|

市場調査レポート

商品コード

1683996

北米の殺菌剤:市場シェア分析、産業動向、成長予測(2025年~2030年)North America Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の殺菌剤:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 191 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

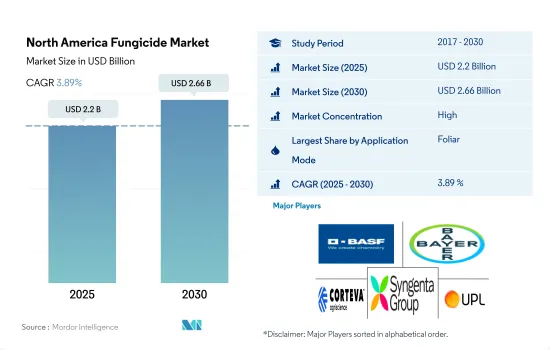

北米の殺菌剤市場規模は2025年に22億米ドルと推定・予測され、2030年には26億6,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは3.89%で成長します。

葉面散布は殺菌剤の主要な散布方法として最も重要です。

- 北米では、農業における真菌性病害を効果的に防除するために、数多くの殺菌剤散布技術が利用されています。適切な散布方法を選択することで、農家はコスト効率の高い解決策を得ることができ、特定のエリアを正確にカバーし、不必要な使用を最小限に抑えることができます。この有効性の向上により、殺菌剤の利用が最適化され、農家の投入コストが削減されます。

- 農業における様々な殺菌剤散布方法の中で、葉面散布が主流であり、2022年の殺菌剤使用量全体の60.8%を占める。この方法は主に穀物や穀類の栽培に利用されており、41.4%の最大市場シェアを占めています。葉面散布の標的を絞った効率的な吸収特性は、病害の防除効果に寄与し、農家の収量増加とコスト削減につながる可能性があります。

- 2022年には、種子治療法が全体の13.8%を占め、第2位の市場シェアを占めています。苗を保護し生産性を向上させる殺菌剤種子処理製品を使用する利点に関する農家の意識の高まりにより、その採用が大幅に増加しました。北米の殺菌剤市場の種子処理分野は、予測期間中にCAGRが4.0%になると予測されています。

- 北米の農業セクターでは、殺菌剤は作物の収量を最大化し、全体的な収益性を向上させることを主な目的として利用されています。散布方法は大幅な成長が見込まれ、予測期間中のCAGRは4.1%です。

米国は、真菌蔓延の増加と高品質の農産物に対する需要の高まりにより、市場で支配的な地位を占めています。

- 北米の殺菌剤市場は著しい拡大を見せており、同地域の様々な国が顕著な成長を遂げています。この殺菌剤需要の急増は、菌類病害を防除し、作物の損失を減らす必要性に起因します。2022年、北米は世界の殺菌剤市場において金額ベースで12.1%というかなりの市場シェアを占めていました。

- 米国は北米の殺菌剤市場を独占し、2022年には47.2%の市場シェアを占めました。米国は広大で多様な農業を営んでおり、国内のさまざまな地域でさまざまな作物が栽培されています。この多様性が作物の様々な真菌病に対する感受性を高め、殺菌剤の需要増につながっています。

- 2022年には、メキシコは殺菌剤の第2位の消費国となり、21.1%という大きな市場シェアを占めました。同国の農業慣行は集約農業を重視しており、高収量作物の大量栽培が特徴です。しかし、このような集約的なやり方は、真菌病が急速に蔓延する好都合な環境も作り出しています。フザリウム萎凋病、うどんこ病、べと病、炭そ病、さび病は穀物や穀類に大きな影響を与え、作物の被害や収量の減少につながります。その結果、作物を保護し生産性を維持するためには、殺菌剤の使用が不可欠となります。

- 農家の意識の高まり、農業技術の進歩、農業セクターの拡大など、さまざまな要因が北米の殺菌剤市場の成長を後押ししています。その結果、北米の殺菌剤市場は予測期間(2023年~2029年)を通してCAGR 4.1%を記録すると予測されています。

北米の殺菌剤市場動向

真菌病による経済的損失の増大が殺菌剤の必要性を高めている

- 真菌病は、植物にダメージを与え、その生産性を低下させることにより、作物に大きな損失をもたらす可能性があります。また、作物の品質に悪影響を与え、販売や消費に適さなくなることもあります。北米ではメキシコが最大の殺菌剤消費国で、2022年には1,400.0gの殺菌剤が消費されます。メキシコの気候は乾燥から熱帯まで様々で、農作物の真菌病の開発と蔓延に好条件を提供しています。

- 2016年から2019年にかけて、米国とカナダにおける真菌病によるトウモロコシの収量減少に起因する平均経済損失は、1ヘクタール当たり138.13米ドルと推定されました。病害による作物収量の減少によって引き起こされる大きな経済的損失は、農家が作物を保護し経済的影響を軽減しようとするため、化学殺菌剤の使用量を増加させる可能性があります。このため、病害の発生を管理・防除するための殺菌剤の需要が高まり、農業における化学薬品の投入量が増加する可能性があります。

- トウモロコシのタールスポット、綿花のオオタバコ病、大豆の突然死症候群といった病害は、2022年に北米で大きな損失をもたらし、農地1ヘクタール当たりの化学殺菌剤散布の必要量を増加させました。殺菌剤の反復的かつ広範な使用は、耐性株の開発にもつながり、革新的な化学分子の開発の必要性を高めています。

- 同地域の気候条件の変化による真菌病の発生率の増加、収量ロスの削減、1ヘクタール当たりの作物生産性の向上などの要因により、北米における化学殺菌剤の需要は今後数年間で拡大すると予想されます。

作物を病害から守るための殺菌剤需要の増加は、原料価格の上昇により殺菌剤の価格を押し上げる可能性があります。

- マンコゼブは幅広いスペクトラムを持つ接触殺菌剤で、米国では多くの果実、野菜、ナッツ、畑作物への適用が認められています。ジャガイモ疫病、葉斑病、かさぶた、さび病など、広範な菌類病害を防除します。ジャガイモ、トウモロコシ、ソルガム、トマト、穀物などの作物の種子治療の役割を果たします。2022年の市場価格は1トン当たり7,800米ドル。

- 接触殺菌剤に分類されるプロピネブは、2022年の市場価格がトン当たり3,500米ドルでした。プロピネブの利用は、かさぶた、早枯病、晩枯病、枯れ病、バッカイ腐敗病、べと病、果実斑点病、褐斑病、狭葉斑点病など様々な病害の防除に及び、リンゴ、ジャガイモ、チリ、トマトなどの作物に影響を与えます。

- ジラムは、ジメチルジチオカルバメート系殺菌剤に分類される殺菌剤で、石果、ポームフルーツ、ナッツ類、野菜、観賞用植物など、商業目的で栽培される幅広い作物に影響を及ぼす真菌病害を防除するために登録されています。リンゴやナシのかさぶた、モモの葉巻、炭そ病、トマトの初期疫病などに使用されます。その用途は、栽培中の作物を害から守り、収穫した果物の貯蔵や輸送中の品質を保つという2つの目的を果たします。2022年の価格は1トン当たり3,300米ドルでした。

- マンコゼブ、プロピネブ、ジラムが最も一般的に使用される殺菌剤成分です。2021年、米国は殺菌剤のほとんどをインド、ベルギー、ドイツから輸入しており、世界第3位の輸入国です。

北米の殺菌剤産業の概要

北米の殺菌剤市場はかなり統合されており、上位5社で74.80%を占めています。この市場の主要企業は以下の通りです。 BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 薬剤散布

- 葉面散布

- 燻蒸

- 種子治療

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd.

- American Vanguard Corporation

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001698

The North America Fungicide Market size is estimated at 2.2 billion USD in 2025, and is expected to reach 2.66 billion USD by 2030, growing at a CAGR of 3.89% during the forecast period (2025-2030).

Foliar application holds the utmost importance as the primary mode of fungicide application

- In North America, numerous techniques for fungicide application are utilized to effectively control fungal diseases in agriculture. By choosing suitable application methods, farmers can attain cost-efficient solutions, ensuring accurate coverage of specific areas and minimizing unnecessary usage. This improved efficacy optimizes fungicide utilization, resulting in decreased input costs for farmers.

- Among various fungicide application methods in agriculture, foliar application is the dominant mode, accounting for 60.8% of the total fungicide usage in 2022. This approach is primarily utilized in cultivating grains and cereals, which hold the largest market share of 41.4%. The targeted and efficient absorption properties of foliar application contribute to its effectiveness in controlling diseases, potentially resulting in increased yields and cost savings for farmers.

- In 2022, the seed treatment method held the second-largest market share, comprising 13.8% of the total. The rise in farmers' awareness about the benefits of using fungicide seed treatment products to protect seedlings and boost productivity resulted in a significant rise in their adoption. The seed treatment segment of the North American fungicide market is projected to experience a CAGR of 4.0% during the forecast period.

- In the North American agricultural sector, fungicides are utilized with the primary aim of maximizing crop yields and improving overall profitability. The mode of application is anticipated to experience substantial growth, with a CAGR of 4.1% during the forecast period.

The United States holds a dominant position in the market due to an increase in fungal infestations and a rising demand for high-quality agricultural produce

- The North American fungicide market is witnessing significant expansion, with various countries in the region experiencing notable growth. This surge in fungicide demand is attributed to the need to control fungal diseases and reduce crop losses. In 2022, North America held a considerable market share of 12.1%, by value, in the global fungicide market.

- The United States dominated the North American fungicide market, accounting for a market share of 47.2% in 2022. The United States has a vast and diverse agricultural landscape, with a wide range of crops grown in different parts of the country. This diversity increases the susceptibility of crops to various fungal diseases, leading to a higher demand for fungicides.

- In 2022, Mexico ranked as the second-largest consumer of fungicides, holding a substantial market share of 21.1%. The country's agricultural practices emphasize intensive farming, characterized by the cultivation of high-yield crops in large quantities. However, this intensive approach also creates a favorable environment for the rapid spread of fungal diseases. Fusarium wilt, powdery mildew, downy mildew, anthracnose, and rust diseases significantly impact grains and cereals, leading to crop damage and reduced yields. As a result, the use of fungicides becomes imperative to protect crops and maintain productivity.

- Various factors, including rising awareness among farmers, advancements in agricultural technologies, and the expansion of the agricultural sector, drive the growth of the fungicide market in North America. As a result, the North American fungicide market is projected to experience a CAGR of 4.1% throughout the forecast period (2023-2029).

North America Fungicide Market Trends

Increasing economic losses due to fungal diseases are increasing the need for fungicides

- Fungal diseases can cause substantial crop losses by damaging plants and reducing their productivity. They can negatively impact crop quality, making the crops unsuitable for sale or consumption. In North America, Mexico is the largest consumer of fungicides, with 1,400.0 g of fungicides consumed in 2022. Mexico's climate varies from arid to tropical, providing favorable conditions for the development and spread of fungal diseases in crops.

- Between 2016 and 2019, the average economic loss resulting from decreased corn yields due to fungal diseases in the United States and Canada was estimated at USD 138.13 per hectare. The significant economic losses caused by reduced crop yields from diseases can increase the usage of chemical fungicides as farmers seek to protect their crops and mitigate the financial impact. This can lead to a higher demand for fungicides to manage and control disease outbreaks, contributing to increased chemical inputs in agriculture.

- Diseases like tar spots in maize, bollworm rots in cotton, and sudden death syndrome in soybeans caused significant losses in North America in 2022, leading to higher requirements for chemical fungicide application per hectare of agricultural land. The repeated and extensive use of fungicides also resulted in the development of resistant strains, increasing the need for the development of innovative chemical molecules.

- Owing to factors like the increased incidence of fungal disease due to changing climatic conditions in the region, the need for reduced yield losses, and higher crop productivity per hectare, the demand for chemical fungicides in North America is anticipated to grow over the coming years.

The increasing demand for fungicides to protect the crops from disease may drive the prices of fungicides due to the increasing raw material prices

- Mancozeb is a broad-spectrum contact fungicide that is labeled for application on numerous fruits, vegetables, nuts, and field crops in the United States. It protects against a wide spectrum of fungal diseases, including potato blight, leaf spot, scab, and rust. It fulfills the role of seed treatment for crops like potatoes, corn, sorghum, tomatoes, and cereal grains. Its market price for 2022 achieved a value of USD 7.8 thousand per metric ton.

- Propineb, classified as a contact fungicide, accounted for a market price of USD 3.5 thousand per metric ton in 2022. Its utilization encompasses the control of various diseases such as scab, early and late blight, dieback, buckeye rot, downy mildew, and fruit spots, as well as brown and narrow-leaf spot diseases, impacting crops like apple, potato, chili, and tomato.

- Ziram, a fungicide categorized within the dimethyldithiocarbamate group, is registered to control fungal diseases that affect an extensive array of crops, including stone fruits, pome fruits, nuts, vegetables, and ornamental plants cultivated for commercial purposes. Its uses encompass addressing issues such as apple and pear scabs, peach leaf curls, anthracnose, and early blight in tomatoes. Its application serves the dual purpose of shielding crops from harm while growing and preserving the quality of the harvested fruits during storage or transport. The price for 2022 stood at USD 3.3 thousand per metric ton.

- Mancozeb, Propineb, and Ziram are the most commonly used fungicide ingredients. In 2021, the United States imported most of its fungicides from India, Belgium, and Germany, and it is the third-largest importer of fungicides worldwide.

North America Fungicide Industry Overview

The North America Fungicide Market is fairly consolidated, with the top five companies occupying 74.80%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 FMC Corporation

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms