|

市場調査レポート

商品コード

1911292

欧州の配電変圧器市場- シェア分析、業界動向、統計、成長予測(2026年~2031年)Europe Distribution Transformer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の配電変圧器市場- シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

概要

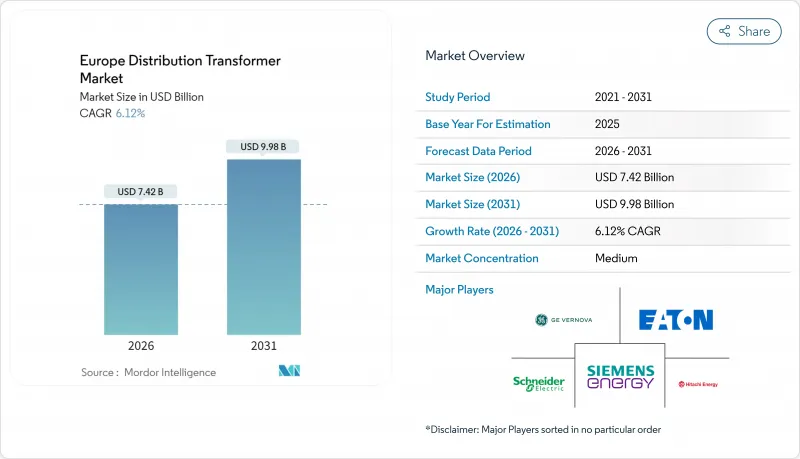

欧州の配電変圧器市場規模は、2026年に74億2,000万米ドルに達すると予測されております。

2025年の69億9,000万米ドルから成長し、2031年には99億8,000万米ドルに達する見込みで、2026年から2031年にかけてCAGR6.12%で拡大すると見込まれております。

堅調な成長の背景には、送電網近代化への資金投入、EUの厳格化するエネルギー効率規制、電気自動車充電拠点やハイパースケールデータセンター群からの需要急増が挙げられます。パンデミックによる停滞を経て、電力事業者の設備投資計画は増加傾向にあり、ネットワーク損失削減と再生可能エネルギー統合のための受入容量拡大を目的に、デジタル技術を搭載した高効率ユニットの導入が進められています。同時に、EUの「Fit for 55」パッケージによる仕様変更が、プレミアム効率コアや生分解性絶縁油への調達シフトを促し、平均販売価格を押し上げつつも寿命損失を低減させています。電磁鋼板のサプライチェーン逼迫は依然として生産の足かせとなっていますが、戦略的備蓄、複数調達先確保、段階的な生産能力増強により、短期納品への影響は緩和されつつあります。主要OEMメーカーによる合併や工場拡張は、地理的展開とコスト競争力における競合激化を示唆しています。一方、電力会社は供給確保のため枠組み契約による発注の集約を進めています。

欧州配電変圧器市場の動向と展望

2024年以降の送電網近代化投資回復

欧州投資銀行は2025年に1,000億ユーロ(1,070億米ドル)を計上し、うち110億ユーロ(118億米ドル)を電力網アップグレードに充てる予定です。注目すべきプロジェクトとしては、4億ユーロ(4億2,800万米ドル)を投じるチェコの配電網アップグレードや、イベルドローラ社による1億ユーロ(1億700万米ドル)のバレンシアネットワーク再設計などが挙げられます。こうした資金調達により、延期されていた公益事業プロジェクトが再開され、迅速な展開に適した標準化された高効率テンプレートに適合する中容量ユニットの一括調達が促進されています。受注が固まるにつれ、OEM各社はドイツ、ポーランド、イタリアで工場稼働率を向上させており、欧州の配電変圧器市場における納期短縮が進んでいます。

EU「Fit for 55」エネルギー効率化指令

Fit-for-55立法パッケージは、2030年までに温室効果ガスを55%削減することを目指しており、電力会社は従来のTier 1機器をTier 2準拠モデルに交換し、2027年までに導入が予想されるTier 3への準備を迫られています。変圧器損失は93TWh(EU発電量の2.9%)を占め、大きな技術的節約余地を提供しています。このため電力会社は、初期費用が15~20%高いにもかかわらず、アモルファス金属コア、先進的なステップラップ設計、エステル充填タンクを仕様に採用しています。欧州の配電用変圧器市場では、入札期間の長期化と、初期コストよりもライフサイクル効率を優先する価値ベースの落札基準が進行中です。

電磁鋼板積層板のリードタイム長期化

世界の方向性電磁鋼板の供給逼迫は継続しており、リードタイムは3~4年に延び、価格は2020年比で約2倍に上昇しています。材料費が完成品単価の45%を占める状況下、メーカーは割当配分を調整し、高利益率の受注を優先せざるを得ません。このボトルネックは特に100MVA超のカテゴリーに影響を及ぼし、欧州配電変圧器市場の需要を牽引する大規模な国境を越えた連系プロジェクトの遅延を招く可能性があります。

セグメント分析

2025年時点において、小型変圧器(10MVA以下)は欧州配電変圧器市場で最大の45.12%のシェアを維持し、屋上太陽光発電の接続、複合用途不動産の電化、郊外配電線路向けに供給されています。短納期生産サイクルとカタログベース設計により迅速な導入が可能となっています。しかしながら、ENTSO-E(欧州送電系統運用者連合)の10年ネットワーク開発計画に基づく資本集約的な送電網増強により、100MVA超の機器需要がCAGR6.74%で拡大しています。新規400kV送電回廊や洋上風力発電陸揚げステーションの開発を背景に、欧州の大型変圧器市場規模は2031年までに33億1,000万米ドルに達すると予測されます。メーカー各社は、これらの特注モデル向けの工場受入試験期間を短縮するため、専用の生産棟と高電圧試験場を設けております。電力会社は、40年の耐用年数と相対的な損失低減により、高価格を相殺し、総所有コストの経済性を維持しております。

油冷式設計は2025年の収益の79.85%を占め、熱的余裕とコスト効率の高さから今後も中核を成し続ける見込みです。OEMメーカーは濾過システムと水分監視システムのアップグレードにより油寿命を25年に延長し、電力会社の更新判断を支援しています。天然・合成エステル油を用いたパイロットプロジェクトも進展中です。2025年、R&Sグループはスウェーデンの電力会社向けにNytro BIO 300X充填の40MVAユニットを出荷し、実稼働性能を実証いたしました。エステル油への関心は、鉱物油漏洩リスクが許容されない火災感受性の高いトンネル、港湾、都市変電所で最も高まっております。空冷式ユニットは、ゼロ可燃性が求められる地下鉄、半導体工場、データセンターで引き続き使用されていますが、珪素鋼板価格の上昇により利益率の圧迫に直面しています。EU SSTARプログラムの資金提供を受けた固体変圧器モジュールの革新は将来のニッチ市場を開拓する可能性がありますが、高コストのため現時点では導入は限定的です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 2024年以降の送電網近代化投資回復

- EU「Fit for 55」エネルギー効率化指令

- データセンター集積地における中圧・低圧変圧器の改修需要急増

- TEN-T回廊におけるEV充電拠点の展開

- 農村地域における再生可能エネルギーハイブリッドマイクログリッドの迅速な導入

- 公益事業主導による生分解性エステル流体のパイロット導入

- 市場抑制要因

- 電磁鋼板のリードタイム長期化

- 都市部変電所における騒音・設置面積制限の強化

- 鉱物油変圧器用ベースオイル原料の価格変動性

- 配電事業者(DSO)の料金凍結交渉に伴う設備投資(CAPEX)の延期

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 出力定格別

- 大型(100 MVA以上)

- 中型(10~100 MVA)

- 小型(10 MVA以下)

- 冷却方式別

- 空冷式

- 油冷式

- 相数別

- 単相

- 三相

- エンドユーザー別

- 電力会社

- 産業用

- 商業用

- 住宅用

- 地域別

- ドイツ

- 英国

- フランス

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、パートナーシップ、PPA)

- 市場シェア分析(主要企業の市場順位・シェア)

- 企業プロファイル

- Hitachi Energy Ltd.

- Siemens Energy AG

- Schneider Electric SE

- Eaton Corporation plc

- GE Vernova

- SGB-SMIT Group

- CG Power Systems Belgium NV

- Westrafo SRL

- SEA SpA(Societa Elettromeccanica Arzignanese)

- GBE SpA

- Brush Transformers Ltd.

- Ormazabal(Velatia)

- Efacec Power Solutions SA

- VEO Oy

- JST Transformateurs

- Koncar D&ST Inc.

- Kolektor Etra d.o.o.

- Wilson Power Solutions Ltd.

- WEG Transformers Europe

- Hyosung Heavy Industries Co., Ltd.