|

市場調査レポート

商品コード

1684002

南米の除草剤:市場シェア分析、産業動向、成長予測(2025年~2030年)South America Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の除草剤:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 187 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

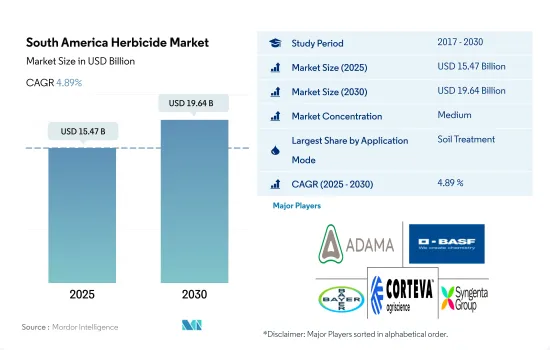

南米の除草剤市場規模は2025年に154億7,000万米ドルと推定・予測され、2030年には196億4,000万米ドルに達し、予測期間(2025年~2030年)のCAGRは4.89%で成長すると予測されます。

農産物に対する需要の高まりと雑草を効果的に管理することへの注目が市場の成長を強化しています。

- 化学灌漑は2022年の市場金額の19.7%を占める。灌漑インフラが整備された地域で普及しています。点滴灌漑システムの採用が増加していることが、今後数年間の市場成長を促進すると予想されます。

- 葉面散布剤は第2位のシェアを占め、予測期間(2023年~2029年)のCAGRは5.1%と予想されます。除草剤は植物の葉に直接散布され、そこで吸収されて植物全体に移行し、不要な植生を抑制します。農業では一般的な方法で、除草剤の使用量を最小限に抑えながら、的を絞った効率的な雑草防除が可能になります。

- 燻蒸法は、2023年から2029年の間に7,830万米ドルの成長が見込まれています。この方法では、土壌や温室のような閉鎖空間内の害虫や雑草を駆除するために、ガス状の除草剤を使用します。この方法は一般的に広い面積を処理するために使用され、特に土壌を媒介する害虫に対して効果的です。

- 土壌処理分野は、予測期間中(2023年~2029年)にCAGR 5.4%を記録すると予想されています。この方法は、土壌に除草剤を直接散布して、植え付け前の雑草を防除したり、しつこい雑草問題を管理したりするものです。土壌治療は、作物の定着と生育に有利な環境を作り出すのに役立ちます。

- 南米の除草剤市場は、予測期間中(2023年~2029年)に50億4,000万米ドルの成長が見込まれます。南米における除草剤の需要は、雑草の生育を効果的に抑制し、作物の収量を最大化するために、こうした散布方法を採用していることが影響しています。農法、作物のタイプ、雑草の圧力、害虫管理戦略の変化が除草剤製品の需要を押し上げています。

雑草防除の利点と収量への影響に関する意識の高まりが成長を牽引

- 南米は2022年の除草剤世界市場全体の35.5%を占める。南米の除草剤市場は、アルゼンチン、ブラジル、チリ、その他南米など様々な地域で成長を遂げています。これらの国々は、広大な農地を有する主要な農業生産国であるため、雑草の個体数を管理し、最適な作物収量を確保するために除草剤の使用が極めて重要になります。

- ブラジルは市場で53.6%のシェアを占め、期間中のCAGRは5.2%と予想されます。同国の農家は、雑草防除の利点と雑草が作物収量に与える影響に対する認識を深めています。雑草による作物損失の増加は、除草剤の採用率上昇につながる可能性があります。

- 2022年には、アルゼンチンが南米の除草剤市場で35.1%のシェアを占め、CAGRは5.6%と他国に比べて最速でした。食料と農産物の需要増加に伴い、アルゼンチンの農家は耕作面積を拡大し、作物生産を強化する可能性があり、雑草を防除する除草剤の必要性が高まる。

- 特定の除草剤に対する雑草耐性は、農家にとって大きな課題となりうる。その結果、農家はより新しい除草剤の製剤や作用機序に切り替える可能性があり、こうした代替剤への需要が高まる。こうした要因から、除草剤の消費量は期間中に19万1,900トン増加すると予想されます。

- 南米の除草剤市場は、予測期間中(2023年~2029年)にCAGR 5.2%を記録すると予測されます。農作物損失の増加、農作物を保護する必要性、雑草防除に対する意識の高まりが、農業製品に対する需要の高まりと相まって、市場の成長を促進しています。

南米の除草剤市場動向

雑草がはびこるのに適した土壌条件のため、アルゼンチンが除草剤消費で南米を独占

- 雑草は、土地や水資源の利用を妨げ、作物の収量に悪影響を及ぼす不要で望ましくない植物です。雑草による作物の収量損失は、雑草の発生時期、雑草の種類、作物の種類など、いくつかの要因に左右されます。雑草は、管理せずに放置すると、100%の収量損失をもたらす可能性があります。除草剤は、望ましくない雑草を操作または制御するために使用される化学物質です。除草剤は、雑草を防除するための効果的で操作性の高いツールであり、機械的な方法よりも少ないエネルギーで効率的に収量を達成することができます。

- 2022年の除草剤消費量は、アルゼンチンが7.4kg/haで南米を独占しました。アルゼンチンの土壌は多様で、パンパ地方の肥沃な土壌から乾燥地帯の砂質やローム質の土壌まです。さまざまな雑草種が特定の土壌条件に適応しているため、国内のさまざまな地域で繁茂し、広がっています。ノビエ、ブタクサ、ジョングラス、フィンガーグラス、グースグラス、バーニヤードグラス、ライグラスが最も重要な雑草とされています。

- ブラジルの2022年の除草剤消費量は5.3kg/haで、2番目に多いです。ブラジルは主に熱帯気候で、ほとんどの地域で年間を通じて気温が高いです。高温は多くの雑草種の発芽、成長、繁殖を促進するため、雑草の生育にとって好条件となります。Commelina benghalensis、Conyza spp.、Cyperus spp.、Bidens pilosa、Sorghum halepenseなどがブラジルで見られる主な雑草です。

- 南米には、特にブラジルやアルゼンチンなど広大な耕作地があり、除草剤の需要を牽引しています。大規模な作物を栽培するための開墾は、効果的な雑草防除の必要性を助長し、除草剤の需要を増大させています。

様々な除草剤の防除効果と他国からの輸入への依存が、この地域におけるアトラジン除草剤の価格を引き上げる可能性があります。

- アトラジンはトリアジン系に属する除草剤で、さまざまな作物の広葉雑草やイネ科雑草の防除に広く使用されています。南米におけるアトラジンの価格は、2022年には1万3,810米ドルでした。アトラジンの除草剤としての作用機序は、植物の光合成プロセスを阻害することです。特に葉緑体の光化学系II(PSII)タンパク質複合体を標的とし、光合成中に光エネルギーを化学エネルギーに変換する植物の能力を阻害します。その結果、有毒な製品別が蓄積され、最終的には対象となる雑草が枯死します。

- パラコートは、ビピリジリウム化合物という化学的分類に属する除草剤として広く使用されています。主に農業および非農業環境において、さまざまな広葉雑草およびイネ科雑草を防除します。パラコートは、その速効性と非選択性から、作物が出穂する前に雑草を防除するプレプラントまたはプレイマージェンス除草剤として使用されるのが一般的です。綿花、トウモロコシ、大豆、サトウキビ、その他さまざまな作物など、幅広い作物に有効です。パラコートは、2022年の南米での価格が4,600米ドルでした。

- グリホサートは広く使用されている除草剤で、有機ホスホン酸類に属します。非選択性浸透性除草剤であるため、さまざまな作物の幅広い雑草を効果的に防除できます。南米におけるグリホサートの価格は、2022年には1,100米ドルでした。グリホサートの有効性、広範な活性、比較的安価な価格により、この地域の農家は雑草防除にグリホサートを選択することが多いです。しかし、その使用は、潜在的な健康や環境への影響に対する懸念から議論の的となっています。

南米除草剤産業の概要

南米除草剤市場は適度に統合されており、上位5社で48.24%を占めています。この市場の主要企業は以下の通りです。 ADAMA Agricultural Solutions Ltd, BASF SE, Bayer AG, Corteva Agriscience and Syngenta Group.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- アルゼンチン

- ブラジル

- チリ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 化学灌漑

- 葉面散布

- 燻蒸

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- アルゼンチン

- ブラジル

- チリ

- その他の南米

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- American Vanguard Corporation

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Rainbow Agro

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001704

The South America Herbicide Market size is estimated at 15.47 billion USD in 2025, and is expected to reach 19.64 billion USD by 2030, growing at a CAGR of 4.89% during the forecast period (2025-2030).

The rising demand for agricultural products and a focus on managing weed effectively are strengthening the market's growth

- Chemigation accounted for 19.7% of market value in 2022. It is a popular choice in areas with well-developed irrigation infrastructure. The rising adoption of drip irrigation systems is expected to fuel the market's growth in the coming years.

- Foliar holds the second major share and is expected to record a CAGR of 5.1% during the forecast period (2023-2029). Herbicides are applied directly to the leaves of plants, where they are absorbed and translocated throughout the plant to control unwanted vegetation. It is common practice in agriculture, allowing for targeted and efficient weed control while minimizing herbicide usage.

- The fumigation method is anticipated to witness a growth of USD 78.3 million between 2023 and 2029. This method involves using gaseous herbicides to control pests and weeds in soil or enclosed spaces, such as greenhouses. It is commonly used to treat large areas and is especially effective against soil-borne pests.

- The soil treatment segment is expected to record a CAGR of 5.4% during the forecast period (2023-2029). This method involves applying herbicide directly to the soil to control weeds before planting or managing persistent weed issues. Soil treatment can help create a favorable environment for crop establishment and growth.

- The South American herbicide market is expected to grow by a value of USD 5.04 billion during the forecast period (2023-2029). The demand for herbicides in South America is influenced by the adoption of these application methods to control weed growth effectively and maximize crop yield. Changing agricultural practices, crop types, weed pressure, and pest management strategies are driving the demand for herbicide products.

The growth was driven by rising awareness about the benefits of weed control and its impact on yield

- South America accounted for 35.5% of the total global herbicide market in 2022. The herbicide market in South America is experiencing growth in various regions, including Argentina, Brazil, Chile, and the Rest of South America. These countries are major agricultural producers with vast expanses of farmland; therefore, the use of herbicides becomes crucial to manage weed populations and ensure optimal crop yields.

- Brazil held a major share of 53.6% in the market and is expected to register a CAGR of 5.2% during the period. Farmers in the country are becoming increasingly aware of the benefits of weed control and the impact of weeds on crop yields. Rising crop losses due to weeds may lead to higher adoption of herbicides.

- In 2022, Argentina held a 35.1% share of the South American herbicide market, registering a CAGR of 5.6%, which was the fastest compared to other countries. With the rising demand for food and agricultural products, farmers in Argentina may expand their cultivation areas and intensify crop production, leading to a greater need for herbicides to control weeds.

- Weed resistance to certain herbicides can be a significant challenge for farmers. As a result, they may switch to newer herbicide formulations or modes of action, driving demand for these alternatives. Due to these factors, the consumption of herbicide is expected to increase by 191.9 thousand metric ton during the period.

- The South American herbicide market is projected to record a CAGR of 5.2% during the forecast period (2023-2029). The rising crop losses, the need to protect crops, and increasing awareness of weed control, coupled with rising demand for agriculture products, are driving the growth of the market.

South America Herbicide Market Trends

Argentina dominated South America in the consumption of herbicides due to the favorable soil conditions for weed infestation

- Weeds are unwanted and undesirable plants that interfere with the utilization of land and water resources and thus adversely affect crop yields. Yield losses in crops due to weeds depend on several factors, such as weed emergence time, type of weeds, and crop type. Weeds can result in 100% yield loss if left uncontrolled. Herbicides are chemicals used to manipulate or control undesirable weeds. Herbicides are effective and operative tools to control weeds, allowing yields to be achieved efficiently with less energy than mechanical practices.

- Argentina dominated South America in consumption of herbicides at a rate of 7.4 kg/ha in 2022. Argentina has diverse soil types, ranging from fertile soils in the Pampas region to sandy and loamy soils in the arid areas. Different weed species are adapted to specific soil conditions, allowing them to thrive and spread in different areas of the country. Fleabane, pigweed, johnsongrass, fingergrass, goosegrass, barnyard grass, and ryegrass are considered the most important weeds.

- Brazil has the second-highest herbicide consumption rate of 5.3 kg/ha in 2022. Brazil has a predominantly tropical climate, with warm temperatures throughout the year in most regions. High temperatures provide favorable conditions for weed growth, as they accelerate the germination, growth, and reproduction of many weed species. Commelina benghalensis, Conyza spp., Cyperus spp., Bidens pilosa, and Sorghum halepense are some of the major weed species found in Brazil.

- South America has vast areas of arable land, particularly in countries like Brazil and Argentina, which drives the demand for herbicides. The clearing of land for cultivating large-scale crops contributes to the need for effective weed control, thereby increasing the demand for herbicides.

effectiveness in controlling various herbicides and dependency on imports from other countries may raise the price of Atrazine herbicides in the region.

- Atrazine is a herbicide belonging to the chemical class of triazines and is widely used to control broadleaf and grassy weeds in various crops. The price of atrazine in South America was USD 13.81 thousand in 2022. Atrazine's mode of action as a herbicide involves inhibiting the photosynthesis process in plants. It specifically targets the photosystem II (PSII) protein complex in chloroplasts, disrupting the plants' ability to convert light energy into chemical energy during photosynthesis. This leads to the accumulation of toxic byproducts and, ultimately, the death of the targeted weeds.

- Paraquat is a widely used herbicide belonging to the chemical class of bipyridylium compounds. It primarily controls various broadleaf and grassy weeds in agricultural and non-agricultural settings. Due to its rapid action and non-selective nature, paraquat is commonly used as a pre-plant or pre-emergence herbicide to control weeds before crops emerge. It is effective in a wide range of crops, including cotton, corn, soybeans, sugarcane, and various other crops. Paraquat was priced at USD 4.6 thousand in South America in 2022.

- Glyphosate is a widely used herbicide belonging to the chemical class of organophosphonates. It is a non-selective systemic herbicide, meaning it can effectively control a broad range of weeds in various crops. The price of glyphosate in South America was USD 1.1 thousand in 2022. Glyphosate's effectiveness, broad-spectrum activity, and relatively low cost have made it a popular choice for weed control for farmers in the region. However, its use has been controversial due to concerns about potential health and environmental impacts.

South America Herbicide Industry Overview

The South America Herbicide Market is moderately consolidated, with the top five companies occupying 48.24%. The major players in this market are ADAMA Agricultural Solutions Ltd, BASF SE, Bayer AG, Corteva Agriscience and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Chile

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 FMC Corporation

- 6.4.7 Rainbow Agro

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms