|

市場調査レポート

商品コード

1666573

乾式配電変圧器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Dry Type Distribution Transformer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 乾式配電変圧器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月19日

発行: Global Market Insights Inc.

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

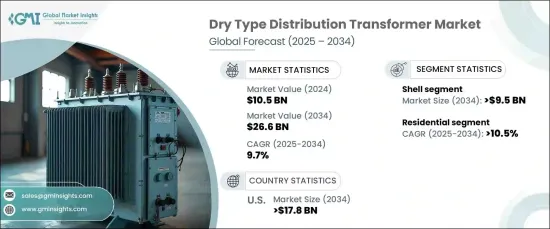

世界の乾式配電変圧器市場は2024年に105億米ドルとなり、2025年から2034年にかけてCAGR9.7%という驚異的な成長が見込まれています。

市場拡大の主な要因は、技術革新、環境規制の強化、最新の電力システムのニーズの進化です。乾式変圧器は、その強化された安全機能、環境に優しい設計、運用効率により、好まれる選択肢になりつつあります。油入り変圧器とは異なり、乾式変圧器は可燃性液体を使用しないため、より安全で持続可能な選択肢となっています。

都市化が加速し、産業が成長するにつれて、効率的で環境に優しい配電ソリューションに対する需要は増加の一途をたどっています。再生可能エネルギー源やスマートグリッドとの統合といった技術の進歩が、配電ソリューションの採用をさらに後押ししています。さらに、二酸化炭素排出量の削減を重視する世界の環境規制の強化により、乾式変圧器は電力インフラにとって不可欠な存在となっています。持続可能性とエネルギー効率に強く焦点を当てたこの市場は、今後10年間で大きく成長する見通しです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 105億米ドル |

| 予測金額 | 266億米ドル |

| CAGR | 9.7% |

特に、シェルコアセグメントが市場を席巻し、2034年には95億米ドルに達すると予測されています。シェルコア変圧器の優れた性能とコンパクトな設計は、スペースの最適化とエネルギー効率が重要な分野に理想的です。これらの変圧器は、再生可能エネルギー、スマートグリッド、都市インフラなどの産業でますます利用されるようになっています。その効率性と安全性は、持続可能で近代的な配電システムに対する需要の高まりに完全に合致しています。スマートグリッドと再生可能エネルギーソリューションへの世界のシフトが続く中、シェルコア変圧器の採用は大幅に増加すると予想されます。

住宅部門も力強い成長を遂げており、2034年までのCAGRは10.5%と予測されています。都市部や住宅用途で乾式変圧器の導入が増加しているのは、より安全でスペース効率の高いソリューションが求められているためです。都市部の人口密度が高まるにつれ、これらの変圧器はより狭いスペースでの配電に理想的なソリューションを提供します。さらに、太陽光発電やスマートグリッドのような再生可能エネルギー源の統合が、住宅地での採用を促進しています。エネルギー効率の高い住宅を選ぶ消費者が増える中、乾式変圧器は持続可能性の目標を達成しながら信頼性の高い配電を維持するために不可欠です。

米国では、乾式配電変圧器市場は2034年までに178億米ドルを創出すると予測されています。再生可能エネルギーへの注目の高まりは、厳しいエネルギー効率規制と相まって、乾式変圧器の採用を大きく後押ししています。乾式変圧器は、都市インフラ、電気自動車充電ステーション、スマートグリッドシステムなどの用途でますます使用されるようになっています。よりクリーンで信頼性の高い電力ソリューションへの需要が高まるにつれ、乾式変圧器はエネルギー事情に欠かせない存在になりつつあります。都市化と産業開発が進む中、これらの変圧器は米国全域で持続可能かつ効率的な配電を確保する上で重要な役割を果たしています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有償

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 規制状況

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 成長ポテンシャル分析

- ポーター分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:コア別、2021年~2034年

- 主要動向

- クローズド

- シェル

- ベリー

第6章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- オープンワウンド

- キャスト樹脂

- 真空加圧含浸

- 真空加圧カプセル化

第7章 市場規模・予測:巻線別、2021年~2034年

- 主要動向

- 2巻線

- オートトランス

第8章 市場規模・予測:定格別、2021~2034年

- 主要動向

- 250 kVA以下

- 250 kVA~1 MVA

- 1 MVA以上

第9章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業・産業用

- ユーティリティ

第10章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第11章 企業プロファイル

- ABB

- Bharat Heavy Electricals

- CG Power and Industrial Solutions

- Eaton

- Fuji Electric

- GE

- Hitachi Energy

- Instrument Transformer Equipment

- Raychem RPG

- Schneider Electric

- SGB SMIT

- Siemens Energy

- TMC Transformers

- Toshiba Energy Systems and Solutions

- URJA Techniques

- WEG

The Global Dry Type Distribution Transformer Market was valued at USD 10.5 billion in 2024, with expectations to grow at an impressive CAGR of 9.7% between 2025 and 2034. The market's expansion is primarily driven by technological innovations, increasing environmental regulations, and the evolving needs of modern power systems. Dry-type transformers are becoming the preferred choice due to their enhanced safety features, eco-friendly design, and operational efficiency. Unlike oil-filled transformers, dry-type transformers do not use flammable liquids, making them a safer and more sustainable option.

As urbanization accelerates and industrial growth increases, the demand for efficient, environmentally friendly electrical distribution solutions continues to rise. Technological advancements, such as integration with renewable energy sources and smart grids, are further boosting their adoption. Additionally, stricter global environmental regulations, which emphasize reducing carbon footprints, are making dry-type transformers an essential part of the power infrastructure landscape. With a strong focus on sustainability and energy efficiency, this market is poised for significant growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.5 Billion |

| Forecast Value | $26.6 Billion |

| CAGR | 9.7% |

In particular, the shell-core segment is expected to dominate the market, projected to reach USD 9.5 billion by 2034. The superior performance and compact design of shell-core transformers make them ideal for sectors where space optimization and energy efficiency are critical. These transformers are increasingly utilized in industries such as renewable energy, smart grids, and urban infrastructure. Their efficiency and safety features align perfectly with the growing demand for sustainable and modern power distribution systems. As the global shift toward smart grids and renewable energy solutions continues, the adoption of shell-core transformers is expected to rise substantially.

The residential sector is also experiencing robust growth, with a projected CAGR of 10.5% through 2034. The increasing deployment of dry-type transformers in urban and residential applications is driven by the need for safer, space-efficient solutions. As urban areas become more densely populated, these transformers provide an ideal solution for power distribution in smaller spaces. Moreover, the integration of renewable energy sources like solar power and smart grids is driving their adoption in residential areas. With more consumers opting for energy-efficient homes, dry-type transformers are essential for maintaining reliable power distribution while meeting sustainability goals.

In the U.S., the dry-type distribution transformer market is forecasted to generate USD 17.8 billion by 2034. The growing focus on renewable energy, coupled with strict energy efficiency regulations, is significantly driving the adoption of dry-type transformers. They are increasingly used in applications such as urban infrastructure, electric vehicle charging stations, and smart grid systems. As the demand for cleaner and more reliable power solutions rises, dry-type transformers are becoming an indispensable part of the energy landscape. With continued urbanization and industrial development, these transformers are playing a crucial role in ensuring sustainable and efficient power distribution across the U.S.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Core, 2021 – 2034 (‘000 Units, USD Million)

- 5.1 Key trends

- 5.2 Closed

- 5.3 Shell

- 5.4 Berry

Chapter 6 Market Size and Forecast, By Product, 2021 – 2034 (‘000 Units, USD Million)

- 6.1 Key trends

- 6.2 Open wound

- 6.3 Cast resin

- 6.4 Vacuum pressure impregnated

- 6.5 Vacuum pressure encapsulated

Chapter 7 Market Size and Forecast, By Winding, 2021 – 2034 (‘000 Units, USD Million)

- 7.1 Key trends

- 7.2 Two winding

- 7.3 Auto transformer

Chapter 8 Market Size and Forecast, By Rating, 2021 – 2034 (‘000 Units, USD Million)

- 8.1 Key trends

- 8.2 ≤ 250 kVA

- 8.3 >250 kVA to ≤ 1 MVA

- 8.4 > 1 MVA

Chapter 9 Market Size and Forecast, By Application, 2021 – 2034 (‘000 Units, USD Million)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial & industrial

- 9.4 Utility

Chapter 10 Market Size and Forecast, By Region, 2021 – 2034 (‘000 Units, USD million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 France

- 10.3.3 Germany

- 10.3.4 Italy

- 10.3.5 Russia

- 10.3.6 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Australia

- 10.4.3 India

- 10.4.4 Japan

- 10.4.5 South Korea

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Turkey

- 10.5.4 South Africa

- 10.5.5 Egypt

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Bharat Heavy Electricals

- 11.3 CG Power and Industrial Solutions

- 11.4 Eaton

- 11.5 Fuji Electric

- 11.6 GE

- 11.7 Hitachi Energy

- 11.8 Instrument Transformer Equipment

- 11.9 Raychem RPG

- 11.10 Schneider Electric

- 11.11 SGB SMIT

- 11.12 Siemens Energy

- 11.13 TMC Transformers

- 11.14 Toshiba Energy Systems and Solutions

- 11.15 URJA Techniques

- 11.16 WEG