|

市場調査レポート

商品コード

1850970

衛星アンテナ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Satellite Antenna - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 衛星アンテナ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月26日

発行: Mordor Intelligence

ページ情報: 英文 146 Pages

納期: 2~3営業日

|

概要

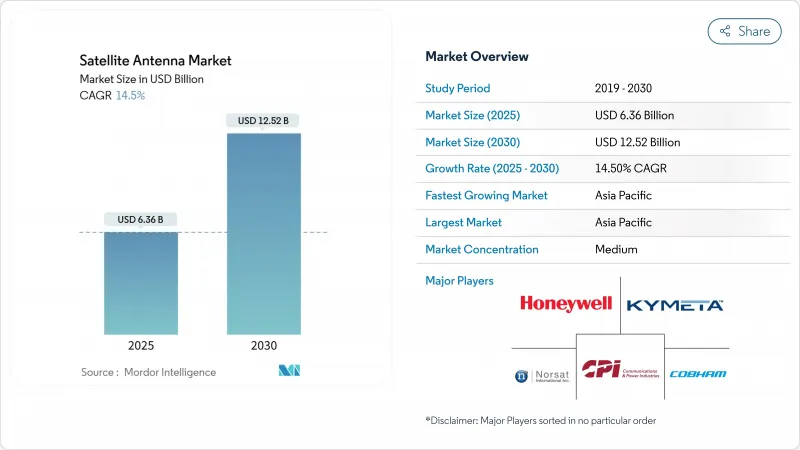

衛星アンテナ市場規模は2025年に63億6,000万米ドル、2030年には125億2,000万米ドルに達すると予測され、CAGRは14.5%と堅調です。

高スループット接続に対する旺盛な需要、マルチ軌道コンステレーションの展開、アンテナ製造コストの低下により、商業および防衛領域での採用が加速しています。ソフトウェア定義ビームステアリング、軽量複合材、高度に統合されたチップセットは、運用者の生涯所有コストを下げながら性能を向上させています。また、製品ポートフォリオを拡大する戦略的合併や、宇宙インフラをデジタル主権の柱として扱う政府によって、成長が強化されています。このような複合的な要因により、衛星アンテナ市場は、サプライヤーが規制や軌道ゴミの複雑さを乗り越えても、二桁成長を続けています。

世界の衛星アンテナ市場の動向と洞察

LEOブロードバンド衛星群の急増

スターリンク(Starlink)やワンウェブ(OneWeb)のような低軌道プロジェクトは、リンク予算の前提を塗り替え、高速で移動する衛星を1分間に何十機も追跡できる電子制御アレイの導入を事業者に促しています。2024年9月には、411のコンステレーションが登録されたが、完全に打ち上げられたのはわずか5%に過ぎず、アンテナ・サプライヤーには広大な滑走路が残されています。コンパクトなフェーズドアレイには、GNSSレシーバーとエッジコンピューティングが統合され、端末がLEO、MEO、GEOの各レイヤーでビームを自動切り替えできるようになっています。遠隔地コミュニティ、海上航路、災害対応チームは早くから恩恵を受けています。フェーズドアレイは機械部品が不要なため、生涯保守コストが下がり、大規模展開の経済的根拠が強まる。デュアル軌道端末を民生用電子機器の価格帯で大量生産できるベンダーは、衛星アンテナ市場が携帯端末のような数量に拡大するにつれて、大きな価値を獲得することになります。

宇宙の急速な軍事化(MilSATCOM)

防衛当局は、確実で妨害に強いリンクをミッション・クリティカルと見なしています。米国の2025年度予算では、宇宙ベースのシステムに252億米ドルが割り当てられており、競合する電磁環境で動作するマルチバンド、指向性アンテナの調達の引き金となっています。戦闘で実証済みの要件には、干渉を緩和するためのサイドローブ抑制、スプーフィング防止、ダイナミック・ビーム・ホッピングが含まれます。欧州とアジア太平洋における並行プログラムは、さらに需要を拡大しています。軍部はまた、小型無人偵察機や下士官兵にフィットするよう端末の軽量化を推進しており、GaNパワーアンプやコンフォーマル複合材におけるブレークスルーを後押ししています。長期的には、安全な光クロスリンクがRFを補完することになるが、短期的な支出は先進的なフェーズドアレイRFアーキテクチャに集中し、衛星アンテナ市場の勢いを維持しています。

赤道直下のKu/Kaバンド降雨フェード

豪雨はKu帯とKa帯の信号を最大20dB減衰させるため、事業者はリンクマージンをオーバーサイズするか、より低い周波数に戻すことを余儀なくされます。インドネシアとブラジルの熱帯性マイクロバーストは、企業やバックホール顧客のSLAを損なう予測不可能なフェードを引き起こします。緩和策としては、アダプティブ・コーディング、サイト・ダイバシティ、暴風雨時にCバンドにフォールバックするデュアルバンド端末などがあるが、これらのソリューションはサービス・プロバイダーにとって設備投資と固定資産税(OPEX)を引き上げることになります。将来的な気候変動が不確定要素になるため、通信事業者の中には、容量面で有利であるにもかかわらず、Ka帯中心のネットワークに消極的なところもあります。その結果、赤道直下の地域での採用動向は、世界の衛星アンテナ市場の動向に遅れる可能性があります。

セグメント分析

Kuバンドは、成熟した地上インフラとバランスの取れたレインフェード耐性を活かし、2024年の衛星アンテナ市場の29%を占めました。同セグメントは、放送やVSATサービスの中心であり続け、特に規制上の認可が既に存在するところでの利用が多いです。これとは対照的に、Ka帯域はCAGR 15.2%で急拡大しており、ビット当たりの低コストと柔軟なスポットビームアーキテクチャを求めるブロードバンド事業者を惹きつけています。この成長軌道は、NASAの地球観測コンステレーションにおける26 Tb/日のルーティング要件に支えられ、Ka端末の衛星アンテナ市場規模が拡大することを意味します。Cバンドはサイクロンが発生しやすい地域で重要性を維持し、Xバンドは干渉耐性により防衛ニッチであり続ける。新興のマルチバンドアンテナは従来のサイロを曖昧にし、リアルタイムの周波数切り替えを可能にします。この機能はシステム全体の可用性を高め、衛星アンテナ市場においてサプライヤーが対応可能な収益源を広げます。

マルチビーム・フラットパネル設計は、KuとKaの同時接続を可能にし、雨によるフェード時にトラフィックを反転させることができます。プログラマブルRFフロントエンドを統合するサプライヤーは、必要なところに動的に電力を割り当て、スペクトル効率を高めることができます。これらの進歩は、モバイルVSAT、クルーズ、石油・ガスプラットフォームなどの価値提案を変革します。そのため、高周波数端末の衛星アンテナ市場規模は2030年までに倍増すると予測されるが、熱帯地域の需要をフルに引き出すためには、サプライヤーは天候に適応したインテリジェンスを組み込む必要があります。

パラボラアンテナは2024年に衛星アンテナ市場規模の38%を占め、ドルあたりの利得が高い静的ゲートウェイに好まれます。機械式ジンバルは、大型クルーズ船やテレポート・ハブでは依然として費用対効果が高いです。しかし、CAGR18.4%で拡大するフラットパネル電子制御アレイは、モビリティの使用事例を再定義しつつあります。Anokiwaveを搭載したパネルは現在、工場で校正され、設置時間を短縮し、ナローボディ航空機のコンフォーマル胴体への取り付けをサポートしています。試作中のインフレータブル・ディッシュは、20:1のパッキング効率を約束し、打ち上げ質量に敏感な小型衛星に対応します。

小型のパラボラ・セグメントと位相シフター・サブアレイを組み合わせたハイブリッド・アーキテクチャは、ディッシュの高利得の利点とESAの俊敏性を引き出します。フレキシブルな誘電体材料を研究しているベンダーは、アンテナを車両ルーフの周囲に曲げることができ、空気抵抗によるペナルティをなくすことができます。その結果、対応可能な衛星アンテナ市場は、超薄型端末を必要とするパーソナル・ビークル、電車、都市型ドローン・タクシーにまで拡大します。リフレクターの既存企業は、インストールされた基盤を保護するために、自動ポインティングとヘルス・モニタリング・ファームウェアを組み込むことで対応し、2030年まで、完全な置き換えではなく、共存のシナリオを示します。

衛星アンテナ市場レポートは、周波数帯(Cバンド、Xバンド、Kuバンド、その他)、アンテナタイプ(パラボラアンテナ、ホーン型アンテナ、FRPレドーム型アンテナ、その他)、アプリケーション(スペースボーン、エアボーン、その他)、エンドユーザー(民間および政府、防衛)、地域別に分類されています。

地域分析

アジア太平洋地域は、中国、インド、日本、韓国がマルチオービットシステムと国産製造の規模を拡大するにつれて、2030年までのCAGRが14.6%となり、最も急速な拡大を記録します。2024年2月に開設される中国第5の南極前哨基地は、科学と防衛の両分野で使用される衛星アンテナを展示します。インドの「Make in India」政策に沿った生産連動型インセンティブは、フィードホーン、レドーム、RFICサブシステムの現地生産を促進し、地域の事業者のコストを引き下げます。日本の自動車業界は、地上波以外のバックホールを利用したコネクテッドカー・サービスの準備を進めており、サプライヤーは屋上統合用のアンテナの小型化を促しています。

北米は、深い航空宇宙サプライチェーン、多額の国防支出、起業家精神にあふれた宇宙ベンチャーのおかげで、依然として最大の衛星アンテナ市場です。米国宇宙軍は衛星管制ネットワークを維持し、19基のアンテナを75%の稼働率で運用しており、2025年からは新たに12基の大容量アンテナを計画中です。カナダの極地通信プログラムは、低温耐性のあるアンテナの需要を増やしています。メキシコとその他のラテン諸国は、設備投資の圧力により当面の規模は抑制されるもの、インターネット・コミュニティWi-Fi用にGEOゲートウェイを活用しています。

欧州は堅調なシェアを維持しており、軍事や気候監視のミッションをサポートするAMPERプロジェクトの形状メッシュ反射器など、ESAの技術実証によって強化されています。ドイツと英国はデータの自律性を確保するためにソブリン・テレポートに資金を提供し、モバイル・ネットワーク事業者はスコットランドとバイエルン州の地方で衛星経由のバックホールをテストしています。東欧の通信事業者は、為替変動に打ち勝つためにリース・トゥ・オーウン・モデルを採用し、アンテナ・サプライヤーへの発注パイプラインをスムーズにする戦術をとっています。中東では、GCCの政府系ファンドがGEO VHTSプロジェクトを支援しており、サウジアラビアのロードマップでは、2030年までに国の宇宙収入が3倍になるとしています。南米は後塵を拝しているが、石油・ガスのオフショア接続で二重冗長アンテナが義務付けられているブラジルに成長の兆しが見られます。これらの力学を総合すると、衛星アンテナ市場内では地域的な需要の分散が保たれ、マクロ的なショックから世界的な収益を守ることができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- LEOブロードバンド衛星群の普及

- 宇宙の急速な軍事化(MilSATCOM)

- 高スループット衛星(HTS)ペイロードの採用

- 商用機内接続(IFC)のブーム

- ESAベースのフラットパネルコスト曲線デフレーション(UNDER-RADAR)

- 月および近月ミッションの通信需要(UNDER-RADAR)

- 市場抑制要因

- 赤道地域におけるKu/Kaバンド降雨減衰

- フェーズドアレイチップセットの輸出管理のボトルネック

- 軌道デブリ保険料の高騰(UNDER-RADAR)

- 新興市場の通信事業者の設備投資危機(注目されていない)

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 周波数帯域別

- Cバンド

- Xバンド

- Kuバンド

- Kaバンド

- L/Sバンド

- VHF/UHFバンド

- アンテナタイプ別

- パラボラ反射鏡

- フラットパネル(ESA/RSA)

- ホーン

- 誘電体共振器

- FRPレドーム

- 金属刻印

- 用途別

- 宇宙船

- 空挺

- 海事

- 陸上(移動式および固定式)

- エンドユーザー別

- 商業用

- 政府と防衛

- 地域別

- 北米

- 米国

- カナダ

- 南米

- ブラジル

- アルゼンチン

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州地域

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC諸国

- トルコ

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Honeywell International Inc.

- CPI International Inc.

- Kymeta Corp.

- Norsat International Inc.

- Cobham SATCOM

- L3Harris Technologies Inc.

- Viasat Inc.

- Airbus Defence and Space

- Gilat Satellite Networks Ltd.

- Maxar Technologies

- Ball Aerospace

- Intellian Technologies

- Isotropic Systems(All.Space)

- Hanwha Phasor

- SES S.A.(O3b mPOWER User Terminals)

- Thales Alenia Space

- MT Mechatronics

- SatixFy Ltd.

- General Dynamics Mission Systems

- LEOcloud Inc.

- Hughes Network Systems