|

市場調査レポート

商品コード

1911770

中東・アフリカの変圧器市場:シェア分析、業界動向、統計、成長予測(2026年~2031年)Middle East And Africa Transformer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカの変圧器市場:シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

概要

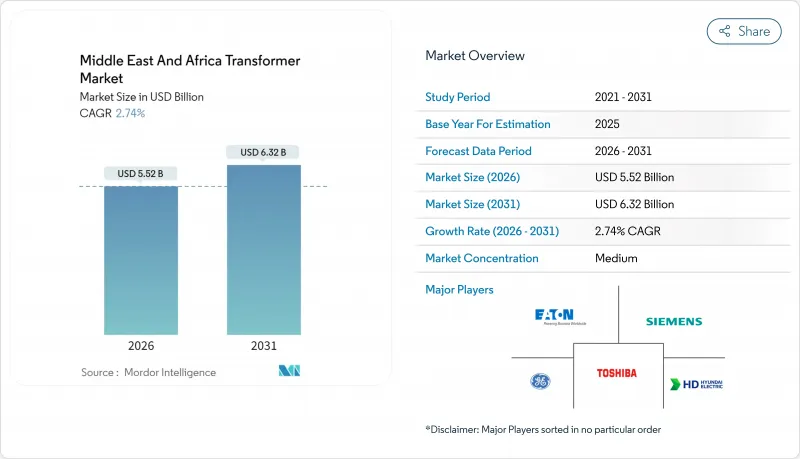

中東・アフリカの変圧器市場は、2025年に53億7,000万米ドルと評価され、2026年の55億2,000万米ドルから2031年までに63億2,000万米ドルに達すると予測されています。

予測期間(2026~2031年)におけるCAGRは2.74%と見込まれます。

この緩やかな成長の背景には、構造的な変化が潜んでいます。国家基金が送電網近代化の大規模プロジェクトへ資本を誘導する一方で、電力会社の予算は原油価格の変動に敏感な状態が続いています。サウジアラビアのNEOMプロジェクトのような大規模投資地域では、コンバータステーションや高圧直流送電(HVDC)リンクが従来型配電設備の増設に取って代わり、特殊な高電圧需要が急増しています。サプライチェーンの課題がこの動向をさらに加速させています。日立エナジーは、新規電力クラスのユニットには現在3年のリードタイムが必要であると警告しており、これにより電力会社は過剰発注を余儀なくされ、地域参入企業は生産の現地化を進めています。同時に、環境規制の強化とコンパクトな設備へのニーズを反映し、密集した都市部やハイパースケールデータセンターでは空冷設計が普及しつつあります。

中東・アフリカの変圧器市場の動向と洞察

大規模再生可能エネルギーが送電網拡大を牽引

各国のクリーンエネルギー目標が調達構造を根本的に変革しています。サウジアラビアは2030年までに再生可能エネルギー比率50%を目標としており、風力発電所ごとに複数の33/132kV昇圧変圧器を必要とする集電回路の設置が義務付けられています。エジプトのスエズ湾プロジェクトも大陸規模で同様の取り組みを進めており、モロッコの再生可能エネルギー52%目標は、屋根設置型太陽光発電に連動する配電ユニットの需要を押し上げています。間欠的な出力は電圧安定性に負荷をかけるため、電力会社は高調波フィルタリング機能を備えたパワーエレクトロニクス統合変圧器をますます指定しています。したがって、デジタル対応製品ラインを持つメーカーはプレミアム価格を設定できます。能動的な送電網管理への持続的な転換は、中東・アフリカの変圧器市場における高付加価値製品の構成を確固たるものにしています。

都市部の電力需要増加

都市の急速な成長が既存ネットワークに負荷をかけています。ドバイでは23億1,000万米ドルを投じた地下送電網更新計画において、高温環境対応のコンパクトユニットが優先されています。ラゴスやアブジャでも同様の容量不足が顕在化し、マイクログリッドの導入を促進しています。都市計画では騒音規制や漏洩防止対策が強化され、油入タンクよりも乾式コアが好まれます。NEOMはIoTセンサを初期段階から統合し、予測保全を自治体制御室に組み込むことで基準を確立。こうした都市中心の支出は出荷を地理的に集中させ、サプライヤーはサービス拠点の最適化が可能となる一方、地域的な物流混乱の影響を受けやすくなります。

原油価格連動による公益事業設備投資の削減

予算が原油収入に連動するため、入札は瞬時に凍結される可能性があります。ナイジェリアでは2024年にブレント原油価格がバレル当たり70米ドルを下回った際、複数の送電網プロジェクトが延期され、老朽化した設備群の寿命が最適な更新時期を超えて延長されました。サウジアラビアでも同様の低迷期に二次変電所の認可が抑制されましたが、旗艦プロジェクトは継続されました。変動の激しいサイクルは製造業者の在庫計画を複雑化し、地理的分散とリーン生産モデルを有する企業に有利に働きます。蓄積された更新需要があるにもかかわらず、年間発注量の変動が中東・アフリカの変圧器市場のキャッシュフローを歪めています。

セグメント分析

100MVAを超える大型変圧器は、再生可能エネルギーの長距離送電を目的とした400kV・500kV送電路への公益事業投資を反映し、4.62%という最速のCAGRが見込まれます。数量ベースでは出荷台数が少ないも、金額ベースでは中東・アフリカの変圧器市場規模に大きく貢献しました。中容量機器は2025年に64.35%のシェアを維持し、変電所拡大や産業施設建設の大半を支えています。電力会社の事前発注は複数年に及ぶリードタイム対策となり受注状況を良好に保ちますが、サプライヤーは資本集約性と厳格な検査設備要件に直面し、新規参入を制限されています。

需要構成は、モロッコースペイン間HVDCやGCC電力取引パイロット事業など、連系プロジェクトが活発な高電圧地域に偏っています。一方、小規模ユニットは農村電化や商用屋上太陽光発電を支え、着実ながらも緩やかな成長をもたらしています。これらの動向が相まって、中東・アフリカの変圧器市場のプレミアム化傾向を確固たるものとし、研究開発を高電圧絶縁システムやデジタルネイティブ制御インターフェースへと導いています。

2025年時点で油入変圧器は中東・アフリカの変圧器市場の83.95%を占めています。これは熱的余裕度が湾岸地域の気候に適しているためです。しかしながら、ハイパースケールデータセンターや防火設備を要する複合用途高層ビルの需要に牽引され、空冷設計は4.92%のCAGRで成長すると予測されています。地方自治体の条例で油槽や遮水堤が規制される地域では、採用がさらに加速しています。サプライヤーは、無負荷損失を最大30%削減する非晶質コア技術革新を推進しており、従来より高い初期費用を相殺しています。

乾式変圧器の設備投資額は依然として高額ですが、メンテナンス費用と保険料の削減によりライフサイクルコストの差は縮小しています。IEC 60076-11:2022が各国規格へ移行するにつれ、技術的な明確化により仕様の曖昧さが解消され、潜在需要が解放されます。その結果、冷却方式の選択は気候条件ではなく用途中心となり、中東・アフリカの変圧器産業の販売構成にサブセグメンテーションが加わります。

中東・アフリカの変圧器市場レポートは、定格出力(大型、中型、小型)、冷却方式(空冷式、油冷式)、相(単相、三相)、変圧器タイプ(電力用、配電用)、エンドユーザー(電力会社、産業、商業、住宅)、地域(サウジアラビア、アラブ首長国連邦、カタール、南アフリカ、エジプト、ナイジェリア、その他の中東・アフリカの諸国)ごとに分類されています。

その他の特典

- エクセル形態の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電力会社規模の再生可能エネルギーが送電網拡大を牽引

- 都市部における電力需要の増加

- 国費による送電網近代化プログラム

- 鉱業主導のマイクログリッド投資

- 海水淡水化プラントの電化

- 越境高電圧直流送電(HVDC)リンク

- 市場抑制要因

- 原油価格上昇に伴う電力会社の設備投資削減

- 低コストなアジアからの輸入品による価格圧力の高まり

- 熟練した保守作業員の不足

- 乾式変圧器向け樹脂供給のボトルネック

- サプライチェーン分析

- 規制情勢

- 技術の展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の激しさ

第5章 市場規模と成長予測

- 定格出力別

- 大型(100MVA超)

- 中型(10~100MVA)

- 小型(10MVA以下)

- 冷却方式別

- 空冷式

- 油冷式

- 相別

- 単相

- 三相

- 変圧器タイプ別

- 電力

- 配電

- エンドユーザー別

- 電力会社

- 産業用

- 商用

- 家庭用

- 地域別

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- エジプト

- ナイジェリア

- その他の中東・アフリカ

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、パートナーシップ、PPA)

- 市場シェア分析(主要企業の市場順位・シェア)

- 企業プロファイル

- Hitachi Energy Ltd.

- Siemens AG

- General Electric Co.

- Schneider Electric SE

- Eaton Corporation plc

- Mitsubishi Electric Corp.

- Toshiba Corp.

- HD Hyundai Electric Co., Ltd.

- Hyosung Heavy Industries

- Bharat Heavy Electricals Ltd.

- ABB Saudi Arabia

- Elsewedy Electric

- CG Power & Industrial

- Wilson Transformer(南アフリカ)

- Aktif Elektroteknik

- Voltamp Oman

- Arteche

- Alfanar

- Saudi Power Transformers Co.

- ZTR