trend led to a significant rise in the pet cat population across the region. In Brazil alone, as of 2020, about 14.3 million households owned cats as pets. Similarly, in Argentina, the rate of cat ownership was higher, with 31.4% of households, or 4.6 million households, having cats as pets.

- An important emerging trend in the region is the establishment of cat cafes. As of 2021, around 20 cat cafes were in Brazil, providing customers with a unique opportunity to enjoy a drink while interacting with cats in a comfortable setting. This growing trend of cat cafes and the cat's ability to adopt smaller living spaces can further enhance the adoption of cats as popular pets in the region.

Brazil stands out with the highest pet expenditure in the region due to higher-income individuals and premiumization

- Pet expenditure in South America showed consistent growth, with an increase of about 18.1% between 2019 and 2022. This upward trend could be attributed to the increased number of pet owners across the region. In Brazil, the number of households owning a pet recorded a CAGR of 1.3%, while in Argentina, it recorded a CAGR of 1.4% between 2016 and 2020.

- Pet owners in the region are increasingly focused on pet humanization, with higher-income individuals driving sales growth by opting for products made with natural ingredients, driving pet product premiumization. For instance, the retail sales value of premium dry dog food in Brazil witnessed a significant rise from USD 335.7 million in 2016 to USD 567.4 million in 2020, recording a CAGR of 14.7%. This surge in demand reflected the growing preference for premium pet products. From 2017 to 2022, the number of pet owners spending on pet food increased by about 33.8% annually for dogs, 21.7% for cats, and 12.7% for other pet animals. Among the South American countries, Brazil stood out with the highest pet expenditure per animal, reaching USD 455.8, followed closely by Argentina at USD 428.3 in 2022. This higher pet expenditure in Brazil was largely due to the country's larger pet population.

- Among distribution channels, offline retail channels such as pet shops, vet clinics, and supermarkets are the preferred distribution channels for purchasing pet food products in the region. However, during the pandemic, e-commerce's share in the distribution of pet food increased by about 14.2% between 2019 and 2021.

- The higher consumption of premium pet food and growing pet humanization are the factors anticipated to drive pet expenditure in the region during the forecast period.

South America Pet Food Industry Overview

The South America Pet Food Market is fragmented, with the top five companies occupying 27.62%. The major players in this market are BRF Global, Empresas Carozzi SA, Mars Incorporated, Nestle (Purina) and PremieRpet (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Pet Food Product

- 5.1.1 Food

- 5.1.1.1 By Sub Product

- 5.1.1.1.1 Dry Pet Food

- 5.1.1.1.1.1 By Product

- 5.1.1.1.1.1.1 Kibbles

- 5.1.1.1.1.1.2 Other Dry Pet Food

- 5.1.1.1.2 Wet Pet Food

- 5.1.2 Pet Nutraceuticals/Supplements

- 5.1.2.1 By Sub Product

- 5.1.2.1.1 Milk Bioactives

- 5.1.2.1.2 Omega-3 Fatty Acids

- 5.1.2.1.3 Probiotics

- 5.1.2.1.4 Proteins and Peptides

- 5.1.2.1.5 Vitamins and Minerals

- 5.1.2.1.6 Other Nutraceuticals

- 5.1.3 Pet Treats

- 5.1.3.1 By Sub Product

- 5.1.3.1.1 Crunchy Treats

- 5.1.3.1.2 Dental Treats

- 5.1.3.1.3 Freeze-dried and Jerky Treats

- 5.1.3.1.4 Soft & Chewy Treats

- 5.1.3.1.5 Other Treats

- 5.1.4 Pet Veterinary Diets

- 5.1.4.1 By Sub Product

- 5.1.4.1.1 Diabetes

- 5.1.4.1.2 Digestive Sensitivity

- 5.1.4.1.3 Oral Care Diets

- 5.1.4.1.4 Renal

- 5.1.4.1.5 Urinary tract disease

- 5.1.4.1.6 Other Veterinary Diets

- 5.1.1 Food

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Alltech

- 6.4.3 BRF Global

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 Empresas Carozzi SA

- 6.4.6 Farmina Pet Foods

- 6.4.7 General Mills Inc.

- 6.4.8 Mars Incorporated

- 6.4.9 Nestle (Purina)

- 6.4.10 PremieRpet

- 6.4.11 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms