|

市場調査レポート

商品コード

1911398

イタリアの施設管理市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Italy Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| イタリアの施設管理市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

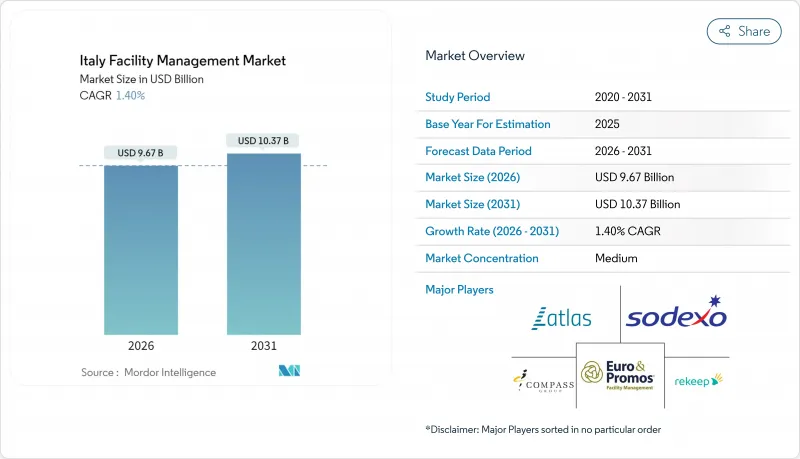

イタリアの施設管理市場は、2025年の95億4,000万米ドルから2026年には96億7,000万米ドルへ成長し、2026年から2031年にかけてCAGR 1.4%で推移し、2031年までに103億7,000万米ドルに達すると予測されております。

この着実な拡大は、国家復興・レジリエンス計画、商業用不動産の段階的な回復、電気・ガス価格の上昇にもかかわらず統合契約への需要増加に起因しています。予知保全の導入拡大、資産所有者によるESG監視の強化、新たな公共調達規則が、イタリア施設管理市場の競争構造を形成しました。一方、技術投資は引き続きIoT対応のHVAC最適化や遠隔資産監視へと移行しています。イタリア施設管理市場のハードサービス中核分野は2024年も堅調な基盤を維持しましたが、観光業が牽引する資本流入によりホテルや高級リゾート向けソフトサービスの需要が加速しました。北部地域の人手不足によりプロバイダーの利益率が圧迫されたため、自動化や成果連動型契約モデル(報酬を測定可能な建物性能指標に連動させる方式)への移行が進みました。

イタリア施設管理市場の動向と洞察

公共セクター機関におけるアウトソーシングの動向がFM市場を拡大

公共調達法(D.Lgs. 36/2023)による入札手続きの簡素化を受け、自治体予算の縮小が非中核業務のアウトソーシングを加速させました。これにより自治体は複数のサービスを成果連動型契約に統合可能となりました。例えばトスカーナ州では、38の博物館を一括して単一事業者に委託。調整コストを削減しつつサービス品質を向上させる、拡張可能な文化遺産アウトソーシングモデルの実例を示しています。大規模な枠組み契約は統一デジタルプラットフォームとIoT導入を促進し、イタリアの施設管理市場に持続的な成長の勢いをもたらしています。

イタリアの観光・ホスピタリティ産業の成長がソフトFMサービスの需要を押し上げる

2024年のホテル投資額は21億ユーロ(24億米ドル)を超え、過去10年間の平均を30%上回りました。これによりローマ、ヴェネツィア、ミラノのリゾート施設では、ハウスキーピング、コンシェルジュ、ケータリングといった高頻度サービスへの注力が強化されています。1日平均宿泊料金は4%上昇し、延べ6,450万人の観光客が訪れました。これにより、季節変動に応じて柔軟にキャパシティを調整できるプロバイダーが求められています。サステナビリティ認証やエネルギー効率の高いバックオフィス運営が主要な選定基準として浮上し、技術主導のソフトサービス提供をさらに推進するとともに、イタリアの施設管理市場の短期的な拡大を支えています。

イタリア各州の規制枠組みの分断化がコンプライアンスコストを複雑化

イタリアの20の州は、D.Lgs. 81/2008(労働安全衛生法)に基づく職場安全の執行権限を保持しており、検査スケジュールや書類形式に差異が生じています。2025年5月の国家・地域間協定による研修の統一化に向けた取り組みは不均等に進展し、複数地域にまたがるFMプロバイダーは個別対応型のコンプライアンスチームを維持せざるを得ず、地域横断的な規模の経済効果を阻害しています。こうしたコストは、イタリア施設管理市場における営業利益率の向上分の一部を相殺する結果となっています。

セグメント分析

2025年時点で、ハードサービスはイタリア施設管理市場シェアの58.85%を占めました。義務付けられた防火検査、MEP設備のアップグレード、空調設備の改修が、この優位性を支えました。特に病院施設では年間FM支出が平均161.58ユーロ/m2に達しています。ハードサービスの市場規模は、裁量的支出が減少した局面でもコンプライアンス主導の投資が需要を支えたため、緩やかな成長を維持しました。

しかしながら、ソフトサービスは2031年までCAGR2.38%の見通しを示しました。これは、高級観光の回復と、衛生・ケータリング・セキュリティ基準を向上させた職場プロトコルの進化に支えられたものです。医療・ホスピタリティ業界の顧客が感染管理手順を厳格化したことで、清掃サービスは特に大きな成長を遂げました。ラツィオ州本庁舎におけるデジタルツインの試験運用は、空間最適化分析が環境品質と居住者体験の連動性を強化する実例を示し、ソフトサービス提供者に高収益のアドバイザリー業務をもたらしました。

イタリアの施設管理市場は、サービスタイプ(ハードサービス、ソフトサービス)、提供形態(社内提供、外部委託)、エンドユーザー業界(商業(IT・通信、小売・倉庫)、ホスピタリティ(ホテル、飲食店、大規模レストラン)、公共・公共インフラ(政府、教育、交通機関))などにより区分されています。市場予測は金額ベース(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 現在の稼働率

- 主要FM事業者の収益性率

- 労働力指標- 労働参加率

- サービスタイプ別施設管理市場シェア(%)

- 施設管理市場シェア(%)、ハードサービス別

- 施設管理市場シェア(%)、ソフトサービス別

- 主要都市圏における都市化と人口増加

- イタリアのインフラ計画におけるセクター別投資優先順位

- 労働基準および安全基準に特化した規制要因

- 市場促進要因

- 公共部門機関におけるアウトソーシングの動向がFM市場を拡大

- イタリアの観光・ホスピタリティ産業の成長がソフトFMサービスの需要を促進

- コスト最適化のための統合施設管理契約の導入増加

- 老朽化した建物ストックに対する予知保全および改修サービスの必要性

- EU復興・レジリエンス基金による学校改修プロジェクト向け資金が地域FM事業の機会を促進

- 北イタリアにおけるデータセンター産業の拡大が専門的な技術的FM需要を促進

- 市場抑制要因

- イタリア各地域における規制枠組みの断片化がコンプライアンスコストを複雑化させております

- 熟練技術労働者のコスト上昇がFMプロバイダーの利益率を圧迫

- 5Gインフラの展開遅延がスマートビルFM導入を遅らせる

- COVID-19後の自治体予算制約により、中小都市における公共施設維持管理の外部委託が減少

- バリューチェーン分析

- PESTEL分析

- 新規参入企業向けの規制・法的枠組み

- マクロ経済指標がFM需要に与える影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資と資金調達分析

第5章 市場規模と成長予測

- サービスタイプ別

- ハードサービス

- 資産管理

- MEPおよびHVACサービス

- 消防システムと安全対策

- その他のハードFMサービス

- ソフトサービス

- オフィスサポートおよびセキュリティ

- 清掃サービス

- ケータリングサービス

- その他のソフトFMサービス

- ハードサービス

- 提供形態別

- 自社管理

- 外部委託

- 単一FM

- 包括型施設管理(Bundled FM)

- 統合型施設管理(Integrated FM)

- エンドユーザー業界別

- 商業施設(IT・通信、小売・倉庫など)

- ホスピタリティ(ホテル、飲食店、大規模レストラン)

- 公共・公共インフラ(政府、教育、交通機関)

- 医療(公的・民間施設)

- 工業・プロセス(製造業、エネルギー、鉱業)

- その他のエンドユーザー産業(集合住宅、娯楽、スポーツ・レジャー)

第6章 競合情勢

- 市場集中度

- 戦略的展開とパートナーシップ

- 市場シェア分析

- 企業プロファイル

- ATLAS I.F.M. SRL

- Sodexo Facilities Management Services(SODEXO GROUP)

- Compass Group PLC

- Euro & Promos Facility Management SPA(EURO & PROMOS)

- Rekeep SpA

- Olly Services SRL

- NAZCA

- Elmet SRL

- Apleona GmbH

- SGI Srl

- CNS Consorzio Nazionale Servizi

- Siram SpA

- BumaQ S.r.l.

- Ares Facility Management

- P&P Spa