|

市場調査レポート

商品コード

1684056

医療機器用MLCC:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Medical Devices MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医療機器用MLCC:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 224 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

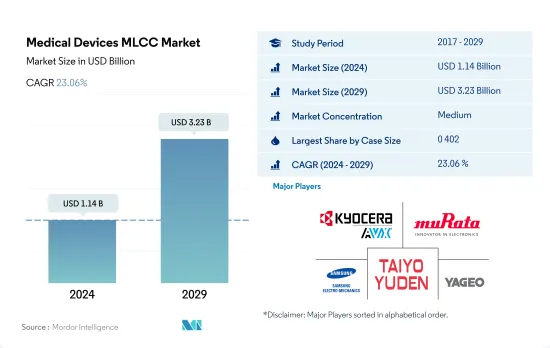

医療機器用MLCC市場規模は、2024年に11億4,000万米ドルと推定され、2029年には32億3,000万米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは23.06%で成長します。

進化する医療機器におけるMLCCの影響力が高まる

- 世界の医療機器用MLCC市場は、ヘルスケア支出の増加と先進医療機器への需要に牽引され、大きな成長を遂げています。市場はケースサイズによって区分され、主要サイズは明確な技術的進歩を提供し、特定の医療ニーズに対応しています。

- 0.402MLCCは小型で大容量であるため、最先端の医療機器に不可欠な部品です。慢性疾患の管理、患者の健康増進、ヘルスケアイノベーションの推進において極めて重要な役割を果たしています。関節炎やがんなどの慢性疾患の増加は、0 603 MLCCの需要に拍車をかけています。これらの部品は、早期発見と正確な診断のためにMRIやCTスキャンを行う機器に不可欠です。

- AIを搭載した医療用ロボットやウェアラブル医療用センサーの出現が、0 805 MLCCの需要を押し上げています。これらの部品は、医療機器のAIやロボット機能に電力を供給し、手術ロボットやリハビリロボットがその動向をリードしています。1 206 MLCCは、AI主導の診断ツールやウェアラブル医療センサーで重要な役割を果たします。がんや心房細動のような疾患が蔓延し続ける中、正確で効率的な診断が最重要となっています。

- 特定の医療用インプラントのニーズに対応する過程で、1 210 MLCCは、人口動態の変化や美容施術によって推進される医療用インプラントの多様な状況と整合します。人口の高齢化と美容手術の増加に伴い、特殊な医療用インプラントの需要が高まっています。その他のケースサイズ・セグメントは、進化する医療技術に適応し、明確なデバイス設計と空間的制約に対応しています。

医療機器の技術革新が、大陸を越えてMLCCの成長を促進しています。

- アジア太平洋は、ヘルスケア市場における大きなビジネスチャンスに後押しされ、医療機器産業のダイナミックなハブとして台頭しました。世界の心臓病負担の60%を占めるインドは、医療機器製造能力を確立するために420億米ドルを投資し、日本との協力を目指しています。このパートナーシップは、患者モニターや心臓カテーテルのような先端機器の製造におけるMLCCの活用と一致しています。

- 北米のヘルスケア事情は、心臓病や脳卒中などの慢性疾患の負担が大きいことが特徴です。MLCCは、こうした課題に対応するコンパクトで信頼性の高い医療機器を製造する能力を提供します。何百万人ものアメリカ人が慢性疾患を抱えて生活しているため、MLCCを統合した医療ソリューションに対する需要が高まっており、患者の転帰を向上させる上でMLCCが重要な役割を果たすことが強調されています。

- 欧州最大のヘルスケア市場は、高齢化と慢性疾患の増加によって牽引されています。MLCCを搭載したウェアラブル医療機器は、糖尿病や心血管障害といった疾患の管理に役立っています。小型化されたコンポーネントの需要はMLCCの能力と合致しており、電力管理やワイヤレス接続のためにウェアラブル機器への統合を容易にしています。

- その他中東・アフリカ(MEA)を含む世界のその他の地域(RoW)には、機会と課題があります。MEA地域は医療機器と医薬品に大きな可能性を示しています。中東のヘルスケア部門は、医療技術や医薬品への投資を原動力に、2026年までに4,080億AEDの収益に達すると予測されています。MLCCを組み込んだものを含む先進医療機器への需要が急増しており、同地域のヘルスケア拡大と技術重視の姿勢に合致しています。

世界の医療機器用MLCC市場動向

医療モノのインターネットの普及と機器の技術進歩がヘルスケア支出を促進

- ヘルスケア業界は、革新的なウェアラブルデバイスの採用拡大など、著しい技術進歩を経験しており、MLCCにとって有望な市場となっています。医療やヘルスケア・アプリケーションで使用される相互接続デバイスを含む医療モノのインターネット(IoMT)の人気の高まりは、今後数年にわたってMLCCに数多くの機会を生み出すと思われます。[1]

- COVID-19パンデミックの間、世界のヘルスケア支出は大幅に急増し、2020年には世界GDPの10.8%に相当する9兆米ドルに達しました。注目すべきは、この支出の配分が所得層によって大きく異なることです。政府支出は、2020年の医療費増加の主な要因でした。すべての所得層で、一人当たりの政府保健支出は増加し、前年度の伸び率を上回りました。[2]

- 差し迫ったパンデミックや大災害に対するヘルスケアの準備態勢を強化するため、調査、緊急対応能力、ヘルスケア・インフラへの投資が増加しています。政府やヘルスケア機関は、起こりうる健康危機を管理し、その影響を軽減するために、調査、緊急対応訓練、インフラの強化といった事前対策の必要性を認識しています。迅速かつ効率的な緊急対応を確保することで、こうした分野への医療支出に対する需要が高まっています。

ウェアラブル技術市場の戦略的適応が医療機器用MLCCの需要を増強

- 2020年、ヒアラブル、腕時計、リストバンド、その他のウェアラブルの世界市場は著しい急成長を遂げ、出荷額は4億4,470万米ドルに達し、前年比28.38%の大幅な成長率を示しました。しかし、2021年には前年比19.99%と成長率が鈍化し、勢いはやや鈍化しました。その結果、2022年には7.7%減となったが、これは主にマクロ経済情勢が厳しく、2021年の例外的な業績に匹敵する業績を達成するのが困難であったことによる。

- この落ち込みは、市場の飽和に部分的に起因しています。ウェアラブルデバイス部門は、前年度に大幅な拡大を示しており、相当数の潜在顧客がすでにそうしたデバイスを採用していたため、需要の減少につながりました。需要を喚起し、勢いを取り戻すために、ベンダーは、より低価格の代替品の提供、魅力的な下取りオファーの導入、融資オプションの提供、サブスクリプション・サービスの導入などの戦略的手段を採用しています。さらに、さまざまな機能セットや価格帯の機器を取り入れることで製品ポートフォリオを多様化し、その周囲に強固なエコシステムを構築している企業は、市場が成長軌道を取り戻した後に報酬を得る立場にあります。

医療機器用MLCC業界の概要

医療機器MLCC市場は適度に統合されており、上位5社で57.03%を占めています。この市場の主要企業は以下の通り。 Kyocera AVX Components Corporation(Kyocera Corporation), Murata Manufacturing, Samsung Electro-Mechanics, Taiyo Yuden and Yageo Corporation(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ヘルスケア支出

- 世界の医療費

- 医療機器導入率

- 世界の医療機器普及率

- ウェアラブル売上高

- 世界の医療用ウェアラブル販売台数

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- ケースサイズ

- 0 402

- 0 603

- 0 805

- 1 206

- 1 210

- その他

- 電圧

- 100V~500V

- 500V以上

- 100V未満

- 静電容量

- 10μF~100μF

- 10μF未満

- 100μF以上

- 誘電タイプ

- クラス1

- クラス2

- 地域

- アジア太平洋

- 欧州

- 北米

- 世界のその他の地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Yageo Corporation

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Medical Devices MLCC Market size is estimated at 1.14 billion USD in 2024, and is expected to reach 3.23 billion USD by 2029, growing at a CAGR of 23.06% during the forecast period (2024-2029).

The influence of MLCCs in the evolving medical device landscape is growing

- The global medical devices MLCC market is experiencing significant growth, driven by growing healthcare expenditure and demand for advanced medical devices. The market is segmented by case size, with key sizes offering distinct technological advancements and addressing specific medical needs.

- Due to their compact size and high capacity, 0 402 MLCCs are critical components in cutting-edge medical devices. They play a pivotal role in managing chronic ailments, improving patients' well-being, and driving healthcare innovations. The increasing prevalence of chronic diseases like arthritis and cancer spurs the demand for 0 603 MLCCs. These components are essential in devices that carry out MRIs and CT scans for early detection and accurate diagnosis.

- The emergence of AI-powered medical robots and wearable medical sensors drives demand for 0 805 MLCCs. These components power AI and robotic functionalities in medical devices, with surgical robots and rehabilitation robots leading the trend. The 1 206 MLCCs play a crucial role in AI-driven diagnostic tools and wearable medical sensors. As diseases like cancer and atrial fibrillation continue to become more prevalent, accurate and efficient diagnostics have become paramount.

- In the process of addressing specific medical implant needs, 1 210 MLCCs align with the diverse landscape of medical implants driven by demographic shifts and aesthetic procedures. With the aging population and an increase in aesthetic surgeries, the demand for specialized medical implants is growing. The other case sizes segment addresses distinct device designs and spatial constraints, adapting to evolving medical technology.

Medical device innovations are fueling the growth of MLCCs across continents

- Asia-Pacific emerged as a dynamic hub for the medical device industry, driven by substantial opportunities in healthcare markets. With a remarkable 60% share of the global heart disease burden, India aims to collaborate with Japan by investing USD 42 billion to establish medical equipment manufacturing capabilities. This partnership aligns with the utilization of MLCCs in producing advanced devices like patient monitors and cardiac catheters.

- North America's healthcare landscape is marked by a high burden of chronic diseases like heart disease and stroke. MLCCs offer the capacity to create compact and reliable medical devices that cater to these challenges. With millions of Americans living with chronic diseases, the demand for medical solutions that integrate MLCCs has increased, emphasizing their crucial role in enhancing patient outcomes.

- The European healthcare market, the largest in the region, is driven by the aging population and increasing chronic diseases. Wearable health devices equipped with MLCCs aid in managing conditions like diabetes and cardiovascular disorders. The demand for miniaturized components aligns with MLCCs' capabilities, facilitating their integration into wearable devices for power management and wireless connectivity.

- The Rest of the World (RoW) encompassing the Middle East & Africa (MEA) presents opportunities and challenges. The MEA region shows substantial potential for medical devices and pharmaceuticals. The Middle East's healthcare sector is projected to reach a revenue of AED 408 billion by 2026, driven by investments in medical technology and pharmaceuticals. The demand for advanced medical devices, including those incorporating MLCCs, is surging, aligning with the region's healthcare expansion and focus on technology.

Global Medical Devices MLCC Market Trends

The increasing popularity of the Internet of Medical Things and technological advancements in devices are propelling healthcare spending

- The healthcare industry is experiencing significant technological advancements, including the growing adoption of innovative and wearable devices, making it a promising market for MLCCs. The increasing popularity of the Internet of Medical Things (IoMT), which involves interconnected devices used in medical and healthcare applications, will create numerous opportunities for MLCCs over the coming years. [1]

- During the COVID-19 pandemic, there was a substantial surge in global healthcare expenditure, which reached USD 9 trillion, equivalent to 10.8% of the global GDP, in 2020. Notably, the distribution of this expenditure varied significantly among different income groups. Government expenditure was the primary catalyst behind the overall rise in health spending in 2020. In all income groups, per capita government spending on health witnessed an upswing, surpassing the growth rate observed in previous years. [2]

- To boost healthcare readiness for impending pandemics or health catastrophes, increased investments are being made in research, emergency response capabilities, and healthcare infrastructure. Governments and healthcare organizations recognize the necessity for proactive measures like research, emergency response training, and infrastructure enhancements to manage and lessen the effects of possible health crises. Ensuring prompt and efficient emergency responses has increased the demand for healthcare expenditure in these areas.

Strategic adaptions in the wearables technology market augmenting the demand for medical devices MLCCs

- In 2020, the global market for hearables, watches, wristbands, and other wearables experienced a remarkable surge, with shipments reaching USD 444.7 million, representing a substantial growth rate of 28.38% compared to the previous year. However, the momentum slightly slowed down in 2021, as the growth rate moderated to 19.99% compared to the preceding year. Consequently, in 2022, the industry witnessed a decline of 7.7%, mainly driven by challenging macroeconomic conditions and the difficulty in achieving comparable results to the exceptional performance observed in 2021.

- This decline can be partially attributed to market saturation, wherein the wearable device sector had witnessed substantial expansion in the prior years, leading to diminished demand as a significant number of potential customers had already adopted such devices. To stimulate demand and regain momentum, vendors are adopting strategic measures, such as offering lower-cost alternatives, introducing attractive trade-in offers, providing financing options, and implementing subscription services. Furthermore, companies that diversify their product portfolio by incorporating devices with varying feature sets and price points, while building a robust ecosystem around them, stand to reap rewards once the market regains its growth trajectory.

Medical Devices MLCC Industry Overview

The Medical Devices MLCC Market is moderately consolidated, with the top five companies occupying 57.03%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Healthcare Expenditure

- 4.1.1 Global Health Care Expenditure

- 4.2 Medical Devices Adoption Rate

- 4.2.1 Global Medical Devices Adoption Rate

- 4.3 Wearables Sales

- 4.3.1 Global Medical Wearables Sales

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Case Size

- 5.1.1 0 402

- 5.1.2 0 603

- 5.1.3 0 805

- 5.1.4 1 206

- 5.1.5 1 210

- 5.1.6 Others

- 5.2 Voltage

- 5.2.1 100V to 500V

- 5.2.2 Above 500V

- 5.2.3 Less than 100V

- 5.3 Capacitance

- 5.3.1 10 μF to 100 μF

- 5.3.2 Less than 10 μF

- 5.3.3 More than 100 μF

- 5.4 Dielectric Type

- 5.4.1 Class 1

- 5.4.2 Class 2

- 5.5 Region

- 5.5.1 Asia-Pacific

- 5.5.2 Europe

- 5.5.3 North America

- 5.5.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms