風力タービンのメンテナンス・修理・オーバーホール(MRO)市場-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Wind Turbine Maintenance, Repair and Overhaul (MRO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683100

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

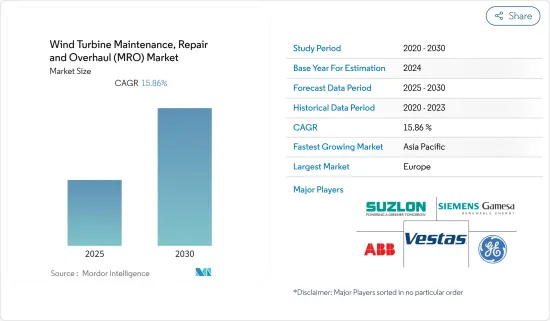

風力タービンのメンテナンス・修理・オーバーホール(MRO)市場は予測期間中にCAGR 15.86%を記録する見込み

主要ハイライト

- 風力タービンのオフショア配備の増加が世界の風力タービンのメンテナンス・修理・オーバーホール(MRO)(MRO)市場を牽引し、予測期間中に最も急成長するセグメントとなる可能性が高いです。

- さらに、発電用風力発電の採用が大幅に増加しています。さまざまな国が風力発電市場に投資しており、メンテナンスの必要性が高まる可能性が高いです。中東・アフリカは風力発電所の著しい成長を目の当たりにしており、これが世界の風力タービンのメンテナンス・修理・オーバーホール(MRO)市場の成長に機会を提供すると考えられます。

- アジア太平洋は、2020年に風力発電設備容量が最大かつ最速で増加するため、最も急成長する地域と予想されます。

風力タービンのMRO市場動向

洋上風力発電設備が大きな成長を遂げる見込み

- エネルギー需要が高まる中、クリーンなエネルギーを供給できる再生可能エネルギーの導入に主要国や企業が舵を切っています。先進技術を駆使した洋上風力発電の導入は、国や企業の高額投資を引き付けています。

- 導入場所別では、コストの低下と技術の向上により、予測期間中も洋上産業が世界の風力タービン産業投資の牽引役であり続けると予想されます。

- 世界のオフショア市場は2020年も安定的に推移し、新規増設量は2019年とほぼ同じ606万kWとなりました。オフショアの累積設置容量は3,530万kWに達し、前年比21.7%増となりました。

- 洋上風力産業は2020年に大規模な設置を示しました。例えば、中国は単年度で3GWの洋上風力を設置し、オランダ(設置量150万kW)、ベルギー(設置量706万kW)、英国(設置量483万kW)、ドイツ(設置量237万kW)がこれに続きました。しかし、英国における新規導入量の伸びの鈍化は、主に差金決済契約(CfD)1ラウンドとCfD2ラウンドのプロジェクト実行のずれによるものでした。さらにドイツでは、新規設置の鈍化は主に、不利な条件と短期洋上風力発電プロジェクト・パイプラインの水準低下によるものでした。

- より沖合など、より複雑で困難な環境での風力タービンの導入増加が予想され、風力タービンの能力増強と相まって、風力タービンの運転部品にさらなる圧力がかかっています。その結果、ギアボックスなどの部品の早期故障が発生し、風力発電所の大幅な低迷を招く可能性が高いです。さらに、MROサービスの提供にかかるコストは、陸上サイトよりもはるかに高いです。材料やサービスの増加、アクセスしにくい地形などの要因が、陸上施設に比べて成長を抑制しています。

- したがって、上記の点から、洋上風力発電の導入は、予測期間中に風力タービンのメンテナンス、修理、オーバーホール市場で大きな成長を示すと予想されます。

アジア太平洋が急成長市場になる見込み

- アジア太平洋は、中国の貢献により、世界で最も急速に成長している風力エネルギー市場です。この地域の累積設備容量は346.70GWで、そのうち陸上風力発電の設備容量は336.29GW、洋上風力発電の設備容量は10.41GWです。

- 2020年時点で、中国はアジア太平洋で最大の風力発電設備容量、約278.32GWを有しています。また、陸上風力発電の世界市場でもトップクラスです。2020年、中国は新たに5,893万kWの風力発電を追加し、その内訳は陸上設備が4,894万kW、洋上設備が999万kWです。これらのことは、中国がアジア太平洋におけるメンテナンス・修理・オーバーホール(MRO)サービスの最大市場になると予想されることを示しています。

- 一方、風力発電設備容量でアジア太平洋第2位のインドは、2020年時点で3,862万5,000kWにとどまっています。しかし、人口13億5,000万人のインドでは、今後10年間で電力需要が倍増すると見込まれています。そこでインド政府は、2022年までに再生可能エネルギー発電容量を175GW、そのうち風力発電を60GW、2030年までに450GW、そのうち風力発電を140GWとする目標を掲げています。韓国は、120mのハブ高で695GWという膨大な技術的ポテンシャルを誇っています。

- 韓国はまた、2030年までに6,380万kWの再生可能エネルギー容量を持つことを目指しており、そのうち約1,800万kWが風力発電によるものです。Orstedなどの国際的な企業は、韓国は風力発電、特にその地理的特性を考慮した沖合地域での風力発電で成功する可能性があると述べています。

- このことは、予測期間中、世界の風力タービンのメンテナンス、修理、オーバーホール事業に携わる参入企業にとって、アジア太平洋が優れたビジネス先となることを示すと予想されます。

風力タービンのMRO産業概要

世界の風力タービンのメンテナンス・修理・オーバーホール(MRO)市場は適度にセグメント化されています。この市場の主要企業には、Siemens Gamesa Renewable Energy SA、General Electric Company、Suzlon Energy Ltd、ABB Ltd、Vestas Wind Systems A/Sなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 世界の再生可能エネルギーミックス(2020年)

- 2027年までの風力発電設備容量(GW)と予測

- 市場規模と需要予測(単位:10億米ドル、2027年まで)

- 世界の風力タービンの平均規模(MW)、2018~2027年

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 展開場所

- オンショア

- オフショア

- サービスタイプ

- メンテナンス

- 修理

- オーバーホール

- コンポーネント

- ギアボックス

- 発電機

- ローターブレード

- その他

- 地域

- 北米

- 欧州

- アジア太平洋

- 南米

- 中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Siemens Gamesa Renewable Energy SA

- General Electric Company

- Stork(a Fluor Company)

- Moventas Gears Oy

- ZF Friedrichshafen AG

- Vestas Wind Systems A/S

- Suzlon Energy Ltd

- ABB Ltd

- Dana SAC UK Ltd

- Nordex SE

- Mistras Group

- Integrated Power Services LLC

第7章 市場機会と今後の動向

目次

Product Code: 48701

The Wind Turbine Maintenance, Repair and Overhaul Market is expected to register a CAGR of 15.86% during the forecast period.

Key Highlights

- Increasing, offshore deployment of wind turbine is likely to drive the global wind turbine maintenance, repair, and overhaul (MRO) market, thus making it fastest growing segment during the forecast period.

- Moreover, the adoption of wind power for power generation is increasing significantly. Various countries are investing in the wind energy market which likely to increase the requirement for maintenance. Middle-East and Africa region witnessing significant growth in wind power plant which is likely to provide the opportunity to the growth of global wind turbine maintenance, repair & overhaul market.

- Asia-Pacific is expected to be the fastest growing region, owing to the largest and fastest increase in wind power installed capacity in 2020.

Wind Turbine MRO Market Trends

Offshore Wind Installations Expected to Witness Signifcant Growth

- As demand for energy is rising, major countries and companies are turning towards the adoption of renewable energy as it has the ability to provide clean energy. The adoption of offshore wind energy with advance technology attracted the countries and companies for high investment.

- By location of deployment, the offshore industry is expected to remain the driver of the global wind turbine industry investments during the forecast period, owing to declining costs and improved technology.

- The global offshore market remained stable in 2020, with 6.06 GW of new additions, almost the same as in 2019. The total cumulative offshore installations have reached 35.3 GW, representing a 21.7% increase in cumulative offshore wind installed capacity over the previous year.

- The offshore wind industry witnessed major installations in 2020. For instance, China installed a 3 GW offshore wind in a single year, followed by the Netherlands (installed 1.5 GW), Belgium (installed 706 MW), the United Kingdom (installed 483 MW), and Germany (237 MW). However, the slowdown of growth in terms of new installation in the United Kingdom was mainly due to the gap between the execution of projects in the Contracts for Difference (CfD) 1 and CfD 2 rounds. Furthermore, in Germany, the slowdown in new installations was primarily caused by unfavorable conditions and a lower level of the short-term offshore wind project pipeline.

- The expected increase in the deployment of wind turbines in more complex and challenging environments, such as farther offshore, coupled with the growing capacity of the wind turbine capacity, has put additional pressure on the operating components of the wind turbine. This results in premature failure of the components, such as gearbox and other components, and is likely to cause a significant downturn in wind farms. Additionally, the costs involved in providing MRO services are much higher than onshore sites. Factors, such as increased material, service, and hard-to-access terrains, are restraining growth compared to onshore facilities.

- Therefore, owing to the above points, offshore wind deployments are expected to witness significant growth in wind turbine maintenance, repair & overhaul market during the forecast period.

Asia-Pacific Expected to be the Fastest Growing Market

- Asia-Pacific is the fastest growing wind energy market in the world, owing to the contribution of China. The region has a cumulative installed capacity of 346.70 GW, of which onshore wind power installed capacity is 336.29 GW and offshore wind power installed capacity is 10.41 GW.

- As of 2020, China had the largest wind power installed capacity in Asia-Pacific, around 278.32 GW. The country is also considered among the top markets in the onshore wind power industry globally. In 2020, China added up to 58.93 GW of new wind power, with 48.94 GW onshore installations and 9.99 GW offshore installations. All of this indicates that China is expected to be the largest market for maintenance, repair, and overhaul services in the Asia-Pacific region.

- On the other hand, India, the second-largest country in the Asia-Pacific region in terms of wind energy installed capacity, sat only with a capacity of 38.625 GW as of 2020. However, over the next ten years, the electricity demand is expected to double in the country of 1.35 billion people. Accordingly, the Indian government has set a target of 175 GW of renewable energy capacity by 2022, of which 60 GW is expected to come from wind energy, and a target of 450 GW by 2030, of which 140 GW is expected to be wind-based generation. The country boasts a technical potential at a 120-meter hub height of a vast 695 GW.

- South Korea also aims to have a total renewable energy capacity of 63.8 GW by 2030, with approximately 18 GW coming from wind power. The international players, such as Orsted, have stated that South Korea may thrive from wind power generation, particularly in offshore areas considering its geographical characteristics.

- This, in turn, is expected to present Asia-Pacific as an excellent business destination for players involved in the global wind turbine maintenance, repair & overhaul business during the forecast period.

Wind Turbine MRO Industry Overview

The global wind turbine maintenance, repair, and overhaul market is moderately fragmented. Some of the key players in this market include Siemens Gamesa Renewable Energy SA, General Electric Company, Suzlon Energy Ltd, ABB Ltd, and Vestas Wind Systems A/S among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Global Renewable Energy Mix, 2020

- 4.3 Wind Power Installed Capacity and Forecast in GW, till 2027

- 4.4 Market Size and Demand Forecast in USD billion, till 2027

- 4.5 Global Average Size of Wind Turbine in MW, 2018-2027

- 4.6 Recent Trends and Developments

- 4.7 Government Policies and Regulations

- 4.8 Market Dynamics

- 4.8.1 Drivers

- 4.8.2 Restraints

- 4.9 Supply Chain Analysis

- 4.10 Porter's Five Forces Analysis

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Consumers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitutes Products and Services

- 4.10.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Service Type

- 5.2.1 Maintenance

- 5.2.2 Repair

- 5.2.3 Overhaul

- 5.3 Component

- 5.3.1 Gearbox

- 5.3.2 Generators

- 5.3.3 Rotor Blades

- 5.3.4 Other Components

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Siemens Gamesa Renewable Energy SA

- 6.3.2 General Electric Company

- 6.3.3 Stork (a Fluor Company)

- 6.3.4 Moventas Gears Oy

- 6.3.5 ZF Friedrichshafen AG

- 6.3.6 Vestas Wind Systems A/S

- 6.3.7 Suzlon Energy Ltd

- 6.3.8 ABB Ltd

- 6.3.9 Dana SAC UK Ltd

- 6.3.10 Nordex SE

- 6.3.11 Mistras Group

- 6.3.12 Integrated Power Services LLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

風力タービンのメンテナンス・修理・オーバーホール(MRO)市場-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日