|

市場調査レポート

商品コード

1683805

グリーン水素-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Green Hydrogen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| グリーン水素-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

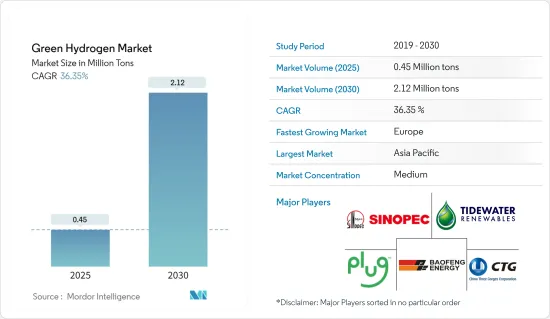

グリーン水素市場規模は、2025年には45万トンと推計され、予測期間中(2025年~2030年)のCAGRは36.35%で、2030年には212万トンに達すると予測されます。

COVID-19パンデミックは、生産の停止とサプライチェーンの混乱により、グリーン水素産業全体の成長に中程度の影響を与えました。しかし、パンデミック後、グリーン水素の需要は輸送分野で増加し、それが業界の成長を促進しました。

中期的には、化学産業におけるグリーン水素の需要と、炭素排出に関する環境問題の高まりが、グリーン水素の需要を牽引すると予想されます。

その反面、グリーン水素の投資コストが高いこと、技術やインフラへのアクセスが限られていること、エネルギー損失が大きいことなどが、業界全体の成長を妨げる可能性が高いです。

グリーン水素の利用を促進する有利な規制と政策は、市場に新たな成長機会を提供すると予測されます。

アジア太平洋が市場を独占し、予測期間中は欧州が最も高い年間成長率を記録すると予想されます。

グリーン水素市場の動向

電力およびその他のエンドユーザー産業セグメントが市場を独占する見込み

- 水素は非常に汎用性の高いエネルギー・キャリアであり、エネルギー・システムの脱炭素化において重要な役割を果たす可能性を秘めています。

- 風力発電所や太陽光発電所で生産された再生可能エネルギーは、圧縮ガスとして貯蔵されます。水素エネルギー貯蔵システムは、電気をグリーン水素に変換する電解槽、水素を圧縮ガスとして貯蔵する貯蔵設備、グリーン水素を電気に変換する燃料電池で構成されます。

- 世界の主要国は、主に脱炭素化を目指す発電セクターをターゲットに、水素貯蔵能力を増強しています。

- この推進は、補助金やインセンティブなど、さまざまな取り組みを通じて明らかになっています。例えば、米国政府は2023年、16のプロジェクトに約4,800万米ドルを割り当て、クリーン水素技術、特に燃料電池と貯蔵の促進に注力しています。

- 世界中の主要経済諸国は、気候変動目標を達成するために、水素を利用した統合的なグリーン発電ソリューションの採用を促進する革新的ソリューションの開発分野に取り組んでいます。重要な動きとして、2023年9月、インドの新・再生可能エネルギー省は、グリーン水素貯蔵を利用して100MWの24時間発電を行うパイロット・プロジェクトの計画を発表しました。

- さらに2024年4月、サトルジ・ジャル・ヴィディユット・ニガム(SJVN)は、インド初の多目的グリーン水素パイロット・プロジェクト、毎時20Nm3の電解槽と25kWの燃料電池容量に基づくグリーン水素パイロット・プロジェクト、ヒマーチャル州ジャクリのナスパ・ジャクリ水力発電所(NJHPS)の稼働を発表しました。

- 同様に、中国は2023年7月、甘粛省甘南州合作市に12MW/2MWhのグリーン水素ベースのエネルギー貯蔵施設を完成させ、躍進を遂げました。

- 数多くの市場企業が、グリーン水素を発電施設に統合する革新的なソリューションを開発しています。例えば、シーメンス・エナジーとシーメンス・ガメサは、グリーン水素を直接製造する単一の同期システムとして洋上風力タービンを開発するために、今後5年間で総額約1億2,000万ユーロの投資を目標としており、2025/2026年までに本格的な洋上実証が行われる予定です。

- グリーン水素の採用の高まりは、建築・電力セクターにおける積極的な脱炭素化の取り組みと相まって、調査対象市場の有望な姿を描き、今後数年間の堅調な成長を予測しています。

- さらに、グリーン水素(H2)のような低炭素燃料は、2050年までに温室効果ガス(GHG)排出量正味ゼロを目指す世界のエネルギーシステムの重要な構成要素となります。

- 国際再生可能エネルギー機関(IRNA)の報告書によると、世界における新規水素発電プロジェクトの数は年々変化しています。例えば、2022年には5つのプロジェクトがあったが、2023年には2つしかありませんでした。

- したがって、前述の要因は、電力およびその他のエンドユーザーエネルギー産業におけるグリーン水素の消費を促進すると予測されます。

アジア太平洋が市場を独占する見込み

- アジア太平洋が市場を独占すると予想されます。中国はこの地域で最大のGDPを誇り、中国とインドは世界で最も急速に経済が発展している国のひとつです。

- 2022年3月、中国は2021年から2035年までの初の長期水素計画を明らかにしました。この戦略的ロードマップは段階的なアプローチを強調し、技術の進歩と製造能力の強化を通じて国内の水素産業の成長を優先させるものです。特筆すべきは、2025年までに再生可能な資源から年間10万トンから20万トンの水素を製造することを目標とし、2035年までに再生可能な水素を経済で主流化し、中国のグリーンエネルギー移行を強化するという広範な目標を掲げていることです。さらに、同計画は多様な技術経路を提唱しており、今後15年間で再生可能エネルギー源の多様な組み合わせを促進するとしています。

- 中国の鉄鋼メーカーは、グリーン水素へのシフトの先頭に立ち、高炉操業のようなプロセスで化石燃料を置き換えることを目指しています。特に、大手鉄鋼メーカーのBaowuは、広東省湛江市でグリーン水素を燃料とする電気アーク炉の建設に着手しました。

- 鉄鋼、セメント、肥料のような産業は、二酸化炭素排出量が多いことで知られており、脱炭素化への圧力が高まっています。2030年までに化石燃料の輸入を1,000億インドルピー削減し、年間約5,000万トンのCO2排出量を削減することを目指す「グリーン水素国家ミッション」の野心的な目標と、インドの一致団結した努力により、グリーン水素はその移行における希望の光となっています。

- 同様に、NTPCリミテッドは2023年1月から、インドのグジャラート州スラートにあるカワス・タウンシップのPNGネットワークに最大8%のグリーン水素を混合するという重要な一歩を踏み出しました。

- 東京都は、遅れをとるどころか、公有地を利用したグリーン水素施設の開発で前進しています。都は、2024年度までに3基の建設を開始し、同年末までに1基の稼働を目指す意向を発表しました。しかし、政府からの更なる詳細な発表が待ち望まれます。

- 2024年1月、SKエコプラントはブルーム・エナジーと提携し、画期的なグリーン水素イニシアチブを開始しました。韓国南方電力および地方自治体との提携により、大規模な水素発電の導入を目指します。SKエコプラントは、ブルームの最先端の固体酸化物電解槽(SOEC)技術を活用し、韓国の済州島で輸送用燃料としてグリーン水素を製造します。2025年後半に予定されている今度の発表では、1.8メガワットの電解槽技術が導入されます。

- したがって、上記の要因はアジア太平洋におけるグリーン水素の消費を押し上げると予想されます。

グリーン水素産業の概要

世界のグリーン水素市場は部分的に統合されています。市場の主要企業には、China Petroleum &Chemical Corporation、Ningxia Baofeng Energy Group、Plug Power Inc.、China Three Gorges Corporation(CTG)、Tidewater Renewables Ltd.などがいる(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 化学産業における可能性の実現

- 炭素排出に関する環境問題の高まり

- 市場抑制要因

- グリーン水素の高い投資コスト

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 技術スナップショット

第5章 市場セグメンテーション

- エンドユーザー産業

- 精製

- 化学

- 鉄鋼

- 運輸

- 電力およびその他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- 世界のその他の地域

- 南米

- 中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)分析

- 主要企業の戦略

- 企業プロファイル

- Air Products and Chemicals Inc.

- Air Liquide

- BP PLC

- China Petroleum & Chemical Corporation

- China Three Gorges Corporation

- Engie

- Fortescue Future Industries

- Green Hydrogen International Corp.

- Iberdrola SA

- Intercontinental Energy

- LHYFE

- Linde PLC

- Ningxia Baofeng Energy Group Co. Ltd

- Plug Power Inc.

- Reliance Industries Limited

- Tidewater Renewables Ltd

- Uniper SE

- Yara

第7章 市場機会と今後の動向

- グリーン水素の利用を促進する有利な規制と政策

The Green Hydrogen Market size is estimated at 0.45 million tons in 2025, and is expected to reach 2.12 million tons by 2030, at a CAGR of 36.35% during the forecast period (2025-2030).

The COVID-19 pandemic moderately impacted the overall growth of the green hydrogen industry, owing to a halt in production and disruption in the supply chain. However, after the pandemic, the demand for green hydrogen increased in the transportation segment, which, in turn, has propelled the industry's growth.

Over the medium term, the demand for green hydrogen in the chemical industry and growing environmental concerns regarding carbon emissions are expected to drive the demand for green hydrogen.

On the flip side, the high investment cost of green hydrogen, limited access to technology and infrastructure, and high energy losses will likely hinder the industry's overall growth.

Favorable policies and regulations promoting the usage of green hydrogen are projected to offer new growth opportunities to the market.

Asia-Pacific is expected to dominate the market, and Europe will likely witness the highest annual growth rate during the forecast period.

Green Hydrogen Market Trends

The Power and Other End-user Industries Segment is Expected to Dominate the Market

- Hydrogen is a very versatile energy carrier that has the potential to play a significant role in decarbonizing the energy system.

- Renewable energy produced via wind or solar farms is stored as compressed gas. The hydrogen energy storage system consists of an electrolyzer to convert electricity to green hydrogen, a storage facility to store hydrogen as a compressed gas, and a fuel cell to convert green hydrogen to electricity.

- Leading economies worldwide are ramping up their hydrogen storage capacities, primarily targeting the power generation sector for decarbonization.

- This push is evident through various initiatives, such as grants and incentives. For example, in 2023, the US government allocated nearly USD 48 million across 16 projects, focusing on advancing clean hydrogen technologies, notably fuel cells and storage.

- Major economies around the globe are foraging into the field of developing innovative solutions to improve the adoption of integrated green hydrogen-based power generation solutions to meet climate goals. In a significant move, in September 2023, India's Ministry of New & Renewable Energy unveiled plans for a pilot project to generate 100 MW of round-the-clock power using green hydrogen storage.

- Moreover, in April 2024, Satluj Jal Vidyut Nigam (SJVN) announced the commissioning of India's first multi-purpose green hydrogen pilot project, a 20 Nm3/hr electrolyzer and 25 kW fuel cell capacity-based green hydrogen pilot project, Nathpa Jhakri Hydro Power Station (NJHPS) in Himachal's Jhakri.

- Similarly, China made strides in July 2023, inaugurating a 12 MW/2 MWh green hydrogen-based energy storage facility in Gannanzhou Cooperation City, Gansu Province.

- Numerous market players are developing innovative solutions to integrate green hydrogen into power generation facilities. For instance, Siemens Energy and Siemens Gamesa target a total investment of around EUR 120 million in the coming five years to develop an offshore wind turbine as a single synchronized system to directly produce green hydrogen, with a full-scale offshore demonstration expected by 2025/2026.

- The rising adoption of green hydrogen, coupled with aggressive decarbonization efforts in the building and power sectors, paints a promising picture for the market under study, projecting robust growth in the coming years.

- Additionally, low-carbon fuels, like green hydrogen (H2), will be a key component of the global energy system, which aims to achieve net zero greenhouse gas (GHG) emissions by 2050.

- According to the report of the International Renewable Energy Agency (IRNA), the number of new power-to-hydrogen projects worldwide has changed yearly. For instance, in 2022, there were five projects, and in 2023, there were only two.

- Therefore, the aforementioned factors are projected to boost the consumption of green hydrogen in the power and other end-user energy industries.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is expected to dominate the market. China has the largest GDP in the region, and China and India are among the fastest-emerging economies in the world.

- In March 2022, China revealed its first long-term hydrogen plan from 2021 to 2035. This strategic roadmap emphasizes a phased approach, prioritizing the growth of the domestic hydrogen industry through technological advancements and enhanced manufacturing capabilities. Notably, the plan targets producing 100,000 to 200,000 tons of hydrogen annually from renewable sources by 2025, with a broader goal of mainstreaming renewable hydrogen in the economy to bolster China's green energy transition by 2035. Additionally, the plan advocates for a diverse technology pathway, promoting a varied mix of renewable sources over the next 15 years.

- Chinese steelmakers spearhead the shift toward green hydrogen, aiming to replace fossil fuels in processes like Blast Furnace operations. Notably, Baowu, a major player, initiated the construction of a green hydrogen-fueled electric arc furnace in Zhanjiang, Guangdong.

- Industries like steel, cement, and fertilizers, known for their high carbon footprint, face mounting pressure for decarbonization. However, with India's concerted efforts and the ambitious targets set by the National Green Hydrogen Mission, which aims to slash INR 1 lakh crore worth of fossil fuel imports and nearly 50 million metric tons (MMT) of CO2 emissions annually by 2030, green hydrogen emerges as a beacon of hope in their transition.

- Similarly, NTPC Limited took a significant step starting in January 2023, blending up to 8% green hydrogen into the PNG Network at its Kawas Township in Surat, Gujarat, India.

- Tokyo is making strides in developing its green hydrogen facilities on publicly owned land rather than falling behind. The metropolitan government announced intentions to begin constructing three units by the fiscal year 2024, aiming to have one operational by the end of that year. However, further details from the government are eagerly anticipated.

- In January 2024, SK Ecoplant partnered with Bloom Energy for a groundbreaking green hydrogen initiative. Teaming up with Korea Southern Power and local authorities, they aim to introduce hydrogen power on a significant scale. SK Ecoplant will leverage Bloom's cutting-edge solid oxide electrolyzer (SOEC) technology to produce green hydrogen as a transport fuel on Jeju Island, South Korea. The upcoming presentation, scheduled to commence in late 2025, will involve the implementation of 1.8 megawatts of electrolyzer technology.

- Hence, the above-mentioned factors are expected to boost the consumption of green hydrogen in Asia-Pacific.

Green Hydrogen Industry Overview

The global green hydrogen market is partially consolidated. Some of the major players in the market include China Petroleum & Chemical Corporation, Ningxia Baofeng Energy Group Co. LTD, Plug Power Inc., China Three Gorges Corporation (CTG), and Tidewater Renewables Ltd (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Realizing the Potential in the Chemical Industry

- 4.1.2 Growing Environmental Concerns Regarding Carbon Emissions

- 4.2 Market Restraints

- 4.2.1 High Investment Cost of Green Hydrogen

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 End-user Industry

- 5.1.1 Refining

- 5.1.2 Chemicals

- 5.1.3 Iron and Steel

- 5.1.4 Transportation

- 5.1.5 Power and Other End-user Industries

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Rest of Europe

- 5.2.4 Rest of the World

- 5.2.4.1 South America

- 5.2.4.2 Middle East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Products and Chemicals Inc.

- 6.4.2 Air Liquide

- 6.4.3 BP PLC

- 6.4.4 China Petroleum & Chemical Corporation

- 6.4.5 China Three Gorges Corporation

- 6.4.6 Engie

- 6.4.7 Fortescue Future Industries

- 6.4.8 Green Hydrogen International Corp.

- 6.4.9 Iberdrola SA

- 6.4.10 Intercontinental Energy

- 6.4.11 LHYFE

- 6.4.12 Linde PLC

- 6.4.13 Ningxia Baofeng Energy Group Co. Ltd

- 6.4.14 Plug Power Inc.

- 6.4.15 Reliance Industries Limited

- 6.4.16 Tidewater Renewables Ltd

- 6.4.17 Uniper SE

- 6.4.18 Yara

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Favorable Policies and Regulations Promoting the Usage of Green Hydrogen