|

市場調査レポート

商品コード

1683999

南米の殺菌剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)South America Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の殺菌剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 189 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

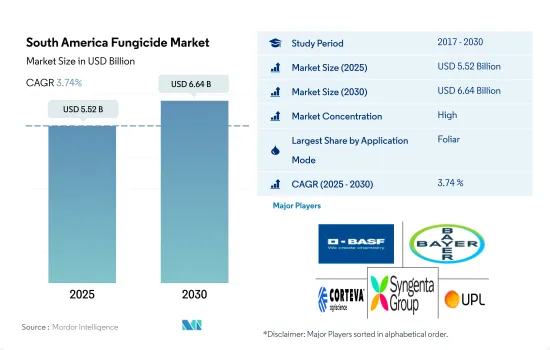

南米の殺菌剤市場規模は2025年に55億2,000万米ドルと推定・予測され、2030年には66億4,000万米ドルに達し、予測期間中(2025年~2030年)のCAGRは3.74%で成長すると予測されています。

葉面散布は殺菌剤の主要な散布方法として最も重要です。

- 南米では、農業における真菌性病害を効果的に防除するために、数多くの殺菌剤散布方法が利用されています。適切な散布方法を選択することで、農家はコスト効率の高い解決策を得ることができ、特定のエリアを正確にカバーし、不必要な使用を最小限に抑えることができます。この有効性の向上により、殺菌剤の利用が最適化され、農家の投入コストが削減されます。

- 農業における様々な殺菌剤散布方法の中で、葉面散布が主流であり、2022年の殺菌剤使用量全体の59.8%を占める。この方法は主に豆類と油糧種子で利用されており、42.1%と最大の市場シェアを占めています。葉面散布の標的を絞った効率的な吸収特性は、病害の防除効果に寄与し、農家の収量増加とコスト削減につながる可能性があります。

- 2022年には、種子治療法が全体の14.2%を占め、第2位の市場シェアを占めています。苗を保護し生産性を向上させる殺菌剤種子処理製品を使用するメリットに対する農家の意識の高まりにより、その採用が大幅に増加しました。その結果、南米の殺菌剤種子処理市場は、2023年から2029年の予測期間中にCAGRが4.0%になると予測されています。

- 南米の農業分野では、殺菌剤は作物の収量を最大化し、全体的な収益性を向上させることを主な目的として利用されています。用途別セグメントは大幅な成長が見込まれ、2023年~2029年の予測期間中のCAGRは4.0%です。

作物に対する真菌病害の脅威がますます大きくなり、ブラジルが市場を独占

- 南米の熱帯気候では多くの作物が生育します。ブラジル、アルゼンチン、パラグアイは南米の3大農業生産国です。これらの国々は、大豆、トウモロコシ、砂糖、コーヒー、果物、野菜の主要輸出国です。

- ブラジルが市場を独占し、2022年の市場シェアは59.4%を占めました。ブラジルの農業が拡大し多様化するにつれ、作物に対する真菌病害の脅威はますます大きくなっています。真菌病原菌は様々な作物に悪影響を及ぼし、収穫量の減少、品質の低下、農家の経済的損失につながります。

- チリは2022年に南米の殺菌剤市場の4.8%を占めました。チリは、北部のアタカマ砂漠は温帯気候、中央部の肥沃な中央渓谷地域は地中海性気候、南部の低い海岸山脈と東部の険しいアンデス山脈は冷涼で湿潤な気候です。これらの気候条件は、この国で真菌病が蔓延するのに好都合です。Captanとthiramはチリで広く使われている殺菌剤です。Captanは有機物含有量の多い自然土壌との相互作用が最も大きく、一方thiramは粘土含有量の多い土壌を好むことが分かっています。

- 殺菌剤市場を牽引する要因としては、耕地面積の減少、人口の増加、作物収量向上の必要性などが挙げられます。既存の殺菌剤に対する様々な真菌の耐性や、植物における新たな病害の出現により、主要企業は新たな真菌の突然変異と戦い、農家の損失を減らすための新規製品を見つけることになりました。作物の病気と戦うための殺菌剤の需要の増加は、予測期間中に市場を牽引すると予想されます。

南米の殺菌剤市場動向

栽植密度の増加などの農業慣行の激化は、真菌病原体の急速な増殖を助長する環境を作り出します。

- 真菌感染症は植物の全体的な健康状態を弱め、生育不良を引き起こします。感染した植物は、草丈が低下し、葉が小さくなり、枝が少なくなることがあり、これは収穫量の低下に直結します。真菌はまた、植物内のホルモンバランスを乱し、その開発と全体的な生産性に影響を与える可能性があります。

- 南米のサザン・コーンは、病害の流行にとって最も重要な地域のひとつです。この地域はアルゼンチン、ボリビア、チリ、ブラジル、パラグアイ、ウルグアイで構成されています。深刻な病害は、さび病、うどんこ病、真菌性葉枯病(セプトリア葉枯病、斑点病)などです。これらの病害は、通常の条件が病害の発生と蔓延に適しているため、毎年発生しています。

- チリは南米最大の殺菌剤消費国で、2022年の消費量は4.1kg/haです。これは、チリの特定の地域が、高湿度、降雨量、気温の変動といった気候条件にあり、真菌病害の開発を助長する環境を作り出しているためです。こうした病害を予防・管理するため、農家はしばしば殺菌剤に頼ることになります。

- ブラジル南部の気候条件は、いくつかの重要な真菌性葉面病害の開発に非常に適しています。12年間の調査で、殺菌剤を散布した小麦の平均収量は40%増加しました。2022年の殺菌剤消費量は、ブラジルが0.9kg/haで第2位でした。

- 栽植密度の増加などの農業慣行の激化は、真菌病原体の急速な増殖と定着を助長する環境を作り出し、予測期間中の殺菌剤需要を促進しています。

マンコゼブは南米で最も広く使用されている殺菌剤です。

- Mancozebはジチオカルバメート系の殺菌剤です。南米ではさまざまな作物の菌類病害を防除するために一般的に使用されています。マンコゼブは、ジャガイモ、トマト、ブドウ、バナナなどの作物で、晩枯病、べと病、初期疫病、炭疽病など、幅広い真菌性病害の管理に有効です。Mancozebは真菌の代謝プロセスを阻害し、その成長と繁殖を妨げることで効果を発揮します。また、Mancozebは他の殺菌剤に比べて活性スペクトルが広く、真菌細胞内の複数の部位に作用するため、より効果的です。2022年の南米におけるMancozebの価格は7,800米ドルでした。

- プロピネブもマンコゼブと同様、ジチオカルバメート系に属する殺菌剤です。プロピネブは、農業における様々な真菌病害の防除に使用されます。プロピネブは、さまざまな作物のべと病、晩枯病、葉斑病、疫病などの真菌病害の管理に有効です。マンコゼブと同様、プロピネブもまたマルチサイト活性によって作用するため、真菌集団における耐性菌の発生が少ないです。プロピネブの2022年の南米での価格は3,540米ドルです。

- MancozebやPropinebと同様、Ziramもジチオカルバミン酸塩の化学クラスに属し、2022年の価格は1メートルあたり3,300米ドルでした。ジラムは農業における真菌性病害の防除に一般的に使用され、紋枯病、べと病、葉斑病、炭疽病などの真菌性病害を効果的に管理することが知られています。ジラムは真菌細胞内のいくつかの主要な酵素を阻害し、さまざまな代謝プロセスを阻害し、病原菌の増殖・繁殖能力を妨げます。複数の部位に作用するため、長期にわたる病害防除に効果的です。

南米殺菌剤産業の概要

南米殺菌剤市場はかなり統合されており、上位5社で70.48%を占めています。この市場の主な企業は次のとおりです。 BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- アルゼンチン

- ブラジル

- チリ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 化学灌漑

- 葉面散布

- 燻蒸

- 種子治療

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- アルゼンチン

- ブラジル

- チリ

- その他南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd.

- American Vanguard Corporation

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Rainbow Agro

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001701

The South America Fungicide Market size is estimated at 5.52 billion USD in 2025, and is expected to reach 6.64 billion USD by 2030, growing at a CAGR of 3.74% during the forecast period (2025-2030).

The foliar application holds the utmost significance as the primary mode of fungicide application

- In South America, numerous methods of fungicide applications are utilized to effectively control fungal diseases in agriculture. By choosing suitable application methods, farmers can attain cost-efficient solutions, ensuring accurate coverage of specific areas and minimizing unnecessary usage. This improved efficacy optimizes fungicide utilization, resulting in decreased input costs for farmers.

- Among various fungicide application methods in agriculture, foliar application is the dominant mode, accounting for 59.8% of the total fungicide usage in 2022. This approach is primarily utilized in pulses and oilseeds, which hold the largest market share at 42.1%. The targeted and efficient absorption properties of foliar application contribute to its effectiveness in controlling diseases, potentially resulting in increased yields and saving costs for farmers.

- In 2022, the seed treatment method held the second-largest market share, comprising 14.2% of the total. The rise in farmers' awareness about the benefits of using fungicide seed treatment products to protect seedlings and boost productivity has resulted in a significant rise in their adoption. As a result, it is projected that the South American fungicide seed treatment market may experience a CAGR of 4.0% during the forecast period from 2023 to 2029.

- In the agricultural sector of South America, fungicides are utilized with the primary aim of maximizing crop yields and improving overall profitability. The mode of the application segment is anticipated to experience substantial growth, with a CAGR of 4.0% during the forecast period from 2023 to 2029.

Brazil dominated the market as the threat of fungal diseases to crops became increasingly significant

- Many crops thrive in the tropical climates of South America. Brazil, Argentina, and Paraguay are the three major agricultural producers in South America. These countries are major exporters of soybeans, maize, sugar, coffee, fruits, and vegetables.

- Brazil dominated the market, accounting for a market share of 59.4% in 2022. As Brazil's agriculture expands and diversifies, the threat of fungal diseases to crops becomes increasingly significant. Fungal pathogens can adversely impact a wide range of crops, leading to yield losses, reduced quality, and economic losses for farmers.

- Chile accounted for 4.8% of the South American fungicide market in 2022. Chile has a temperate climate in the Atacama Desert in the north, a Mediterranean climate in the central and fertile central valley region, and a cool and damp climate in the southern low coastal mountains and rugged Andes in the east. These climatic conditions favor the proliferation of fungal diseases in the country. Captan and thiram are two fungicides widely used in Chile. Captan is found to have the greatest interaction with natural soils with high organic matter content, while thiram showed a preference for soils with high clay content.

- Factors driving the market for fungicides include decreasing arable land, increasing population, and the need to improve crop yields. Resistance of various fungi to the existing fungicides and the emergence of new diseases in plants led the companies to find novel products for fighting the new fungus mutations and reducing the loss to farmers. The increasing demand for fungicides to fight crop diseases is expected to drive the market during the forecast period.

South America Fungicide Market Trends

Intensification of agricultural practices, such as increased planting densities, creates a conducive environment for the rapid proliferation of fungal pathogens

- Fungal infections can weaken the overall health of plants, leading to stunted growth. Infected plants may exhibit reduced height, smaller leaves, and fewer branches, which can directly translate into lower crop yields. Fungi can also disrupt the hormonal balance within plants, affecting their development and overall productivity.

- The Southern Cone of South America is one of the most critical regions for disease epidemics. The region is comprised of Argentina, Bolivia, Chile, Brazil, Paraguay, and Uruguay. Serious diseases that cause epidemics and production losses include leaf rusts, powdery mildew, and fungal leaf blights (Septoria leaf blotch, spot blotch). These diseases are present every year since normal conditions are conducive to their appearance and dissemination.

- Chile is the largest consumer of fungicides in South America, with a consumption of 4.1 kg/ha in the year 2022. This is because certain regions in Chile have climatic conditions, such as high humidity, rainfall, and temperature fluctuations, which can create a conducive environment for fungal disease development. To prevent and manage these diseases, farmers often rely on fungicides as a proactive measure.

- Climatic conditions prevailing in southern Brazil are highly conducive to the development of several important fungal foliar diseases. A twelve-year study demonstrated that wheat plants sprayed with fungicide showed a mean yield increase of 40%. Brazil accounted for the second most fungicide consumption rate of 0.9 kg/ha in 2022.

- The intensification of agricultural practices, such as increased planting densities, creates a conducive environment for the rapid proliferation and establishment of fungal pathogens, thereby fueling the demand for fungicides during the forecast period.

Mancozeb is the most popularly used fungicide in South America

- Mancozeb is a fungicide belonging to the chemical class of dithiocarbamates. It is commonly used in South America to control fungal diseases in various crops. Mancozeb is effective in managing a wide range of fungal diseases, including late blight, downy mildew, early blight, and anthracnose, in crops like potatoes, tomatoes, grapes, and bananas. Mancozeb works by interfering with the metabolic processes of the fungi, preventing their growth and reproduction. In addition, Mancozeb has a broad spectrum of activity compared to other fungicides and acts on multiple sites within the fungal cell, making it more effective. Mancozeb was priced at USD 7.8 thousand in South America in 2022.

- Propineb is also a fungicide belonging to the chemical class of dithiocarbamates, similar to Mancozeb. It is used to control various fungal diseases in agriculture. Propineb is effective in managing fungal diseases such as downy mildew, late blight, leaf spot, and blight in various crops. Like Mancozeb, Propineb also works through multi-site activity, making it less prone to resistance development in fungal populations. Propineb was priced at USD 3.54 thousand in South America in the year 2022.

- Similar to Mancozeb and Propineb, Ziram belongs to the chemical class of dithiocarbamates, priced at USD 3.3 thousand per metric in 2022. It is commonly used to control fungal diseases in agriculture and is known to effectively manage fungal diseases such as common blight, downy mildew, leaf spot, and anthracnose. Ziram inhibits several key enzymes in the fungal cell, disrupting various metabolic processes and interfering with the pathogens' ability to grow and reproduce. The multi-site activity makes it an effective tool for disease control over the long term.

South America Fungicide Industry Overview

The South America Fungicide Market is fairly consolidated, with the top five companies occupying 70.48%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Chile

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 FMC Corporation

- 6.4.7 Rainbow Agro

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms