インドの建築用コーティング:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

India Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 60 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683769

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

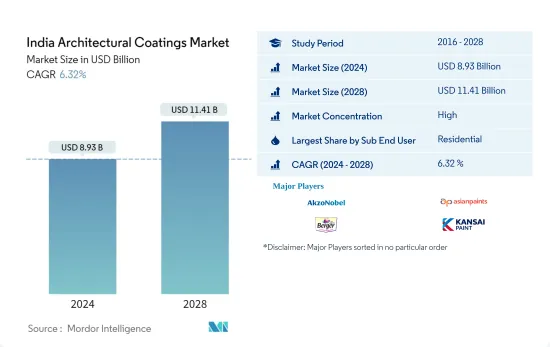

インドの建築用コーティング市場規模は2024年に89億3,000万米ドルと推定され、2028年には114億1,000万米ドルに達し、予測期間(2024-2028年)のCAGRは6.32%で成長すると予測されます。

主なハイライト

- エンドユーザー別最大セグメント:住宅:新築住宅の増加や建築に関する政府の取り組みにより、住宅セクターが建築用コーティング消費の大半を占めています。

- 技術別最大セグメント:水性:低VOC水性塗料に対する意識の高まりから、水性塗料が最大かつ最も急成長していると推定されます。

- 樹脂別最大セグメント:アクリル:インドでは価格に敏感なマーケットプレースであり、アクリル塗料は安価で低VOCであるため、アクリル塗料が樹脂市場を独占しています。

インドの建築用コーティング市場動向

サブエンドユーザー別では住宅が最大。

- 2016年と2017年のインドの建築用コーティング消費量は、悪魔撤廃とGST導入により減少しました。デモネティゼーションは、現金の入手が制限されたため、消費者の小売支出に影響を与えました。そのため、消費者は住宅塗装よりも日常生活に必要なものを優先的に購入するようになりました。2017年7月に施行された物品・サービス税は、塗料がGST税率28%に分類され、物品税、付加価値税(VAT)、入国税の形で支払われる24~27%よりも高くなったため、塗料業界にもかなりの影響を与えました。さらに、2017年の国内総生産(GDP)は前年比で1.5%減少しました。

- 消費は急速に回復し、床面積の増加と建設開発部門への外国直接投資(FDI)株式流入の増加により、2018年にピークに達しました。例えば、産業・国内貿易振興局(インド)によると、2018年のFDIは2017年の1億500万米ドルから5億4,000万米ドルに増加しました。

- 建築用コーティングの消費は、2019年に緩やかな成長が観察され、その後2020年には、COVID-19の国内での蔓延と50日間の全国的な封鎖のために、住宅と商業部門の両方で新規建設の減少のために減少しました。消費と販売の増加は、国内の人口増加と急成長する建設部門への積極的な投資により、予測期間中にかなりの割合で成長すると予想されます。IMFによると、インドの総人口は2022~26年の間に3.6%増加すると予想されています。

インドの建築用コーティング産業の概要

インドの建築用コーティング市場は適度に統合されており、上位5社で63.10%を占めています。同市場の主要企業は以下の通り。 AkzoNobel N.V., Asian paints, Berger Paints India, Kansai Paint and Nippon Paint Holdings(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 床面積動向

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- サブエンドユーザー

- 商業

- 住宅

- 技術

- 溶剤系

- 水性

- 樹脂

- アクリル

- アルキド

- エポキシ

- ポリエステル

- ポリウレタン

- その他の樹脂タイプ

第5章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Acro Paints Limited

- AkzoNobel N.V.

- Asian paints

- Axalta Coating Systems

- Berger Paints India

- Jotun

- JSW

- Kansai Paint Co.,Ltd.

- Nippon Paint Holdings Co., Ltd.

- Shalimar Paints

- Surfa Coats India Private Limited

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The India Architectural Coatings Market size is estimated at USD 8.93 billion in 2024, and is expected to reach USD 11.41 billion by 2028, growing at a CAGR of 6.32% during the forecast period (2024-2028).

Key Highlights

- Largest Segment by End-user - Residential : The residential sector dominated the architectural coating consumption due to the rising construction of new houses and the government initiatives for the building

- Largest Segment by Technology - Waterborne : The waterborne coating is estimated to be the largest and the fastest growing segment due to the rising awareness for the low VOC emission waterborne coatings.

- Largest Segment by Resin - Acrylic : The acrylic coating has dominated the resin market as the country is price sensitive marketplace and the acrylic coatings are cheaper and has low VOC emission.

India Architectural Coatings Market Trends

Residential is the largest segment by Sub End User.

- The architectural coating consumption in India dipped in 2016 and 2017 due to the demonetisation and introduction of GST. The demonetisation impacted the retail spending of the consumers due to limited availability of cash. Thus, diverting the priority of consumers spending on the daily needs rather than painting the houses. The Goods and service tax, which came into effect in July, 2017 also laid a considerable impact on the paint industry as the Paints have been classified in the GST tax rate slab of 28%, higher than 24-27% paid out in the form of excise, value added tax (VAT) and entry taxes. Furthermore, the country's GDP declined by 1.5% in 2017 compared to the previous years.

- The consumption recovered quickly and peaked in 2018 due to the higher addition of floor area and increasing foreign direct investment (FDI) equity inflows for the construction development sector. For instance, According to Department for Promotion of Industry and Internal Trade (India) the FDI in 2018 increased to 540 USD million from 105 USD million in 2017.

- The slow growth in the architectural coating consumption was observed in 2019 followed by a decline in 2020 due to lower new constructions in both residential cand commercial sector owing to the spread of covid-19 in the country and lockdown of 50 days across the country. The increase in consumption and sales is expected to grow at a significant rate in the forecasted period due to the rising population in the country and positive investment in the rapid growing construction sector. According to IMF, The total population in the country is expected to increase by 3.6% during the 2022-26.

India Architectural Coatings Industry Overview

The India Architectural Coatings Market is moderately consolidated, with the top five companies occupying 63.10%. The major players in this market are AkzoNobel N.V., Asian paints, Berger Paints India, Kansai Paint Co.,Ltd. and Nippon Paint Holdings Co., Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Floor Area Trends

- 3.2 Regulatory Framework

- 3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION

- 4.1 Sub End User

- 4.1.1 Commercial

- 4.1.2 Residential

- 4.2 Technology

- 4.2.1 Solventborne

- 4.2.2 Waterborne

- 4.3 Resin

- 4.3.1 Acrylic

- 4.3.2 Alkyd

- 4.3.3 Epoxy

- 4.3.4 Polyester

- 4.3.5 Polyurethane

- 4.3.6 Other Resin Types

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles

- 5.4.1 Acro Paints Limited

- 5.4.2 AkzoNobel N.V.

- 5.4.3 Asian paints

- 5.4.4 Axalta Coating Systems

- 5.4.5 Berger Paints India

- 5.4.6 Jotun

- 5.4.7 JSW

- 5.4.8 Kansai Paint Co.,Ltd.

- 5.4.9 Nippon Paint Holdings Co., Ltd.

- 5.4.10 Shalimar Paints

- 5.4.11 Surfa Coats India Private Limited

6 KEY STRATEGIC QUESTIONS FOR ARCHITECTURAL COATINGS CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 60 Pages

- 納期

- 2~3営業日