|

市場調査レポート

商品コード

1683190

南米のチョコレート市場:市場シェア分析、産業動向、成長予測(2025~2030年)South America Chocolate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米のチョコレート市場:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 166 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

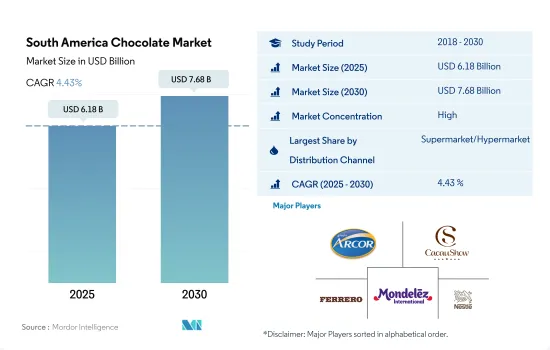

南米のチョコレート市場規模は2025年に61億8,000万米ドルと推定・予測され、2030年には76億8,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは4.43%で成長すると予測されます。

スーパーマーケットとコンビニエンスストアは引き続き多くの消費者を魅了し、2024年の金額シェアは約75%に達すると予想されます。

- 南米のチョコレート市場では、スーパーマーケットとハイパーマーケットが最大の小売チャネルです。都市化の進展とスマートシティ開発施策の増加が、この地域におけるスーパーマーケットとハイパーマーケットの拡大を促進しています。ダークチョコレートに比べ、ミルクチョコレートとホワイトチョコレートが最大のシェアを占めており、2023年の市場数量シェアは65.3%です。

- スーパーマーケットにおけるチョコレートの販売額は、この地域で2023~2029年の間にCAGR 4.21%を記録すると予測されています。これは主に、これらの流通チャネルが提供する複数の利点によるものです。スーパーマーケットやハイパーマーケットでの買い物は通常、小規模店舗での買い物よりも迅速で簡単です。スーパーマーケットはスペースが広いため、消費者がさまざまなチョコレートを購入しやすいです。

- コンビニエンスストアは、南米でチョコレートを購入する際に2番目に好まれる流通チャネルです。コンビニエンスストアは、住宅地や商業地域の近くにあるため非常に近づきやすく、一般的に手頃な価格のチョコレートを提供しています。コンビニエンスストアを通じたチョコレートの販売額は、2020~2023年にかけて8.3%の成長率を記録しました。

- オンラインチャネルは、この地域でチョコレートが消費される流通チャネルとして急成長しています。この流通セグメントは、2024~2027年にかけて金額ベースで16.1%の成長を記録すると予測されています。チョコレート購入を含む飲食品におけるオンライン小売チャネルの役割の進化は、インターネット利用者の増加に影響されています。2022年には、ブラジルの3,800万人の買い物客がチョコレートを含む商品やサービスを購入するためにオンラインショッピングを利用しました。また、ブラジルのオンライン購入者の42%が、迅速な配送を提供するアプリを通じたショッピングを好んでいます。

贅沢な間食行動とブラジルとその他の南米の需要が、2023年にほぼ90%の金額シェアを記録し、地域市場を牽引する

- ブラジルが同地域の主要市場であり、アルゼンチンがこれに続きます。便利で嗜好性の高い間食に対する消費者の嗜好の高まりが、同地域の主要な市場促進要因となっています。2023年現在、ブラジルの16~34歳の消費者の39%がリラックス/ストレス解消のために間食をとっています。また、35歳以上の消費者の32%が、スナックを食べることで不安に対処できると考えています。

- ブラジルでは、チョコレートが最も広く消費されている菓子類であり、2023年の菓子類市場全体の数量シェアは50.02%です。ブラジルの消費者は、チョコレートをその風味からユニークで欠かせない嗜好品として認識しています。2022年には、消費者の67%が週に1回以上チョコレートを消費しています。チョコレート製品の中では、ダークチョコレートが同国で最も急成長しているセグメントであり、2023~2030年の金額ベースのCAGRは6.44%と予想されます。この市場の成長は、消費者が罪悪感のない嗜好品へとシフトしていることに起因しています。2022年には、消費者の81%が健康上のニーズに合わせてカスタマイズ型スナックを好むようになりました。

- アルゼンチンは南米で最も急成長している菓子類市場です。アルゼンチン市場は予測期間中、金額ベースで5.83%のCAGRで推移すると予測されています。アルゼンチンは世界有数の間食大国であり、間食は通常の食事時間と並んで1日のうち何度も行われます。2023年の1人当たり年間チョコレート消費量は1.6kgでした。

- その他の南米では、チリとペルーが成長を牽引する主要国で、2023年には合計で数量の60%以上を占めます。ダークチョコレートだけでなくミルクチョコレートの消費量が増加しているのは、主に消費者の間でギフト文化が高まっていることに加え、若年層や成人層の間でチョコレートの国内消費が増加しているためです。

南米のチョコレート市場動向

原料や包装の差別化に支えられた衝動買いが市場成長に重要な役割を果たす

- 南米では、チョコレートの消費はブラジルが他地域に比べて突出しています。チョコレートは依然として同国で最も消費されている菓子類です。2022年には、ブラジル人口の75%がチョコレートを消費し、ブラジル人の35%が他の飲食物よりもチョコレートを定期的に消費しています。

- この地域では、包装と原料がチョコレートの衝動買いに影響を与えています。チョコレートの包装と原料に関しては、消費者にとって持続可能性がますます重要な要素となっています。2023年時点で、ブラジルの消費者の40%が、チョコレートを含むスナック菓子のサステイナブル包装を好みます。

- 南米の消費者はプレミアムチョコレート製品への関心を高めています。ブラジルでは、2023年時点で、76%の消費者がオーガニックチョコレートやヴィーガン・チョコレートを含む高品質/プレミアムスナックに高いお金を払うことを望んでいます。

- 低糖質または低カロリーのスナック食品に対する消費者の志向の高まりは、予測期間中にチョコレートのヘルシーバリエーションに有利な機会を生み出すと推定されます。2021年には、「砂糖ゼロ」(46%)と「ライト」(55%)が、ブラジルの無糖食品と減糖食品でそれぞれ最も一般的な糖質表示でした。

南米のチョコレート産業概要

南米のチョコレート市場はかなり統合されており、上位5社で92.12%を占めています。この市場の主要企業は、Arcor S.A.I.C, Cacau Show、Ferrero International SA、Mondelez International Inc.、Nestle SAです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 規制の枠組み

- 消費者の購買行動

- 成分分析

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 菓子類

- ダークチョコレート

- ミルクチョコレートとホワイトチョコレート

- 流通チャネル

- コンビニエンスストア

- オンラインストア

- スーパーマーケット/ハイパーマーケット

- その他

- 国名

- アルゼンチン

- ブラジル

- その他の南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Arcor S.A.I.C

- Cacau Show

- Chocoladefabriken Lindt & Sprungli AG

- Confiteca CA

- Ferrero International SA

- Grupo de Inversiones Suramericana SA

- Mars Incorporated

- Mondelez International Inc.

- Nestle SA

- Nugali Chocolates

- The Hershey Company

- The Peccin SA

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 61579

The South America Chocolate Market size is estimated at 6.18 billion USD in 2025, and is expected to reach 7.68 billion USD by 2030, growing at a CAGR of 4.43% during the forecast period (2025-2030).

Supermarkets and convenience stores expected to continue to captivate a larger consumer base, with a value share of almost 75% in 2024

- Supermarkets and hypermarkets are the largest retail channels in the South American chocolate market. The rising urbanization and increasing smart city development policies are promoting the expansion of supermarkets and hypermarkets in the region. Compared to dark chocolate, milk and white chocolate accounted for the largest share, with a market volume share of 65.3% in 2023.

- The sales value of chocolates in supermarkets is anticipated to register a CAGR of 4.21% during 2023-2029 in the region. This is mainly attributed to the multiple benefits offered by these distribution channels. Shopping at supermarkets and hypermarkets is typically a quicker and easier experience than shopping at a smaller store. Supermarkets have larger spaces, making it easy for consumers to buy a range of chocolates.

- Convenience stores are the second most preferred distribution channel for chocolate purchases in South America. Convenience stores are very easy to approach as they are located near residential and commercial areas and generally offer affordable chocolates. The sales value of chocolates through convenience stores registered a growth rate of 8.3% from 2020 to 2023.

- Online channels are the fastest-growing distribution channel through which chocolates are consumed in the region. The distribution segment is projected to register a growth of 16.1% by value during the period 2024-2027. The evolving role of online retail channels in food and beverages, including chocolate purchases, is influenced by the increasing number of internet users. In 2022, 38 million shoppers in Brazil shopped online to purchase goods and services, including chocolates. Also, 42% of Brazilian online buyers prefer shopping through apps that offer fast shipping.

Indulgent snacking behavior and demand from Brazil and Rest of South America, recording an almost 90% value share in 2023, drive the regional market

- Brazil is identified as the major market in the region, followed by Argentina. The rise in consumer preference for convenient indulgent snacking is identified as the key market driver in the region. As of 2023, 39% of Brazilian consumers aged 16-34 years snacked to relax/de-stress. Also, 32% of consumers aged over 35 years believe that eating snacks helps them deal with anxiety.

- In Brazil, chocolate is the most widely consumed confection, with a 50.02% share of the overall confectionery market in 2023 in terms of volume. Brazilians perceive chocolate as a unique and essential indulgent snack due to its flavor. In 2022, 67% of consumers consumed chocolate at least once a week. Within chocolate products, dark chocolate is the fastest-growing segment in the country, with an anticipated CAGR of 6.44% in terms of value during 2023-2030. The market's growth is attributed to the consumer shift toward guilt-free indulgence. In 2022, 81% of consumers preferred snacks personalized as per their health needs.

- Argentina is identified as the fastest-growing confectionery market in South America. The Argentine market is anticipated to record a CAGR of 5.83% by value during the forecast period. Argentina is one of the powerhouse snackers globally, where snacking occurs at multiple points during the day alongside regular mealtimes. In 2023, the annual per capita consumption of chocolate was 1.6 kg.

- In the Rest of South America, Chile and Peru are major countries driving growth, collectively accounting for more than 60% of sales by volume in 2023. The rising consumption of milk, as well as dark chocolates, is primarily attributed to the rising gifting culture among consumers, together with the increasing domestic consumption of chocolates among younger and adult populations.

South America Chocolate Market Trends

Impulse buying behavior supported with the differentiation of products in terms of ingredients and packaging plays a vital role in the market's growth

- In South America, chocolate consumption is prominent across Brazil compared to other countries in the region. Chocolates remain the most consumed confectionery in the country. In 2022, 75% of the Brazilian population consumed chocolate, and 35% of Brazilian people consumed chocolate regularly over any other food or drink.

- Packaging and ingredients influence the impulse buying of chocolates in the region. Sustainability is an increasingly important factor for consumers when it comes to chocolate packaging and ingredients. As of 2023, 40% of Brazilian consumers prefer snacks, including chocolates, in sustainable packaging.

- Consumers in South America are becoming more interested in premium chocolate products. In Brazil, as of 2023, 76% of consumers are willing to pay more for high-quality/premium snacks, including organic chocolates and vegan chocolates.

- The rising consumer inclination toward low-sugar or low-calorie snack food is estimated to create lucrative opportunities for healthy variants of chocolates during the forecast period. In 2021, 'Zero sugar' (46%) and 'light' (55%) were the most common sugar claims in sugar-free and reduced-sugar food products, respectively, in Brazil.

South America Chocolate Industry Overview

The South America Chocolate Market is fairly consolidated, with the top five companies occupying 92.12%. The major players in this market are Arcor S.A.I.C, Cacau Show, Ferrero International SA, Mondelez International Inc. and Nestle SA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Regulatory Framework

- 4.2 Consumer Buying Behavior

- 4.3 Ingredient Analysis

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Confectionery Variant

- 5.1.1 Dark Chocolate

- 5.1.2 Milk and White Chocolate

- 5.2 Distribution Channel

- 5.2.1 Convenience Store

- 5.2.2 Online Retail Store

- 5.2.3 Supermarket/Hypermarket

- 5.2.4 Others

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Arcor S.A.I.C

- 6.4.2 Cacau Show

- 6.4.3 Chocoladefabriken Lindt & Sprungli AG

- 6.4.4 Confiteca CA

- 6.4.5 Ferrero International SA

- 6.4.6 Grupo de Inversiones Suramericana SA

- 6.4.7 Mars Incorporated

- 6.4.8 Mondelez International Inc.

- 6.4.9 Nestle SA

- 6.4.10 Nugali Chocolates

- 6.4.11 The Hershey Company

- 6.4.12 The Peccin SA

7 KEY STRATEGIC QUESTIONS FOR CONFECTIONERY CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms