|

市場調査レポート

商品コード

1683488

全身麻酔薬:世界の市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Global General Anesthesia Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 全身麻酔薬:世界の市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

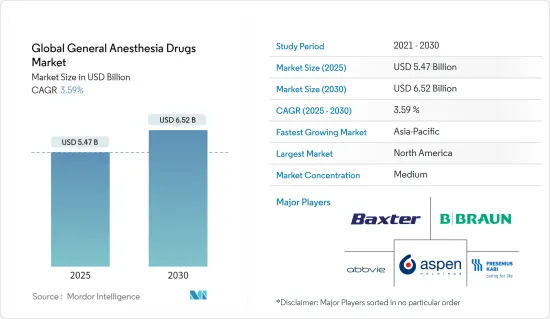

全身麻酔薬の世界市場規模は2025年に54億7,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは3.59%で、2030年には65億2,000万米ドルに達すると予測されています。

全身麻酔の主な目的は、外科手術中に患者の意識を失わせ、痛みを感じさせないようにすることです。がん、心血管疾患、関節炎などの疾病の有病率の増加は、医薬品、理学療法、手術を通じて疾病を効果的に管理する必要性を高め、その結果、手術中の自律神経反射を制御しながら患者の意識を失わせ、痛みの刺激を感じさせなくする全身麻酔薬の需要に拍車をかけています。

人口の間でがんの負担が増加しているため、がん細胞やリンパ節を切除する外科的介入による治療に対する需要が高まっています。したがって、このような処置に使用される全身麻酔薬の市場成長は、予測期間中に増大すると予想されます。例えば、米国がん協会が発表した2024年の統計によると、米国では2023年に192万人の新規がん患者が発生したのに対し、2024年には約200万人の新規がん患者が発生すると予想されています。

さらに、全米成人心臓手術監査報告2023によると、2022年の成人心臓手術件数は24,807件であったのに対し、2021年は19,333件でした。このことは、予測期間中、このような手術に使用される全身麻酔薬の需要を促進すると予想されます。さらに、世界保健機関(WHO)によると、2022年には、2030年までに世界の6人に1人が60歳になり、2050年までに60歳以上の世界人口は21億人に倍増すると言及されています。従って、高齢者人口が様々な慢性疾患に罹患しやすくなり、さらに手術が増えるにつれて、全身麻酔薬のニーズが高まり、予測期間中の市場成長につながります。

さらに、米国食品医薬品局(FDA)、ブラジル保健規制庁(ANVISA)、欧州医薬品庁(EMA)、米国医薬品庁(TGA)などの規制当局による先進的な全身麻酔製品の上市やパイプライン製品の承認の増加が、予測期間中の市場の成長を促進すると予想されます。例えば、2022年10月、Hikma社は、病院で全身麻酔に使用され、気管挿管を容易にし、手術中または人工呼吸中の筋弛緩をもたらす重要な医薬品である塩化サクシニルコリンを、プレフィルドシリンジの注射剤の形で米国で発売しました。

そのため、慢性疾患の手術件数の増加などの要因が全身麻酔薬の需要を高め、予測期間中の市場成長を牽引しています。しかし、小児患者や妊婦の全身麻酔に伴うリスクは、市場の成長を阻害する可能性があります。

全身麻酔薬市場の動向

プロポフォール分野は予測期間中に顕著な成長が見込まれる

プロポフォールは、全身麻酔の導入と維持に用いられる静脈麻酔薬です。プロポフォールの静脈内投与は意識障害の誘発に使用され、その後、複数の薬剤を組み合わせて麻酔を維持することができます。プロポフォールは、麻酔の導入維持と難治性てんかん状態の管理に使用されます。この薬剤は、麻酔を必要とするさまざまな外科手術に常に使用されてきました。

緊急手術の増加、高齢者人口の増加、薬剤の広範な使用、短時間作用性、世界の外科手術数の増加が、このセグメントの成長を促進する主な要因です。例えば、世界保健機関(WHO)の2023年報告書によると、外傷、がん、心血管疾患の発生率は上昇を続けており、外科的介入が公衆衛生システムに与える影響は世界的に拡大し続ける可能性があります。手術は、一般的な疾患による障害を軽減し、死亡リスクを低減できる唯一の治療法です。毎年、多くの人々が外科的治療を受けており、外科的介入は世界の障害調整生存年数の13%を占めると推定されています。例えば、米国疾病管理予防センターによる2023年11月の最新情報によると、米国では過去2年間に、不慮の事故による負傷で約2,500万件の救急外来受診が報告されています。同じ出典によると、2023年の最後の3ヵ月間に活動制限のある怪我をした18歳以上の成人の割合は5.9%でした。したがって、怪我や関連手術のケースの増加は、プロポフォールの採用を促進し、予測期間中のセグメントの成長につながると予想されます。

さらに、主要市場プレーヤーとその戦略的活動(製品の発売や提携など)は、予測期間中の同分野の成長に有利に働くと予想されます。例えば、2022年8月、急性期および重症治療薬の変革に注力する製薬企業Genixus社は、年次全国薬局購買協会会議において、RTAシリンジ製品のKinetiXプラットフォーム内の最初の製品としてプロポフォールを提供することを報告しました。新しいプロポフォールシリンジは、ワークフローを簡素化し、効果的なケアの提供をサポートするために設計されたKinetix RTAプラットフォーム内で利用可能な最初の製品の一つです。同様に、2022年4月、アベット・ファーマシューティカルズ・インクは、ディプリバン(プロポフォール)注射用乳剤USPのAB評価ジェネリック医薬品である、20、50、100mlの単一患者用バイアル入りプロポフォール注射用乳剤USP 10mg/mLを、食品医薬品局(FDA)からの略式新薬承認を受けて発売しました。

したがって、プロポフォールの利点、新しい開発、外科的介入の必要性により、このセグメントは予測期間中にかなりの成長が見られると考えられています。

北米は予測期間中に大幅な成長が見込まれる

北米は、慢性疾患のリスクが高く、ヘルスケアインフラが整っていることから、予測期間中に大きな成長が見込まれます。さらに、高齢化人口の増加と外科手術の需要も北米市場の成長に寄与しています。

例えば、心血管疾患のリスク増大は、患者を治療するための様々な全身麻酔薬の必要性を高めています。米国疾病予防管理センター(Centers for Disease Control and Prevention)によると、2022年には、米国では毎年約80万5,000人が心臓発作を起こし、そのうち60万5,000人が最初の心臓発作を起こし、約20万人がすでに心臓発作を起こしているにもかかわらず、2回目の心臓発作を起こすと発表されています。したがって、この要因が市場の成長を高めています。さらに、全身麻酔は膝関節置換術や開心術などの大手術によく使用されます。例えば、2023年8月にNational Library of Medicineに掲載された論文更新によると、冠動脈バイパス移植(CABG)手術は年間約40万件行われており、米国で最も行われている大手術です。このように、米国では心臓手術の普及率が高いため、全身麻酔薬の需要が高まり、予測期間中の市場の成長に拍車がかかる可能性があります。

さらに、Demographic Outlook(人口統計学的展望)によると、2024年から2054年まで、米国では心臓手術の普及率が高い:米国議会予算局(CBO)が発表した2024年から2054年までの人口動態見通しによると、2024年には25歳から64歳の人口と65歳以上の人口の比率は2.9対1になるとCBOは予測しています。2054年には2.2対1になるかもしれないです。高齢者人口の増加は、心血管疾患や神経疾患など、高齢者の慢性疾患の急増をもたらし、麻酔薬の需要を押し上げています。

さらに、全身麻酔薬の製品上市、規制当局の承認、臨床試験研究の増加が、予測期間中の米国市場の成長をさらに促進すると予想されます。例えば、2022年4月、Sedana Medical社は、集中治療室(ICU)で機械的に人工呼吸された患者の鎮静のために、Sedaconda ACD-S装置システムを介して投与される吸入イソフルランの安全性と有効性を静脈内プロポフォールと比較する臨床試験を米国で実施しました。したがって、全身麻酔薬が提供するこのような結果やさらなる利点は、北米での採用を増加させ、予測期間中の市場成長につながる可能性が高いです。

したがって、外科手術の増加、麻酔薬の有効性を実証するための臨床研究の増加、主要な市場プレイヤーの存在と製品発売などの戦略的活動により、市場は北米で顕著な成長を示すと予想されます。

全身麻酔薬産業の概要

全身麻酔薬市場は、複数の主要市場プレイヤーの存在により、半固有の性質を持っています。市場プレーヤーは、世界中で製品ポートフォリオを改善するために、合併、買収、製品発売、研究開発活動など、さまざまな戦略的活動に継続的に取り組んでいます。市場の主要企業には、AbbVie Inc.、Paion AG、Aspen Holdings、Baxter International Inc.、Fresenius SE &Co.KGaAなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 手術件数の増加

- 新薬の承認と上市

- 市場抑制要因

- 全身麻酔薬の副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 薬剤タイプ別

- セボフルラン

- デスフルラン

- イソフルラン

- 亜酸化窒素

- プロポフォール

- その他の薬剤

- 投与経路別

- 吸入

- 静脈内投与

- 手術タイプ別

- 一般外科

- がん手術

- 心臓手術

- 人工膝関節置換術

- その他の手術

- エンドユーザー別

- 病院

- 外来手術センター

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Aspen Holdings

- Paion AG

- AbbVie Inc.

- Endo International plc(Par Pharmaceutical Inc.)

- Baxter International Inc.

- Safeline pharmaceuticals

- Fresenius SE & Co. KGaA

- Hikma Pharmaceuticals plc

- Pfizer Inc.

- Piramal Critical Care

- AVET Pharmaceuticals Inc.

第7章 市場機会と今後の動向

The Global General Anesthesia Drugs Market size is estimated at USD 5.47 billion in 2025, and is expected to reach USD 6.52 billion by 2030, at a CAGR of 3.59% during the forecast period (2025-2030).

The primary goal of general anesthesia is to make a patient unconscious and not feel pain during the surgical procedure. The increasing prevalence of diseases such as cancer, cardiovascular diseases, arthritis, and others among the population raises the need for effective management of the disease through pharmaceuticals, physical therapy, and surgeries, which in turn fuel the demand for general anesthesia drugs to render a patient unconscious and unable to feel painful stimuli while controlling autonomic reflexes during surgeries.

The increasing burden of cancer among the population raises the demand for treatment through a surgical intervention that involves removing cancer cells and lymph nodes that are affected. Hence, the market growth of general anesthesia drugs used in such procedures is anticipated to augment over the forecast period. For instance, according to 2024 statistics published by the American Cancer Society, about 2 million new cancer cases are expected to be diagnosed in the United States in 2024, compared to 1.92 million new cancer cases in 2023.

Furthermore, according to the National Adult Cardiac Surgery Audit Report 2023, the number of adult heart operations in 2022 was 24,807 compared to 19,333 in 2021. This, in turn, is expected to fuel the demand for general anesthesia drugs used in such procedures over the forecast period. Moreover, according to the World Health Organization, in 2022, it was mentioned that by 2030, one in six people in the world would be aged 60 years, and by 2050, the world's population of people aged 60 years and older would double to 2.1 billion. Therefore, as the senior population is more prone to various chronic diseases and further surgeries, the need for general anesthesia drugs elevates, leading to market growth over the forecast period.

Moreover, increase in advanced general anesthesia product launches and the approvals of pipeline products by regulatory agencies such as the US Food and Drug Administration (FDA), Brazilian Health Regulatory Agency (ANVISA), European Medicines Agency (EMA), Therapeutic Goods Administration (TGA) among others, are expected to fuel the market's growth over the forecast period. For instance, in October 2022, Hikma launched Succinylcholine Chloride, an important medicine used in hospitals for general anesthesia, to facilitate tracheal intubation, and to provide muscle relaxation during surgery or mechanical ventilation in the form of an injection in a prefilled syringe form in the United States.

Therefore, factors such as the rising number of surgeries for chronic diseases raise the demand for general anesthesia drugs, driving the market's growth during the forecast period. However, risks associated with general anesthesia in pediatric patients and pregnant women may likely impede market growth.

General Anesthesia Drugs Market Trends

Propofol Segment is Expected to Witness a Notable Growth Over the Forecast Period

Propofol is an intravenous anesthetic agent used for the induction and maintenance of general anesthesia. Intravenous (IV) administration of Propofol is used to induce unconsciousness, after which anesthesia may be maintained using a combination of medications. Propofol is used for the induction maintenance of anesthesia and the management of refractory status epilepticus. The drug has always been used for various surgical procedures requiring anesthesia.

The increasing incidences of emergency surgeries, a growing senior population, extensive usage of the drug, short-acting characteristics, and a growing number of surgical procedures worldwide are the major factors propelling the segment's growth. For instance, as per the World Health Organization 2023 report, the incidences of traumatic injuries, cancers, and cardiovascular disease continue to rise, and the impact of surgical intervention on public health systems may continue to grow globally. Surgery is the only therapy that can alleviate disabilities and reduce the risk of death from common conditions. Each year, many people undergo surgical treatment, and surgical interventions account for an estimated 13% of the world's total disability-adjusted life years. For instance, as per the November 2023 update by the Centers for Disease Control and Prevention, about 25 million emergency department visits for unintentional injuries were reported in the United States in the past two years. As per the same source, the share of adults age 18 and older who had an activity-limiting injury during the last three months of 2023 was 5.9%. Hence, an increase in cases of injuries and related surgeries is expected to bolster the adoption of Propofol, leading to segment growth over the forecast period.

Furthermore, key market players and their strategic activities, such as product launches and collaborations, are expected to favor the segment's growth over the forecast period. For instance, in August 2022, Genixus, a pharmaceutical company focused on transforming acute and critical care medicines, reported offering Propofol as the first product within its KinetiX platform of RTA syringe products at the Annual National Pharmacy Purchasing Association Conference. The new Propofol Syringe is one of the first products available within the Kinetix RTA platform, designed to simplify workflow and support effective care delivery. Similarly, in April 2022, Avet Pharmaceuticals Inc. launched its Propofol Injectable Emulsion, USP 10 mg/mL, in 20, 50, and 100-ml Single Patient-Use Vials, an AB-rated generic equivalent of DIPRIVAN (Propofol) Injectable Emulsion USP, following its abbreviated new drug application approval from the Food and Drug Administration (FDA).

Hence, owing to the benefits of Propofol, the new developments, and the need for surgical interventions, the segment is believed to witness considerable growth during the forecast period.

North America is Expected to Witness a Significant Growth Over the Forecast Period

North America is expected to witness significant growth over the forecast period due to the region's increased risk of chronic diseases and favorable healthcare infrastructure. Furthermore, an increase in the aging population, along with the demand for surgical procedures, also contributes to the growth of the market in North America.

For instance, the increased risk of cardiovascular diseases is elevating the need for various general anesthesia drugs to treat patients. According to the Centers for Disease Control and Prevention, in 2022, it was stated that every year, around 805,000 people in the United States have a heart attack, out of which 605,000 have a first heart attack and about 200,000 people have already had a heart attack have a second attack. Hence, this factor is elevating the growth of the market. Additionally, general anesthesia is commonly used for major operations, such as knee replacement or open-heart surgery. For instance, according to the article update published in August 2023 in the National Library of Medicine, approximately 400,000 coronary artery bypass grafting (CABG) surgeries are performed yearly, making it the most performed major surgical procedure in the United States. Thus, a high prevalence of cardiac surgery procedures across the United States may create a demand for general anesthetic drugs, fueling the market's growth over the forecast period.

Moreover, according to the Demographic Outlook: 2024 to 2054 published by the Congressional Budget Office (CBO), in 2024, the ratio of people aged 25 to 64 to 65 or older maybe 2.9 to 1, CBO projects. By 2054, it may be 2.2 to 1. Growth in the aged population resulted in a sharp increase in the number of chronic conditions among older people, such as cardiovascular and neurological ailments, driving up demand for anesthetic medicines.

Furthermore, increased product launches, regulatory approvals, and clinical trial studies for general anesthetic drugs are further expected to fuel the US market's growth over the forecast period. For instance, in April 2022, Sedana Medical conducted a clinical trial in the United States to compare the safety and efficacy of inhaled isoflurane administered via the Sedaconda ACD-S device system versus intravenous propofol for sedation of mechanically ventilated patients in the Intensive Care Unit (ICU). Hence, such results and further benefits offered by general anesthetic drugs will likely increase their adoption in North America, leading to market growth over the forecast period.

Hence, due to the increase in surgical procedures, the rise in clinical studies to demonstrate the efficacy of anesthesia drugs, and the presence of major market players coupled with their strategic activities, such as product launches, the market is expected to witness notable growth in North America.

General Anesthesia Drugs Industry Overview

The general anesthesia drugs market is semi-consolidated in nature due to the presence of several key market players. The market players are continuously involved in various strategic activities such as mergers, acquisitions, product launches, and research and development activities to improve their product portfolio across the globe. Some of the key players in the market include AbbVie Inc., Paion AG, Aspen Holdings, Baxter International Inc., and Fresenius SE & Co. KGaA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Number of Surgeries

- 4.2.2 New Drug Approvals and Launches

- 4.3 Market Restraints

- 4.3.1 Side Effects of General Anesthetics

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type of Drugs

- 5.1.1 Sevoflurane

- 5.1.2 Desflurane

- 5.1.3 Isoflurane

- 5.1.4 Nitrous Oxide

- 5.1.5 Propofol

- 5.1.6 Other Drugs

- 5.2 By Route of Administration

- 5.2.1 Inhalation

- 5.2.2 Intravenous

- 5.3 By Surgery Type

- 5.3.1 General Surgery

- 5.3.2 Cancer Surgery

- 5.3.3 Heart Surgery

- 5.3.4 Knee and Hip Replacements

- 5.3.5 Other Surgery Types

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aspen Holdings

- 6.1.2 Paion AG

- 6.1.3 AbbVie Inc.

- 6.1.4 Endo International plc (Par Pharmaceutical Inc.)

- 6.1.5 Baxter International Inc.

- 6.1.6 Safeline pharmaceuticals

- 6.1.7 Fresenius SE & Co. KGaA

- 6.1.8 Hikma Pharmaceuticals plc

- 6.1.9 Pfizer Inc.

- 6.1.10 Piramal Critical Care

- 6.1.11 AVET Pharmaceuticals Inc.