|

市場調査レポート

商品コード

1549958

欧州・中東・アフリカの衛星アンテナ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)EMEA Satellite Antenna - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州・中東・アフリカの衛星アンテナ:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

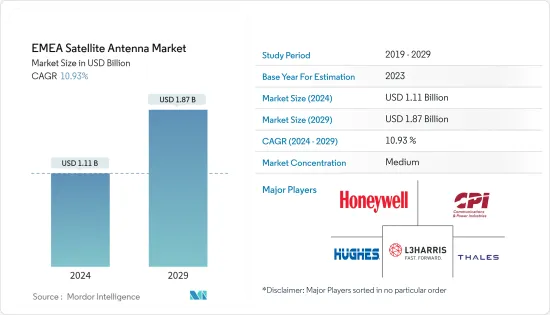

欧州・中東・アフリカの衛星アンテナの市場規模は、2024年に11億1,000万米ドルと推定され、2029年には18億7,000万米ドルに達し、予測期間中(2024年~2029年)にCAGR10.93%で成長すると予測されます。

主なハイライト

- 欧州・中東・アフリカの衛星アンテナ市場は、高速ワイヤレス接続の需要拡大に牽引され、大きな成長を遂げています。この需要は、5Gの展開と6Gネットワークの期待によって大幅に増加しています。5G衛星通信はモバイルブロードバンドサービスの向上をサポートします。この技術は、自律走行車、重要インフラの遠隔制御などの用途に低遅延と中断のないネットワークの可用性を提供するミッションクリティカルな通信に使用されます。

- 同市場は、フラットパネル、相互運用性、モバイル通信などの進歩を目の当たりにしています。航空宇宙・防衛分野での電子制御アンテナ(ESA)採用の増加は、業界参加者に有利な成長の道を示しています。2024年3月、英国の衛星通信会社Hanwha Phasorは、移動体通信用の次期Phasor L3300B陸上アンテナを発表しました。Phasor L3300Bは、アクティブ電子制御アンテナ(AESA)で、商業および軍事用途向けに調整されています。このアンテナの主な特長は、同時に2つの受信チャンネルを使用できるため、シームレスな通信を維持できることです。これにより、アンテナは現在のリンクを中断することなく、新しい衛星との接続を確立することができます。

- 欧州委員会と欧州ICT業界の共同イニシアチブである5Gインフラ官民パートナーシップ(PPP)によると、欧州は2023年に5Gの旅の半ばを迎えました。5Gの普及率は72%に達しましたが、この数字にはスタンドアロン以外の展開も含まれていることに注意する必要があります。しかし、特に産業環境における5Gの本格的な商用導入はまだ先であり、大きな収益の可能性が約束されています。

- GSMAのレポート2024によると、主にアフリカ(特にエチオピアやガーナ)のような新興国市場で、多くの新しい5G市場がネットワークを開始する予定です。さらに、サハラ以南のアフリカにおける5Gの普及率は、2023年には1%未満でしたが、2030年には17%、2億3,400万接続を目指すと予測されています。

- 同市場は、フェーズドアレイアンテナや電子制御アンテナのコスト高という課題に直面しており、さらに規制上のハードルがアンテナの成長を制限しています。規制基準を満たし、ライセンシングを取得することは、メーカー、特に多様な規制状況下で事業を展開する企業にとって課題となります。これらの規格を遵守することは、複雑さを増すだけでなく、アンテナメーカーのコストを増加させます。

- パンデミックはリモートワークやハイブリッドワークへのシフトを加速させ、遠隔地からでも仕事を管理できる信頼性の高いインターネット接続の必要性を増幅させました。さらに、堅牢な通信ネットワークを必要とする遠隔医療サービスの台頭は、衛星技術によって十分に支えられています。

欧州・中東・アフリカの衛星アンテナ市場動向

フラットパネルアンテナが最も高いCAGRで推移する見込み

- コンパクトなサイズと高度な技術により、欧州・中東・アフリカではフラットパネルアンテナの需要が高まっています。フラットパネルアンテナは、船舶やオフショアプラットフォームに高速インターネットや通信サービスを提供するための海洋接続に使用されています。これらのアンテナはコンパクトで、動きや過酷な海洋環境の影響を受けにくいため、信頼性の高い接続が保証されます。

- 欧州の軍事作戦では、通信、指揮、制御の必要性から、衛星通信(SatCom)や通信・情報システム・サービス(CIS)への依存度が高まっています。これらのサービスは、EUの指揮官と遠隔地の部隊との接続を容易にし、効率的な任務とタスクの管理を可能にします。フラットパネルアンテナは、戦術作戦に不可欠な安全で広帯域の通信を保証する極めて重要なものです。

- NATOによると、EU諸国では過去10年間に軍事費が46%増加しており、これは国民所得の4倍の速さです。ドイツ、イタリア、スペインのような国々では、軍事能力の強化、新技術の採用、軍事関連インフラの強化のための資源配分が増加しています。

- 多くの市場関係者は、衛星軍事通信を改善するソリューションの開発に投資しています。例えば、ベルギー国防省は2023年1月、戦術衛星通信サービスに関するエアバスとの15年契約を発表しました。この契約により、同国軍はエアバスのUHF(超高周波)軍事通信チャンネルを活用することになり、この通信チャンネルはエアバスが製作した商用通信衛星に搭載されるペイロードの一部となります。

- フラットパネルアンテナは、インターネット接続を地方やサービスが行き届いていない地域にまで拡大することを可能にします。インフラが整備されていない地域でもブロードバンドアクセスを提供できます。アフリカでは多くのNGOや政府当局が、遠隔地の村や学校にインターネットサービスを提供するためにフラットパネルアンテナを導入しています。また、欧州・中東・アフリカで活動するメディア企業もフラットパネルアンテナを活用することで、重要なニュースイベントやスポーツイベント、屋外プロダクションの特集など、遠隔地からのライブ放送を効率的に行うことができます。

- 衛星フラットパネルアンテナは、地理的な障害を克服する能力で際立っており、従来のインフラでは実現不可能であったり、コストがかかりすぎたりするような遠隔地や厳しい環境でも、信頼性の高い接続を保証します。これらのアンテナは、田園地帯、海洋プラットフォーム、災害被災地など、地上からの電波がほとんど届かない地域のコミュニティや産業にとって重要なリンクとして衛星通信を活用しています。

ドイツが最大の市場シェアを占める

- ドイツには強力な航空宇宙産業と衛星通信産業があります。同国は複数のメーカー、サービスプロバイダー、テクノロジー企業によって支えられています。これは、通信、放送、防衛、調査などさまざまな分野で衛星通信サービスの需要が増加していることが主な要因です。

- ドイツではブロードバンド通信の需要が伸びています。この需要により、航空機、船舶、車両(救急隊員を含む)のユーザー間の接続ニーズが高まっています。これらのプラットフォームでは、移動中も途切れることのない接続が必要であり、多くの場合、大都市や人口の少ない地域内のサービスが行き届いていない地域を横断します。こうした動向は、市場の成長見通しを後押しするものと期待されます。

- ドイツの企業は、自社のサービスを強化するために、ますます最新のソリューションに目を向けるようになっています。例えば2023年7月、超高解像度(VHR)衛星画像を提供する欧州のEuropean Space Imaging(EUSI)は、ミュンヘン近郊のドイツ航空宇宙センター(DLR)の地上局に大規模な投資を行いました。このアップグレードは、EUSIの画像配信スピードと効率を向上させただけでなく、欧州における衛星画像技術のリーディングプロバイダーとしての評判を確固たるものにしました。

- Die Medienanstalten(ドイツのメディア企業)によると、ドイツでは引き続きDTH衛星とケーブルテレビが主なテレビ受信方法となっています。DTH衛星テレビサービスは1,640万世帯で利用されており、全テレビ世帯の42%を占めていますが、2022年の43%からわずかに減少しています。ケーブルテレビの加入世帯は1,590万世帯で、普及率は41%(2022年:43%)に相当し、同国の衛星アンテナ市場を牽引しています。

- さらに、HughesNet、Viasatなどの企業や、Starlinkのような新興のLEO衛星プロバイダーが衛星経由でインターネットサービスを提供しており、遠隔地でのOTTコンテンツのストリーミングを可能にしています。データによると、インターネット経由のテレビ受信(OTT)は、2023年には310万世帯が選択し、2022年と比較して世帯の6%から8%に増加しました。

- ドイツの軍隊である連邦軍は、独立した多衛星通信システムの計画を発表しました。2023年11月9日、ドイツのボリス・ピストリウス国防相は、安全保障政策の成熟の必要性を強調しました。単独システムに加え、ドイツは、特にLEO(地球低軌道)サービスを活用し、EUの今後のIRIS2(衛星による回復力、相互接続、セキュリティのためのインフラストラクチャー)衛星通信コンステレーションと軍事的ニーズを合わせることを目指しています。

欧州・中東・アフリカの衛星アンテナ産業の概要

欧州・中東・アフリカの衛星アンテナ市場は適度に断片化されており、数十年の経験を持つ国内外の企業が存在します。ベンダーは専門知識を活用することで強力な競合戦略を取り入れています。全体として競争企業間の敵対関係は激しく、予測期間中もそれは変わらないと予想されます。

2024年4月:EchoStarの子会社であるHughes Network Systems, LLC(HUGHES)は、Hughes HL1120Wターミナルを発表しました。この端末は電子操縦アンテナ(ESA)技術に基づき、ユーテルサットOneWebの地球低軌道(LEO)衛星ネットワークの運用承認を得ました。この承認はヒューズにとって重要な成果であり、ユーテルサット・ワンウェブの最高レベルの高速接続を世界中の顧客に拡大することを可能にしました。

2024年1月:ユーテルサット・グループの一部門であり、総合GEO-LEO衛星オペレータであるユーテルサット・ワンウェブは、デジタルトランスフォーメーションの主要企業であるSTCグループとともに、サウジアラビアのタブーク地上局から商業サービスを開始するための最終準備を進めていることを発表しました。タブークに位置するこの地上局は、サウジアラビアの著名な建設会社Albabtain LeBlancと共同で開発され、15基の先進的な衛星追尾アンテナシステムを誇ります。この地上局は、特に中東におけるユーテルサットOneWebの低軌道(LEO)接続サービスにおいて、通信サービスを大幅に強化する態勢を整えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 主要マクロ経済動向の影響評価

第5章 市場力学

- 市場促進要因

- 高速コネクティビティの需要増加

- 5G、AI、エッジコミューティングの技術進歩

- 衛星ベースのサービスに対する需要の高まり

- 市場抑制要因

- 衛星アンテナを支えるインフラ整備の高コスト

第6章 市場セグメンテーション

- アンテナタイプ別

- フラットパネルアンテナ

- パラボラアンテナ

- ホーンアンテナ

- ガラス繊維強化プラスチックアンテナ

- 鉄製モールドアンテナ

- その他のアンテナタイプ

- 用途別

- 宇宙

- 陸上

- 海上

- 航空

- 国別

- 英国

- ドイツ

- フランス

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第7章 競合情勢

- 企業プロファイル

- Honeywell International Inc.

- Communications & Power Industries(CPI)International Inc.

- L3harris Technologies Inc.

- Thales Group

- Hughes Network Systems LLC

- Airbus

- General Dynamics Corporation

- COBHAM PLC

- Viasat Inc.

- Mitsubishi Electric Corporation

第8章 投資分析

第9章 市場機会と今後の動向

The EMEA Satellite Antenna Market size is estimated at USD 1.11 billion in 2024, and is expected to reach USD 1.87 billion by 2029, growing at a CAGR of 10.93% during the forecast period (2024-2029).

Key Highlights

- The EMEA satellite antenna market is experiencing significant growth, driven by the growing demand for high-speed wireless connectivity. This demand is significantly increasing with the deployment of 5G and the anticipation of 6G networks. 5G satellite communication supports improving mobile broadband services. This technology is used in mission-critical communications that provide low latency and uninterrupted network availability for applications like autonomous vehicles, remote control of critical infrastructure, etc.

- The market is witnessing advancements like flat panels, interoperable, and mobile communication. The rising adoption of electronically steered antennas (ESA) in aerospace and defense presents lucrative growth avenues for industry participants. In March 2024, Hanwha Phasor, a UK-based satellite communications company, announced the upcoming Phasor L3300B land antenna for mobile communications. The Phasor L3300B, an active electronically steered antenna (AESA), is tailored for commercial and military applications. Its main feature is maintaining seamless communication since it facilitates dual simultaneous receive channels. This allows the antenna to establish connections with new satellites without interrupting its current link.

- According to the 5G Infrastructure Public Private Partnership (PPP), a joint initiative by the European Commission and the European ICT Industry, Europe was midway through its 5G journey in 2023. While 5G coverage reached 72% penetration, it is important to note that this figure includes non-standalone deployments. However, the full-scale commercial implementation of 5G, especially in industrial settings, is still on the horizon, promising significant revenue potential.

- As per the GSMA report 2024, many new 5G markets, primarily in developing regions such as Africa (highlighting Ethiopia and Ghana), are set to launch their networks. Moreover, 5G adoption in sub-Saharan Africa was under 1% in 2023; projections indicate a substantial rise, aiming for 17%, catering to 234 million connections by 2030.

- The market faces challenges from the high costs of phased array and electronically steered antennas, alongside regulatory hurdles limiting antenna growth. Meeting regulatory standards and obtaining licenses poses a challenge for manufacturers, particularly for companies operating across diverse regulatory landscapes. Adhering to these standards not only adds complexity but also increases costs for antenna manufacturers.

- The pandemic accelerated the shift toward remote and hybrid work, amplifying the need for reliable internet connectivity for managing work even from remote areas. Additionally, the rise of telehealth services that require robust communication networks is well supported by satellite technologies.

EMEA Satellite Antenna Market Trends

The Segment for Flat-panel Antennas is Expected to Witness the Highest CAGR

- Due to their compact size and advanced technology, there is a growing demand for flat-panel antennas in the EMEA region. They are used in marine connectivity to facilitate high-speed Internet and communication service to ships and offshore platforms. These antennas are compact and less susceptible to motion and harsh maritime environments, which ensures reliable connectivity.

- Europe's military operations increasingly rely on satellite communications (SatCom) and communication and information system services (CIS) for their communication, command, and control needs. These services facilitate the connection of EU commanders with forces in remote regions, allowing efficient mission and task management. Flat-panel antennas are pivotal, ensuring secure, high-bandwidth communications vital for tactical operations.

- According to NATO, military expenditures increased by 46% in EU countries during the last 10 years, four times faster than national income. Countries like Germany, Italy, and Spain witnessed increased allocation of resources to bolster their military capabilities, embrace new technologies, and enhance military-related infrastructures.

- Many market players are investing in developing solutions for improving satellite military communication. For instance, in January 2023, the Belgian Ministry of Defence announced a 15-year deal with Airbus for tactical satellite communication services. Under this agreement, the Armed Forces will leverage Airbus's UHF (Ultra High Frequency) military communication channels, which are part of a payload hosted on a commercial telecommunications satellite crafted by Airbus.

- Flat panel antennas allow extending internet connectivity to rural and underserved areas. They can provide broadband access in areas that do not support infrastructures. Many NGOs and government authorities in Africa are deploying flat panel antennas to deliver internet services to remote villages and schools. They also facilitate media companies operating in the EMEA region to take advantage of flat panel antennas, which allow live broadcasting from remote locations, such as featuring crucial news events, sports events, or outdoor productions efficiently.

- Satellite flat-panel antennas stand out for their capacity to surmount geographical obstacles, ensuring dependable connectivity in remote or demanding settings where conventional infrastructure proves unfeasible or too costly. These antennas leverage satellite communications as a crucial link for communities and industries in locales with scant terrestrial coverage, including rural zones, offshore platforms, and disaster-affected regions.

Germany Holds the Largest Market Share

- Germany has a strong aerospace and satellite communication industry. The country is supported by several manufacturers, service providers, and technology companies. This is majorly driven by the increasing demand for satellite communication services across various sectors, which include telecommunication, broadcasting, defense, and research.

- The demand for broadband communications is growing in Germany. This demand drives the need for connectivity among users on aircraft, ships, and vehicles, including first responders. These platforms necessitate uninterrupted connectivity throughout their journeys, often traversing underserved areas within major cities and sparsely populated regions. These trends are expected to bolster the market's growth prospects.

- German companies are increasingly turning to modern solutions to enhance their offerings. For instance, in July 2023, European Space Imaging (EUSI), Europe's provider of Very High Resolution (VHR) satellite imagery, made a significant investment in its ground station at the German Aerospace Center (DLR) near Munich. This upgrade not only enhanced EUSI's image delivery speed and efficiency but also cemented its reputation as a leading provider of satellite imagery technology in Europe.

- According to Die Medienanstalten (German Media company), DTH satellite and cable TV continue to be the primary TV reception methods in Germany. DTH satellite TV service is consumed by 16.4 million households, accounting for 42% of all TV households, a marginal decrease from 43% in 2022. A cable TV subscription was used by 15.9 million households, corresponding to 41% penetration (2022: 43%), propelling the market for satellite antennas in the country.

- Additionally, companies such as HughesNet, Viasat, and other emerging LEO satellite providers like Starlink offer internet services via satellite, enabling streaming of OTT content in remote areas. As per data, TV reception via the Internet (OTT) was opted by 3.1 million households in 2023, an increase from 6% to 8% of households compared to 2022.

- Germany's Bundeswehr, the country's armed forces, announced plans for an independent multi-satellite communications system. On November 9, 2023, German Defense Minister Boris Pistorius emphasized the nation's need to mature in its security policies. In addition to its standalone system, Germany aims to align its military needs with the EU's upcoming IRIS2 (Infrastructure for Resilience, Interconnection & Security by Satellites) satcom constellation, particularly leveraging its LEO (low-Earth orbit) services.

EMEA Satellite Antenna Industry Overview

The EMEA satellite antenna market is moderately fragmented, with local and international players having decades of experience. The vendors are incorporating a powerful competitive strategy by leveraging their expertise. Overall, the intensity of the competitive rivalry is high in the market, and it is expected to remain the same over the forecast period.

April 2024: Hughes Network Systems, LLC (HUGHES), a subsidiary of EchoStar, unveiled the Hughes HL1120W Terminal. Based on the electronically steerable antenna (ESA) technology, this terminal secured operational approval from Eutelsat OneWeb for its low Earth orbit (LEO) satellite network. This endorsement marked a significant achievement for Hughes, empowering the company to extend Eutelsat OneWeb's top-tier, high-speed connectivity to a global clientele.

January 2024: Eutelsat OneWeb, a division of the Eutelsat Group and integrated GEO-LEO satellite operator, along with STC Group, a key player in digital transformation, announced their final preparations for launching commercial services from their Tabuk ground station in Saudi Arabia. This ground station, situated in Tabuk and developed in collaboration with Albabtain LeBlanc, a prominent Saudi Arabian construction firm, boasts 15 advanced satellite tracking antenna systems. It is poised to significantly enhance communication services, particularly for Eutelsat OneWeb's low-Earth orbit (LEO) connectivity offerings in the Middle East.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 An Assessment of the Impact of Key Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand of High-Speed Connectivity

- 5.1.2 Technology Advancement in 5G, AI and Edge Commuting

- 5.1.3 Growing Demand for Satellite-Based-Services

- 5.2 Market Restraints

- 5.2.1 High Cost of Development of Infrastructure to Support Satellite Antennas

6 MARKET SEGMENTATION

- 6.1 By Antenna Type

- 6.1.1 Flat Panel Antenna

- 6.1.2 Parabolic Reflector Antenna

- 6.1.3 Horn Antenna

- 6.1.4 Fiberglass Reinforced Plastic Antenna

- 6.1.5 Iron Antenna With Mold Stamping

- 6.1.6 Other Antenna Types

- 6.2 By Application

- 6.2.1 Space

- 6.2.2 Land

- 6.2.3 Maritime

- 6.2.4 Airborne

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Saudi Arabia

- 6.3.5 UAE

- 6.3.6 South Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Honeywell International Inc.

- 7.1.2 Communications & Power Industries (CPI) International Inc.

- 7.1.3 L3harris Technologies Inc.

- 7.1.4 Thales Group

- 7.1.5 Hughes Network Systems LLC

- 7.1.6 Airbus

- 7.1.7 General Dynamics Corporation

- 7.1.8 COBHAM PLC

- 7.1.9 Viasat Inc.

- 7.1.10 Mitsubishi Electric Corporation