欧州の建築用塗料市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Europe Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 2044267

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

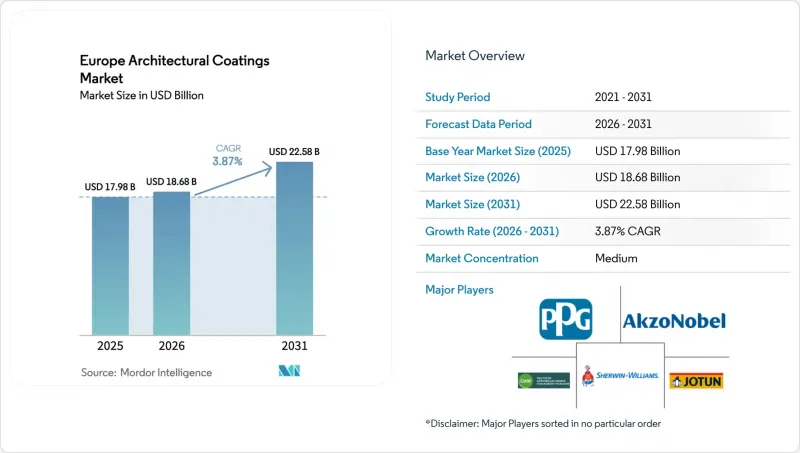

欧州の建築用塗料市場規模は、2025年の179億8,000万米ドルから2026年には186億8,000万米ドルへと拡大し、2031年までに225億8,000万米ドルに達すると予測されています。

2026~2031年にかけては、CAGR 3.87%で成長する見込みです。

購入者が、欧州の連合(EU)の厳格化されたVOC(揮発性有機化合物)排出上限や、平均築年数が50年を超えた建築ストックに対応するにつれ、高付加価値で低排出の配合への慎重な転換が、単純な数量の伸びを上回り始めています。プロの塗装業者が低臭気で洗浄しやすい製品を好むことや、小売業者がコンプライアンスリスクを回避するために多くの溶剤系製品を取り扱いを中止したことから、水性システムへの需要はすでに主流となっています。また、サプライヤー各社は、高金利により収益性が低下している新築工事よりも安定した利益が見込める修繕・改修プロジェクトへと事業を再配置しています。原料価格の高騰によるコスト負担を分散させ、環境配慮型の研究開発パイプラインに資金を投入し、市場展開の規模を強化するため、主要メーカー間の統合が加速しています。

欧州の建築用塗料市場の動向と洞察

老朽化した住宅ストックの改修ブーム

欧州には1990年以前に建設された住宅が2億2,000万戸以上あり、その多くは現代の衛生基準を満たすために、外壁の補修、防湿対策、内装の改修を必要としています。Eurostatの記録によると、2025年の住宅改修費は3,100億ユーロに達し、前年比12%増となりました。その支出の60%はフランス、ドイツ、イタリア、スペインが占めており、特にイタリアでは、省エネ塗料に対する手厚い税額控除のおかげで、単独で20%の急増を記録しました。欧州の議会は、2030年までに年間改修率を2%に倍増させることを目指しており、これにより、再塗装サイクルを7年から12年に延ばす耐久性の高いアクリルとポリウレタン系塗料への需要が高まっています。その結果、欧州の建築用塗料市場は、堅調な全体的な成長を維持しつつ、高利益率のセグメントへとシフトし続けています。

EUのVOC規制が水性塗料への移行を加速

欧州の委員会は2026年2月にEUエコラベル規則を改定し、VOCとSVOCの上限値を引き下げるとともに、バインダーの希釈を抑制する使用適性検査を追加しました。小売業者は、規制に適合しない溶剤系製品ラインを迅速に販売停止にしました。2025年末までに、水性製品は装飾用塗料の数量の70%を占めるようになり、5年間で5ポイント増加しました。現在、純粋なアクリルエマルジョンが内装壁用塗料の主流となっており、一方、スチレンアクリル混合塗料は低価格の外装用塗料へと移行しています。BASF、AkzoNobel、Arkemaは、2025年のパイロット検査において、塗料のカーボンフットプリントを40%削減するバイオ由来樹脂の有効性を確認しました。これらの動きは、規制の強化が水性塗料の普及を加速させるだけでなく、研究開発の規模を持たない中小の配合メーカーにとって参入障壁を高めることも裏付けています。その結果、欧州の建築用塗料市場は、科学による持続可能性の実績を持つ大手既存企業へと傾きつつあります。

二酸化チタンと石油系原料価格の変動

2025年、二酸化チタン(TiO2)のスポット価格は1トンあたり2,800ユーロから3,400ユーロの間で推移し、21%の変動幅が生じたことで、大衆市場用内装用エマルション塗料の粗利益率が圧迫されました。メーカー各社は、充填顔料や複合不透明剤を用いて価格高騰の一部を相殺しましたが、こうした代替品を使用すると、高い着色濃度において耐擦過性や色再現性が低下するリスクがあります。同時に、アクリルモノマーのコストはブレント原油価格に連動し、1バレルあたり75米ドルから95米ドルの範囲で推移しました。EUの関税により安価な中国産二酸化チタンが域内への流入を阻まれているため、現地の配合メーカーはアジアの競合他社に比べて、コストの底値が持続的に高止まりする状況に直面しています。

セグメント分析

住宅プロジェクトは2025年の売上高の68.96%を占め、2031年までCAGR4.04%で拡大する見込みです。老朽化した建物ストックの資産価値を維持する必要があるため、改修工事が主流となっており、また、国の税額控除により、省エネ型外装塗料の費用の最大30%が還付されるようになりました。イタリアはエコボーナス制度を拡充した後、2025年に20%の増加を記録し、支出を牽引しました。消費者は、喘息・アレルギー対応ラベルが付いた低臭気塗料や、塗り替えの間隔が10年持続すると謳われる耐擦傷性内装用エマルジョン塗料をますます指定するようになっています。この動向により、1戸当たりの使用量は減少しているも、平均販売価格は上昇しています。

商用途においても、建築用塗料への需要が高まっています。オフィスではハイブリッドワークへの適応が進み、必要な床面積が約15%削減されています。一方で、ホテル、医療、教育施設の改修工事は加速しており、いずれも業務への影響を最小限に抑えるため、速乾性でVOCゼロ、あるいは抗菌性の塗料が求められています。このセグメントでは、週末に迅速な塗り替えを実施できる供給パートナーが不可欠であり、中堅の地域ブランドはこのサービス面での強みを活用しています。欧州の全体での数量の回復は依然として不均一です。スペインではホスピタリティセグメントで二桁の伸びを見せていますが、ドイツでは資金調達の制約により、オフィス関連の案件が停滞しています。

その他の特典

- エクセル形態の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 老朽化した住宅ストックの改修ブーム

- EUのVOC規制が水性塗料への移行を加速

- コロナ禍後の商業施設内装市場の回復

- 省エネ断熱塗料への需要

- 現場での調色サービスプラットフォーム

- 市場抑制要因

- 二酸化チタンと石油原料価格の変動

- 高金利による新築住宅市場の低迷

- プロの塗装工の人手不足

- バリューチェーン分析

- 規制分析

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- エンドユーザー産業別

- 商用

- 家庭用

- 技術別

- 溶剤系

- 水性

- 樹脂別

- アクリル

- アルキド

- エポキシ

- ポリエステル

- ポリウレタン

- その他

- 地域別

- フランス

- ドイツ

- イタリア

- 北欧諸国

- ポーランド

- ロシア

- スペイン

- 英国

- その他の欧州

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- AkzoNobel N.V.

- Benjamin Moore & Co.

- Brillux GmbH & Co. KG

- CIN S.A.

- DAW SE

- Flugger group A/S

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- KOBER SRL

- Nippon Paint Holdings Co., Ltd.

- POLICOLOR SA

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Sniezka SA

- Sto SE & Co. KGaA

- Teknos Group

- Tikkurila

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日