尿路感染症治療薬- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Urinary Tract Infection Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 112 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685691

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

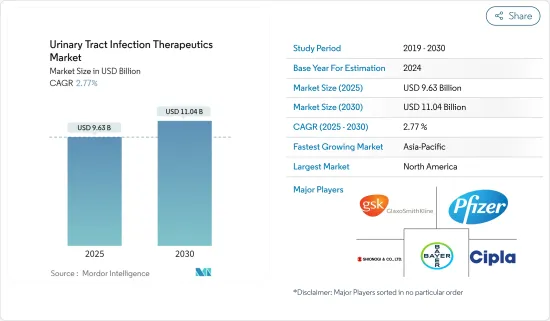

尿路感染症治療薬市場規模は2025年に96億3,000万米ドルと推計され、予測期間(2025年~2030年)のCAGRは2.77%で、2030年には110億4,000万米ドルに達すると予測されます。

コロナウイルス感染患者のかつてない増加は、他のプライマリケアサービスへのアクセスを低下させ、尿路感染症などCOVID-19に関連しない診断の大幅な低下をもたらしました。2020年の尿路感染症診断の週間率はわずかに低下し、これがここ数ヶ月の業界の成長を鈍化させた可能性があります。2020年12月にADIAN Journalに掲載された研究によると、COVID-19の流行による尿路感染症(UTI)診断の大幅な減少が懸念されます。COVID-19感染者がSARS-CoV-2に感染したとき、パンデミックはプライマリ・ケアを劇的に変えました。その結果、プライマリケアサービスを求める患者が減少し、尿路結石を含む診断も減少しました。2020年3月30日から4月24日の間に、人口10万人当たりの尿路結石診断の週間率は、イングランドの平均30-35から10未満に減少しました。4月以降、通常の50%の割合で上昇しています。尿路結石診断率の上昇は、市場成長にプラスの影響を与えています。市場成長を促進する要因には、糖尿病や腎臓結石の有病率の増加、配合剤の発売などがあります。

米国家庭医学会(AAFP)によると、2020年3月、レオナルド・フェレイラ氏によって、腎臓結石は一般的な病気であり、年間発生率は1,000人当たり8例でした。同出典によると、男性の約13%、女性の約7%が一生の間に腎臓結石を発症する可能性があり、米国における尿閉の総発生率は男性1,000人当たり年間4.5~6.8人です。さらに、国際糖尿病連合が2021年に発表した報告書によると、2020年に糖尿病に罹患した20~79歳の人は世界で約4億6,300万人でした。この数は、2030年には6億4,300万人、2045年には7億人に増加すると予測されています。ほとんどの国で2型糖尿病患者の割合が増加しており、低・中所得国では成人の79%が糖尿病にかかっています。尿路感染症は、尿中の糖分が細菌の温床となるため、糖尿病患者にとって特に厄介なものとなります。したがって、糖尿病と腎結石の有病率の増加に伴い、尿路感染症(UTI)の症例数が増加し、薬剤の需要が増加するため、世界の尿路感染症治療薬市場を牽引しています。

加えて、より効率的な配合剤の発売や老人人口の増加が、尿路感染症治療薬市場の成長を後押しすると予想されています。例えば、フランスの製薬会社Allecra社は2020年2月、新規のスペクトラム延長型βラクタマーゼ阻害薬であるエンメタゾバクタムと第4世代セファロスポリンであるセフェピムの配合剤Exblifepを発表し、複雑性尿路感染症を対象とした臨床試験で主要評価項目を達成しました。

しかし、薬の使用に伴う有害事象や、新興諸国や低開発国における尿路結石の有病率に関する認識不足が、市場の成長を抑制しています。

尿路感染症(UTI)治療薬市場の動向

尿路感染症治療薬市場では複雑性尿路結石セグメントが大きなシェアを占める見込み

薬剤耐性菌の増加や抗生物質の過剰使用により、複雑性尿路結石の有病率は今後増加すると予想されます。大多数の医師は、複雑性尿路結石症例の治療にキノロン系抗菌薬を処方しています。セファロスポリンは複雑性尿路結石症例に処方される2番目に多い薬剤です。

2020年にInternational Journal of Molecular medicineに掲載された論文によると、腎結石症は腎結石症または尿路結石症とも呼ばれ、医学上最も古い疾患の一つです。11%の人が生涯のどこかで腎結石を発症すると推定されており、腎結石の有病率と発症率は世界的に増加しています。しかし、尿路結石の全体的な有病率は11.2%で、調査対象者の48.8%が第一度親族にこの病気を持つ人がいた。男性は女性より1.8倍尿石症に罹患する可能性が高かったです。全体として、複雑性尿路結石の有病率は予測期間中に増加すると見られており、これは主に尿路結石症例における耐性菌の増加と尿路結石の再発率の上昇に起因しています。

しかし、米国食品医薬品局からの承認の増加や主要企業による製品発売が市場を押し上げると予想されます。例えば、2019年7月、米国食品医薬品局は、成人の複雑性尿路感染症(cUTI)および複雑性腹腔内感染症(cIAI)を治療するための抗菌薬製品であるMerck and CompanyのRecarbrio(イミペネム、シラスタチン、およびレリバクタム)を承認しました。

このように、cUTIの有病率の上昇や製品上市の増加といった前述の要因はすべて、予測期間中にこのセグメントを押し上げると予想されます。

北米が予測期間中に大きな市場シェアを占める見込み

この地域では、尿路結石に使用される診断手法に関する技術革新が急激に増加しています。2020年11月にInfectious Diseases Society of Americaに掲載されたPranita D. Tammaの論文によると、尿路結石の定期検診中に、ある女性が最後の砦である抗生物質コリスチンに耐性を示す大腸菌に感染していることが観察されました。コリスチン耐性菌の発見は大きな問題とされました。さらに、CDCは他の組織と共同で、米国におけるカテーテル関連尿路結石やその他のヘルスケア関連感染を予防するためのガイドラインを作成しました。さらに、Queensland Pediatric Factsheet 2019は、7歳までに女児の約10人に1人、男児の約50人に1人が尿路感染症に罹患すると推定しています。1歳未満の感染症は男児に多いが、年長児では女児に多いです。

さらに、2019年5月に『Therapeutic Advances in Urology』に掲載された「Anイントロダクション to the Epidemiology and Burden of Urinary Tract Infections」と題する研究によると、尿路感染症(UTI)は成人女性の外来感染症で最も多く、生涯有病率は50~60%です。尿路感染症は社会的にも個人的にも大きな負担となっており、米国では毎年かなりの数の受診が尿路感染症によって占められています。この疾患は、尿路感染症治療薬の売上を増加させ、市場を牽引すると予想されます。

さらに、尿路感染症用の新規クラスの抗生物質の研究開発は、市場の成長を助けると期待されています。例えば、2020年8月には、カリフォルニア工科大学の研究者が、細菌の鉄獲得を標的とする新しいクラスの尿路感染症用抗生物質の開発を発表しました。

このように、前述の要因はすべて、予測期間中に同地域の市場を押し上げると予想されます。

尿路感染症治療薬業界の概要

尿路感染症治療薬市場は細分化された競合市場であり、多数の大手企業で構成されています。現在市場を独占している企業には、AstraZeneca、Bayer AG、Cipla Inc.、GlaxoSmithKline PLC、塩野義製薬、Novartis AG、ファイザーなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 糖尿病および腎結石の増加

- 配合剤の発売

- 市場抑制要因

- 薬の使用に伴う副作用

- 新興諸国および低開発諸国における認識不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 医薬品

- ペニシリンとその配合剤

- キノロン系抗菌薬

- セファロスポリン

- アゾールおよびアムホテリシンB

- ニトロフラン

- その他の医薬品(アミノグリコシド抗体、スルホンアミド、テトラサイクリンなど)

- 適応症

- 合併症性尿路結石症

- 合併症のない尿路結石

- その他の適応症(合併症を繰り返す尿路結石、神経因性膀胱感染症など)

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- AstraZeneca

- Bayer AG

- Cipla Inc.

- GlaxoSmithKline PLC

- Shionogi & Co. Ltd

- Novartis AG

- Pfizer

- Merck & Co. Inc

- Bristol-Myers Squibb Company

- Almirall SA

- Dr. Reddys Laboratories Ltd

- Allergan

第7章 市場機会と今後の動向

目次

The Urinary Tract Infection Therapeutics Market size is estimated at USD 9.63 billion in 2025, and is expected to reach USD 11.04 billion by 2030, at a CAGR of 2.77% during the forecast period (2025-2030).

The unprecedented increase in coronavirus-infected patients had reduced access to other primary care services and resulted in a significant drop in non-COVID-19-related diagnoses, such as urinary tract infection. The weekly rate of UTI diagnosis fell slightly in 2020, which may have slowed the industry's growth in recent months. According to a study published in the ADIAN Journal in December 2020, a significant decrease in urinary tract infection (UTI) diagnoses due to the COVID-19 pandemic raises concern. When people with COVID-19 were infected with SARS-CoV-2, the pandemic changed primary care dramatically. This resulted in fewer patients seeking primary care services and fewer diagnoses, including UTIs. Between March 30 and April 24, 2020, the weekly rate of UTI diagnosis per 100,000 population fell from an average of 30-35 to less than 10 in England. Since April, the rate has risen by 50% of the usual rate. The increase in the rate of UTI diagnosis has positively impacted market growth. Certain factors driving the market growth include the increasing prevalence of diabetes and kidney stones and the launch of combination drugs.

According to the American Academy of Family Physicians (AAFP), in March 2020, by Leonardo Ferreira, kidney stones were a common ailment, with an annual incidence of eight instances per 1,000 persons. As per the same source, around 13% of men and 7% of women may develop a kidney stone during their lifetime, and the total incidence of urinary retention in the US is 4.5 to 6.8 per 1,000 men per year. Moreover, according to the International Federation of Diabetics report in 2021, diabetes affected approximately 463 million persons aged 20 to 79 years worldwide in 2020. This number is anticipated to climb to 643 million by 2030 and 700 million by 2045. In most countries, the proportion of people with Type 2 diabetes is increasing, and diabetes affects 79% of adults in low- and middle-income countries. Urinary tract infections can be especially troublesome for people with diabetes because sugar in the urine serves as a breeding ground for bacteria. Therefore, with the increasing prevalence of diabetes and kidney stones, the number of cases of urinary tract infection (UTI) increases, increasing the demand for drugs, thus, driving the global urinary tract infection therapeutics market.

Additionally, the launch of more efficient combination drugs and the increasing geriatric population is expected to boost the growth of the urinary tract infection therapeutics market. For instance, in February 2020, Allecra, a French pharmaceutical company, announced Exblifep, a combination of enmetazobactam, a novel extended-spectrum beta-lactamase inhibitor, and cefepime, a fourth-generation cephalosporin that met primary endpoints in a clinical trial for complicated UTIs.

However, adverse events associated with the use of medication and the lack of awareness about the prevalence of UTIs in developing and underdeveloped countries are restraining the market's growth.

Urinary Tract Infection (UTI) Therapeutics Market Trends

Complicated UTIs Segment Expected to Hold a Major Share in the Urinary Tract Infection Therapeutics Market

The prevalence of complicated UTIs is expected to increase in the future, owing to the rise in drug-resistant bacteria and excessive use of antibiotics. A vast majority of physicians prescribe quinolones to treat complicated UTI cases. Cephalosporin is the second-most common drug prescribed for complicated UTI cases.

According to an article published in the International Journal of Molecular medicine in 2020, kidney stone disease, also known as nephrolithiasis or urolithiasis, is one of medicine's oldest diseases. It is estimated that 11% of people will develop kidney stones at some point in their lives, and the prevalence and incidence of kidney stones are increasing worldwide. However, the overall prevalence of urolithiasis was 11.2%, with 48.8% of those surveyed having a first-degree relative with the disease. Males were 1.8 times more likely than females to have urolithiasis. Overall, the prevalence of complicated UTIs is set to increase during the forecast period, mainly owing to the increasing bacterial resistance in UTI cases and the rise in recurrence rate for UTIs.

However, increasing approvals from the US Food and Drug Administration and product launches by key players are expected to boost the market. For instance, in July 2019, the US Food and Drug Administration approved Merck and Company's Recarbrio (imipenem, cilastatin, and relebactam), an antibacterial drug product to treat adults with complicated urinary tract infections (cUTI) and complicated intra-abdominal infections (cIAI).

Thus, all aforementioned factors such as rising prevalence of cUTIs and increasing product launches are expected to boost the segment over the forecast period.

North America Expected to Hold Significant Market Share in the Forecast Period

The region is experiencing a drastic increase in innovations related to diagnostic methodologies used for UTIs. According to the article published in Infectious Diseases Society of America in November 2020, by Pranita D. Tamma, during a routine checkup for a UTI, a woman was observed to be infected by E. coli that showed resistance to the last-resort antibiotic, Colistin. The discovery of Colistin-resistant bacteria was considered a major issue. In addition to that, the CDC, in collaboration with other organizations, developed guidelines for preventing catheter-associated UTIs and other healthcare-associated infections in the US. Furthermore, the Queensland Pediatric Factsheet 2019 estimated that approximately 1 in 10 girls and 1 in 50 boys would suffer from a urinary tract infection by seven years of age. Infections in children under one year are more common in boys, but in older children, infections are more common in girls.

Additionally, according to a study published in Therapeutic Advances in Urology in May 2019 titled, "An Introduction to the Epidemiology and Burden of Urinary Tract Infections," urinary tract infections (UTIs) are the most common outpatient infections in adult women, with a lifetime prevalence of 50-60%. UTIs are a substantial societal and personal burden, with UTIs accounting for a significant number of medical visits in the US each year. This condition is expected to drive the market by increasing the sales of urinary tract infection medicines.

Furthermore, research and development of novel classes of antibiotics for urinary tract infections are expected to aid in market growth. In August 2020, for example, researchers at California Polytechnic State University announced the development of a new class of antibiotics for urinary tract infections that target bacterial iron acquisition.

Thus, all aforementioned factors are expected to boost the market in the region over the forecast period.

Urinary Tract Infection (UTI) Therapeutics Industry Overview

The urinary tract infection therapeutics market is fragmented and competitive and consists of a number of major players. Some of the companies currently dominating the market are AstraZeneca, Bayer AG, Cipla Inc., GlaxoSmithKline PLC, Shionogi & Co. Ltd, Novartis AG, and Pfizer, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Diabetes and Kidney Stones

- 4.2.2 Launch of Combination Drugs

- 4.3 Market Restraints

- 4.3.1 Adverse Effects Associated with the Use of Medication

- 4.3.2 Lack of Awareness in Developing and Underdeveloped Countries

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 Drug

- 5.1.1 Penicillin and Combinations

- 5.1.2 Quinolones

- 5.1.3 Cephalosporin

- 5.1.4 Azoles and Amphotericin B

- 5.1.5 Nitrofurans

- 5.1.6 Other Drugs (Aminoglycoside Antibodies, Sulphonamides, Tetracycline, etc.)

- 5.2 Indication

- 5.2.1 Complicated UTI

- 5.2.2 Uncomplicated UTI

- 5.2.3 Other Indications (Recurring Complicated UTI, Neurogenic Bladder Infection, etc.)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 US

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 UK

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AstraZeneca

- 6.1.2 Bayer AG

- 6.1.3 Cipla Inc.

- 6.1.4 GlaxoSmithKline PLC

- 6.1.5 Shionogi & Co. Ltd

- 6.1.6 Novartis AG

- 6.1.7 Pfizer

- 6.1.8 Merck & Co. Inc

- 6.1.9 Bristol-Myers Squibb Company

- 6.1.10 Almirall SA

- 6.1.11 Dr. Reddys Laboratories Ltd

- 6.1.12 Allergan

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 112 Pages

- 納期

- 2~3営業日