|

|

市場調査レポート

商品コード

1683217

半導体レーザー市場-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Semiconductor Laser - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 半導体レーザー市場-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 188 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

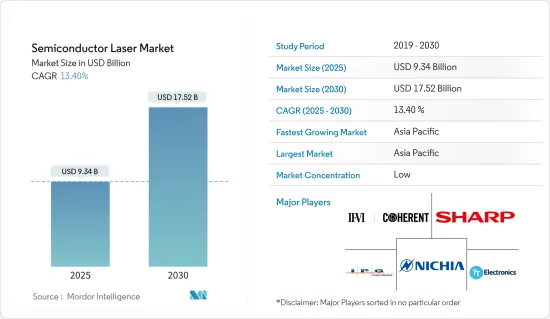

半導体レーザー市場規模は、2025年に93億4,000万米ドル、2030年には175億2,000万米ドルに達すると予測、予測期間(2025~2030年)のCAGRは13.4%。

主要ハイライト

- 半導体レーザーは、レーザーダイオードやダイオードレーザーとも呼ばれ、半導体材料を活性媒質とするレーザーの一種です。半導体pn接合ダイオードという大きな分類のサブセットです。半導体レーザーは一般的に小型で、塩の粒ほどの大きさです。半導体レーザーは、半導体利得媒質による固体レーザーであり、伝導帯のキャリア密度が高い条件下で、バンド間遷移における誘導放出によって光増幅が達成されます。

- 半導体レーザーの動作原理は、半導体材料内に形成されたpn接合への電荷キャリア(電子と正孔)の注入を伴います。レーザーダイオードを横切って順方向電気バイアスを印加すると、電荷キャリアはpn接合の反対側から空乏領域に注入されます。この電荷キャリアの注入により、より多くの電子がより低いエネルギー準位よりも高いエネルギー準位を占めるポピュレーション反転が生じます。伝導帯の電子が価電子帯の正孔と再結合すると、誘導放出によって光子が放出され、レーザー光が発生します。

- 半導体レーザーには、様々な産業で広く使用されているいくつかの利点があります。半導体レーザーは、一般的な照明技術に比べて消費電力が少なく、エネルギー効率が高いです。動作寿命が長く、長期間の使用に適しています。半導体レーザーは小型で軽量であるため、取り扱いが容易で、さまざまなシステムに統合することができます。半導体レーザーは比較的安価であるため、日常的な使用において費用対効果が高いです。また、小規模では設計が複雑に見えるかもしれないが、操作は簡単です。

- 半導体レーザー用途の需要増加の主要要因の1つは、データ転送速度に対する要求の高まりです。デジタル化とモノのインターネット(IoT)により多くのデータが作成されるため、より高速なデータ転送が必要とされています。これは、光通信製品に特化した部品メーカーにとって、大きなビジネス機会となります。

- ファイバーレーザーは、誘導放出によって高強度レーザービームを生成する固体レーザーです。レーザーは、利得媒体またはレーザー光増幅の光源として光ファイバーを利用します。ファイバーレーザーのコアは、エルビウム、ネオジム、イッテルビウムなどの希土類元素をドープした特別設計の光ファイバーで構成されています。これらのドーパントは、レーザーの動作に必要なエネルギーレベルを記載しています。ファイバーはクラッド層で囲まれており、コア内に光を閉じ込め、導く働きをします。

- 半導体レーザーの使用にとって重要な要素の一つは信頼性です。安定した出力を得るためには、一定の温度と一定の電流が必要です。電気回路の制御が欠けると、製品が誤動作し、使用されるデバイスに支障をきたす可能性があります。

半導体レーザー市場動向

通信セグメントが大きな市場シェアを占める見込み

- 半導体レーザーは、現代の通信システムにおいて重要な役割を果たしており、信頼性の高い性能で長距離の高速データ伝送を可能にしています。用途別に分類された世界の半導体レーザー市場分析では、通信産業が世界市場の大半を占めています。世界の半導体レーザー産業は、主に光通信における高い適用率によって牽引されてきました。レーザーダイオードは、ブロードバンド通信ネットワークの重要なコンポーネントへと発展してきました。

- 半導体レーザーは、長さ0.2-1mmと小型で、10-40GHzまでの直接変調が可能、低消費電力、単一波長光、1Wまでの高出力など、多様な優れた性能を持っているため、光ファイバ通信システムの標準的な光伝送器として機能します。

- 半導体レーザーは、半導体を媒質として信号を増幅する固体レーザーの一種です。最近では、光ファイバーベースの通信ネットワークが最も好まれ、すべての光リンクに半導体レーザーが内蔵されています。半導体レーザーは、急速に商業化する通信とデータ通信産業のバックボーンとして機能してきました。

- 垂直共振器面発光レーザー(VCSEL)は、データセンターや高性能コンピュータ(HPC)のマルチモード・ファイバー(MMF)をベースにした光リンクの一次光源です。通信システムにおける最近の設計では、VCSE半導体レーザーをよりエネルギー効率に優れ、高温下でも動作パラメータの調整を必要とせずに室温で高い変調ビットレートを維持できるように強化することを目指しています。

- 量子ドットのようなナノ構造半導体レーザーは、IOP Conf.Series:Materials Science and Engineeringに掲載された紙製によると、量子ドットレイザーは、通信セグメント、特に光通信において重要な役割を担っており、先端技術と高い光利得の要求に後押しされています。

- さらに、5Gと6G通信ネットワークでは、高速かつ低遅延の通信が多様なエンドポイントの相互接続を促進します。これらの重要な用途に共通する要件は、複雑なタスクを超高速で実行するレーザー光源であり、ブロードバンド、セキュア、エネルギー効率の高い通信を可能にします。各国は、5Gと6G通信の展開を促進するためにさまざまな取り組みを行っています。OpenSignalによると、プエルトリコは2023年の5G可用性ランキングで首位に立ち、5G携帯端末のユーザーは調査期間の48.4%を5Gサービスに接続して過ごすことができました。プエルトリコに続いたのは韓国とクウェートで、5Gの利用可能率はそれぞれ42.9%と39.4%でした。

大きな成長が期待されるアジア太平洋

- 日本、中国、韓国、インドなどの国々における通信産業の急激な成長が、アジア太平洋のレーザー市場を牽引すると予想されています。通信ネットワーク事業者は、都市間、都市内、FTTx、モバイルセルラーシステムなど、あらゆる通信用途用にファイバを導入しています。企業とは別に、中国政府当局も電力網、高速道路、鉄道、パイプライン、空港、データセンター、その他多くの用途をサポートするためにファイバーシステムを導入しており、これが調査対象市場の成長を後押ししています。

- AI、5G、モノのインターネット、バーチャルリアリティの急速な開発と、これらの新技術の商業的応用に伴い、データ処理と情報相互作用の需要が高まっており、この地域におけるデータセンターの建設が加速し、産業の爆発的成長につながると予想されます。

- インターネットのトラフィックが指数関数的に増大するなか、データ通信におけるエネルギー消費の削減は持続可能性にとって極めて重要です。小型でビットあたりのエネルギー消費量が少ない半導体レーザーは、短距離光相互接続のエネルギー効率達成に重要な役割を果たします。

- さらに、この地域におけるエレクトロニクス産業の隆盛と消費者向け機器の生産増加により、半導体レーザーの需要は加速しています。さらに、中国、台湾、韓国、日本などの国々には、Apple、Oneplus、Vivo、Samsungなどのスマートフォンメーカーがあり、これらの地域の半導体メーカーは、これらのメーカーの需要に応える半導体レーザーを製造しています。

- また、アジア太平洋の有利な政府イニシアティブと投資は、同地域の製造業の成長と工業化を促進し、市場の成長を後押ししています。2022年2月、インド政府は付加製造(または3Dプリンティング)の国家戦略を発表し、インドを3Dプリンティングの設計、開発、展開の世界的ハブにするため、学術界、政府、産業の協力を促しました。

- 中国は世界最大の半導体生産国のひとつであり、2035年までに半導体市場を完全に自給自足する目標を掲げているため、同国は半導体産業への投資を着実に進めています。同様に、東京都は2021年11月、台湾積体電路製造(TSMC)が熊本県に新設する鋳造工場に対する4,000億円(25億5,000万米ドル)の補助金を含む、7,740億円(49億3,000万米ドル)の半導体投資包装を承認しました。このような投資は、市場の成長に明るい展望をもたらしています。

- データセンターのトラフィックは、人工知能、機械学習、拡張現実、仮想現実などのクラウド用途の急速な採用により、急速に増加しており、イノベーションで調査された市場を牽引しています。Cloud Sceneによると、データセンターの上位市場には、中国、日本、オーストラリア、インド、シンガポールなどがあります。Clousceneによると、2023年9月現在、中国には448のデータセンターがあり、アジア太平洋のどの国・地域よりも多いです。同月の時点で、中国のデータセンター数は世界で4番目に多くなりました。

半導体レーザー市場概要

半導体レーザー市場は、Coherent Corporation、Sharp Corporation、Nichia Corporation、IPG Photonics Corporation、TT Electronicsなどの大手企業が存在し、非常にセグメント化されています。市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年11月-ROHMは、高出力レーザーダイオードRLD90QZW8を開発しました。距離計測や空間認識を必要とする産業機器や民生用途に最適。

- 2023年9月-IPG Photonics Corporationは、ミシガン州ノビで開催されたバッテリーショーで、シングルモード最高コアパワーの新しいデュアルビームレーザーの発売を発表しました。このレーザーは、バッテリー溶接のスピードと生産性をかつてないほど向上させ、スパッタのない溶接速度を、より低いコアパワーで可能な溶接速度の最大2倍まで向上させます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19とその他のマクロ経済要因が市場に与える影響

- 技術スナップショット

第5章 市場力学

- 市場促進要因

- 半導体レーザー用途の普及

- ファイバーレーザー市場の成長

- その他の光源に対する半導体レーザーの選好

- 市場課題

- 信頼性とテストの難しさ

第6章 市場セグメンテーション

- 波長別

- 赤外レーザー

- 赤色レーザー

- 緑色レーザー

- 青色レーザー

- 紫外線レーザー

- タイプ別

- EEL(端面発光レーザー)

- VCSEL(垂直共振器面発光レーザー)

- 量子カスケードレーザー

- ファイバーレーザー

- その他

- 用途別

- 通信用

- 医療

- 軍事・防衛

- 産業用

- 計測センサ

- 自動車

- その他

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- Vendor Positioning Analysis

- 企業プロファイル

- Coherent Inc

- Sharp Corporation

- Nichia Corporation

- IPG Photonics Corporation

- TT Electronics

- Sumitomo Electric Industries, Ltd.

- Sheaumann Laser, Inc.

- Newport Corporation(mks Instruments, Inc.)

- Panasonic Industry Co., Ltd

- Rohm Company Limited

- Hamamatsu Photonics K.K

- Jenoptik Laser GMBH

- TRUmpF Group

- ams OSRAM AG

- Lumentum Holdings Inc.

第8章 投資分析

第9章 市場の将来

The Semiconductor Laser Market size is estimated at USD 9.34 billion in 2025, and is expected to reach USD 17.52 billion by 2030, at a CAGR of 13.4% during the forecast period (2025-2030).

Key Highlights

- A semiconductor laser, also known as a laser diode and diode laser, is a type of laser that utilizes a semiconductor material as its active medium. It is a subset of the larger classification of semiconductor pn junction diodes. Semiconductor lasers are typically small, often about the size of a grain of salt. They are solid-state lasers based on semiconductor gain media, where optical amplification is achieved through stimulated emission at an interband transition under conditions of high carrier density in the conduction band.

- The working principle of a semiconductor laser involves the injection of charge carriers (electrons and holes) into a pn junction formed within the semiconductor material. When a forward electrical bias is applied across the laser diode, charge carriers are injected from opposite sides of the pn junction into the depletion region. This injection of charge carriers creates a population inversion, where more electrons occupy the higher energy levels than the lower energy levels. When the electrons in the conduction band recombine with holes in the valence band, they emit photons through stimulated emission, resulting in the generation of laser light.

- Semiconductor lasers offer several advantages that make them widely used in various industries. Semiconductor lasers consume less power compared to typical lighting techniques, making them more energy-efficient. They have a long operational life, making them suitable for long-term use. Semiconductor lasers are small and lightweight, making them easy to handle and integrate into different systems. Semiconductor lasers are relatively inexpensive, making them cost-effective for everyday use. They are also simple to operate, even though their design may seem complex on a small scale.

- One of the key drivers of the rise in demand for semiconductor laser applications is the rising demand for data transfer speed. As more data is created through digitalization and the internet of Things (IoT), there is a need for faster data transfers. This presents a sizeable opportunity for the component for the component manufacturers that specialize in optical communication products.

- A fiber laser is a solid-state laser that generates a high-intensity laser beam through stimulated emission. The laser utilizes an optical fiber as the gain medium or the source of laser light amplification. The core of a fiber laser consists of a specially designed optical fiber, often doped with rare-earth elements such as erbium, neodymium, or ytterbium. These dopants provide the necessary energy levels for the laser to operate. The fiber is surrounded by a cladding layer that helps confine and guide the light within the core.

- One of the crucial factors for the usage of the semiconductor laser is reliability. The products require constant temperature and constant current to ensure stable output power. Any lack of control of the electric circuit can cause the product to malfunction and hamper the device in which it is used.

Semiconductor Laser Market Trends

Communication Segment is Expected to Hold Significant Market Share

- Semiconductor lasers play a crucial role in modern communication systems, enabling high-speed data transmission over long distances with reliable performance. The communication industry dominates the global semiconductor laser market analysis categorized by applications, accounting for most of the global market. The global semiconductor laser industry has been primarily driven by the high applicability rate in optical communication. Laser diodes have evolved into an important component of broadband communication networks.

- Semiconductor lasers work as standard light transmitters in optical-fiber communication systems, owing to their small size of 0.2-1 mm length as well as their diverse excellent performances such as the capability of direct modulation up to 10-40 GHz, low-power consumption, single wavelength light, and high output power up to 1 W.

- Semiconductor lasers are a specific type of solid-state laser utilizing semiconductors as an active medium to amplify signals. Recently, fiber optics-based telecommunication networks have been the most preferred choice, with every optical link equipped with semiconductor lasers inside. Semiconductor lasers have served as the backbone for rapidly commercializing telecommunications and Datacom industries.

- Vertical-cavity surface-emitting Lasers (VCSELs) are the primary optical sources for optical links based on multimode fiber (MMF) in data centers and high-performance computers (HPCs). Recent designs in telecommunication systems aim to enhance VCSE semiconductor lasers to be more energy-efficient and capable of sustaining high modulation bit rates at room temperature without requiring adjustments to the operating parameters, even at elevated temperatures.

- Nanostructured Semiconductor lasers such as quantum dots have been highly preferred for optical telecommunication devices in recent times, as per the article published in IOP Conf. Series: Materials Science and Engineering, Quantum dot lasers play an important role in the telecommunication sector, especially in optical communication, driven by the demand for advanced technology and high optical gain.

- Moreover, in 5G and 6G telecommunication networks, swift and low-latency communications facilitate the interconnection of diverse endpoints. A common requirement in these critical applications is a laser source to execute intricate tasks at ultra-fast speeds, enabling broadband, secure, and energy-efficient communications. Countries are taking various initiatives to boost the deployment of 5G and 6G communication. According to OpenSignal, Puerto Rico led a 2023 ranking of 5G availability, with users of 5G handsets able to spend 48.4 percent of the surveyed period connected to a 5G service. Puerto Rico was followed by South Korea and Kuwait, with 5G availabilities of 42.9 and 39.4 percent, respectively.

Asia-Pacific Expected to Witness Major Growth

- The exponential growth in the communication industry in countries such as Japan, China, South Korea, and India is anticipated to drive the laser market in the Asia-Pacific region. Telecom network operators have installed fiber for all telecom applications, including inter-city, intra-city, FTTx, and mobile cellular systems. Apart from enterprises, the Chinese government authorities also install fiber systems to support the electric power grid, highways, railways, pipelines, airports, data centers, and many other applications, which drive the growth of the studied market.

- With the rapid development of AI, 5G, the Internet of Things, virtual reality, and the commercial application of these new technologies, the demand for data processing and information interaction is growing, which is expected to speed up the construction of data centers in the region and lead to the explosive growth of the industry.

- As internet traffic grows exponentially, reducing the energy consumption in data communications is crucial for sustainability. With their smaller size and lower energy consumption per bit, semiconductor lasers play a significant role in achieving energy efficiency in short-distance optical interconnects.

- Moreover, the flourishing electronics industry in this region and the increased production of consumer devices are accelerating the demand for semiconductor lasers as they are used for several manufacturing processes. Additionally, countries like China, Taiwan, Korea, and Japan are home to smartphone manufacturers such as Apple, Oneplus, Vivo, and Samsung, which makes semiconductor manufacturers around these regions produce semiconductor lasers that cater to the demands of these manufacturers.

- Also, favorable government initiatives and investments in Asia-Pacific promote the growth of the manufacturing sector and industrialization in the region, which drives the market's growth. In February 2022, the government of India released a national strategy for additive manufacturing (or 3D printing) to encourage collaboration between academia, government, and industry to make India a global hub for the design, development, and deployment of 3D printing.

- China is one of the largest producers of semiconductors in the world, and the country is making steady investments in the industry as it has set a target to become fully self-sufficient in the semiconductor market by 2035. Similarly, Tokyo approved a JPY 774 billion (USD 4.93 billion) package for semiconductor investments in November 2021, including a JPY 400 billion (USD 2.55 billion) subsidy for Taiwan Semiconductor Manufacturing Company's (TSMC) new foundry in Kumamoto prefecture. Such investments are creating a positive outlook for market growth.

- Datacenter traffic is rapidly increasing, owing to the rapid adoption of cloud applications, such as artificial intelligence, machine learning, augmented reality, and virtual reality, driving the market studied with innovations. According to Cloud Scene, some of the top markets in data centers include China, Japan, Australia, India, and Singapore. According to Clouscene, as of September 2023, there were 448 data centers in China, the most of any country or territory in the Asia-Pacific region. China had the fourth-highest number of data centers worldwide as of that month.

Semiconductor Laser Market Overview

The Semiconductor Laser market is highly fragmented, with the presence of major players like Coherent Corporation, Sharp Corporation, Nichia Corporation, IPG Photonics Corporation, and TT Electronics. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- November 2023 - ROHM developed a high-power laser diode, the RLD90QZW8. It is ideal for industrial equipment and consumer applications requiring distance measurement and spatial recognition.

- September 2023 - IPG Photonics Corporation announced the launch of a New Dual-Beam Laser with the Highest Single-Mode Core Power at The Battery Show in Novi, Michigan. It offers unprecedented speed and productivity improvements for battery welding with spatter-free welding speeds up to 2X faster than possible with lower core powers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 and Other Macroeconomic Factors on the Market

- 4.5 Tech Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Proliferation of Semiconductor Laser Applications

- 5.1.2 Growth in the Fiber Laser Market

- 5.1.3 Preference for Semiconductor Lasers Over Other Light Sources

- 5.2 Market Challenges

- 5.2.1 Difficulties Regarding Reliability and Testing

6 MARKET SEGMENTATION

- 6.1 By Wavelength

- 6.1.1 Infrared Lasers

- 6.1.2 Red Lasers

- 6.1.3 Green Lasers

- 6.1.4 Blue lasers

- 6.1.5 Ultraviolet Lasers

- 6.2 By Type

- 6.2.1 EEL (Edge-emitting Laser)

- 6.2.2 VCSEL (Vertical-cavity Surface-emitting Laser)

- 6.2.3 Quantum Cascade Laser

- 6.2.4 Fiber Laser

- 6.2.5 Other Types

- 6.3 By Application

- 6.3.1 Communication

- 6.3.2 Medical

- 6.3.3 Military and Defense

- 6.3.4 Industrial

- 6.3.5 Instrumentation and Sensor

- 6.3.6 Automotive

- 6.3.7 Other Applications

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Positioning Analysis

- 7.2 Company Profiles

- 7.2.1 Coherent Inc

- 7.2.2 Sharp Corporation

- 7.2.3 Nichia Corporation

- 7.2.4 IPG Photonics Corporation

- 7.2.5 TT Electronics

- 7.2.6 Sumitomo Electric Industries, Ltd.

- 7.2.7 Sheaumann Laser, Inc.

- 7.2.8 Newport Corporation (mks Instruments, Inc.)

- 7.2.9 Panasonic Industry Co., Ltd

- 7.2.10 Rohm Company Limited

- 7.2.11 Hamamatsu Photonics K.K

- 7.2.12 Jenoptik Laser GMBH

- 7.2.13 TRUmpF Group

- 7.2.14 ams OSRAM AG

- 7.2.15 Lumentum Holdings Inc.