|

市場調査レポート

商品コード

1911467

北米の産業用ファスナー市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)North America Industrial Fasteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の産業用ファスナー市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

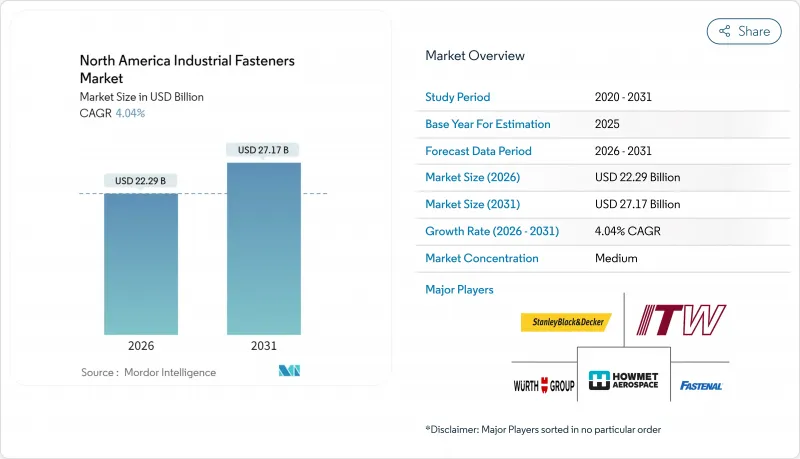

北米の産業用ファスナー市場規模は、2026年に222億9,000万米ドルと推定されております。

これは2025年の214億2,000万米ドルから成長した数値であり、2031年には271億7,000万米ドルに達すると予測されております。2026年から2031年にかけてはCAGR4.04%で成長が見込まれております。

健全なインフラ投資、電気自動車生産の増加、国内製造を優先するリショアリング計画が、投入コストの変動にもかかわらず成長の勢いを維持しています。住宅・商業・土木プロジェクトにおける建設活動が基盤需要を支え、自動車・航空宇宙プログラムが高付加価値の需要量を追加しています。デジタルトレーサビリティ、耐食性コーティング、用途特化設計を統合するサプライヤーは価格決定力を強化しています。エンドユーザーは組み立て時間の短縮、耐用年数の延長、コンプライアンス対応の容易化を実現するエンジニアリングソリューションを引き続き重視しています。競合の激しさは中程度に留まっております。主要な既存企業は、規模の経済、流通網の深さ、そして戦略的な買収を活用し、地位を固めております。

北米の産業用ファスナー市場の動向と洞察

建設セクターの勢いがファスナー需要を支える

1兆2,000億米ドル規模のインフラ投資・雇用創出法に基づく建設支出により、高強度ボルト、アンカー、ねじ棒を必要とする橋梁、交通ハブ、公益事業プロジェクトが安定的に供給されています。テキサス州およびフロリダ州における住宅改修および集合住宅着工により、建材販売業者は大量のバルクネジや釘を継続的に発注しております。プレハブおよびモジュラー建築技術では、クレーン設置時に迅速に調整でき、公差を維持する精密設計のファスナーが好まれます。サプライチェーン管理者は、腐食性の沿岸地域や寒冷気候条件に耐えるコーティングを指定する傾向が強まっており、これにより生涯メンテナンスコストを削減できます。完全なトレーサビリティを備えた認証ロットを在庫する流通業者は、米国製品購入義務(Buy-American)への準拠と即時納品を要求する契約を獲得しております。

自動車の電動化が締結部品の要件を変革

バッテリー式電気自動車プラットフォームには、バッテリーパック内の熱サイクル管理と電気的絶縁を担う専用スタッド、スリーブナット、リベットが採用されています。米国組立ラインを拡大する自動車メーカーは、軽量シャーシにおけるガルバニック腐食を抑制するアルミニウム対応締結部品を必須としています。高速ロボット組立は、一貫したトルク・テンション性能への需要を促進し、サプライヤーにより厳しい寸法公差を求めます。電気ピックアップトラックやSUVの生産拡大に伴い、1台あたりの平均ファスナー使用量が増加し、APQPおよびPPAP基準に適合したエンジニアリング部品の高価格化を支えています。セルメーカーとの協業は、次世代固体電池向け締結方法の共同開発を加速させています。

構造用接着剤の課題は、従来の締結部品に挑むことである

電気自動車、航空機内装、民生用電子機器における軽量化戦略では、保守性が重要でない箇所で機械式ハードウェアを接着接合に置き換えています。接着剤は荷重を均等に分散させ、応力集中を低減し、ドリル穴加工を削減します。ボルト数を減らした接着と組み合わせたハイブリッド接合技術は、取り付け時間と部品点数を削減し、ファスナー全体の需要を抑制します。これに対し、締結部品サプライヤーは、メンテナンス性を考慮した取り外し可能な設計を推進するとともに、トルク管理が必須の安全上重要な領域に注力することで対応しています。分解しやすいコーティング技術の研究開発は、接着剤との直接的な競合ではなく、その補完を目的としています。

セグメント分析

2025年、北米の産業用ファスナー市場において金属ファスナーは76.80%を占めました。これは建設、機械、輸送分野における強度対コストの優位性を反映しています。炭素鋼ボルトは高速道路橋梁の固定に、ステンレス鋼グレードは食品加工・製薬プラントで使用されています。アルミニウムファスナーは航空宇宙パネルやEVバッテリー筐体を支え、重量削減が単価高を相殺しています。支配的地位にもかかわらず、鋼材価格の周期的な変動は利益率を圧迫し、メーカーは二次加工の自動化やスクラップ管理の強化を迫られています。このセグメントは、州や省を越えた調達を簡素化する標準化された仕様の恩恵を受け続けています。

複合材料および特殊材料は、2031年までにCAGR5.14%で最も急速に成長する分野です。ガラス繊維強化ポリマー、セラミックス、高温合金は、金属が腐食、電気伝導性、磁気干渉に弱点を持つ性能ギャップを埋めます。洋上風力発電機のナセルでは、炭素繊維スタッドが犠牲コーティングなしで海水の侵食に耐えます。半導体製造工場では、クリーンルーム内での粒子飛散を避けるためPEEK製ネジが指定されます。成長は、材料科学における継続的な技術革新と、リードタイム短縮のための最終市場近隣における成形能力の拡大にかかっています。現在、価格プレミアムが普及量を制限していますが、過酷な環境下ではライフサイクルコスト分析が非金属オプションを有利に評価するため、採用は着実に増加しています。こうした動向が、北米の産業用ファスナー市場の長期的な見通しを強化しています。

2025年時点で、木材販売店・整備工場・卸売業者向けに供給される標準グレードのハードウェアが、北米の産業用ファスナー市場規模の62.10%を占めました。大径六角ボルト、粗目ネジ、釘は日常的な修理・組立作業向けに大量の樽詰めパッケージで出荷されます。自動冷間鍛造ラインによる規模の経済が実現され、輸入圧力に抗する競争力ある価格設定が可能となっています。しかしながら、コモディティ化は利益率の低下を招き、生産者を原材料価格変動のリスクに晒しています。

航空宇宙、防衛、エネルギー分野において耐熱合金、高精度ねじ、独自コーティングが要求されることから、高性能ファスナーは年率4.98%の成長が見込まれます。超合金スタッドはジェットエンジンケーシングを固定し、二相ステンレスボルトは周期的な圧力に耐える海底パイプラインを締結します。AS9100やNADCAPなどの認証制度はリードタイムを延長しますが、一度承認されればサプライヤーを固定化し、魅力的な収益を可能にします。多くの企業が複雑な形状のプロトタイプを製作するため、高価な金型を必要としない積層造形のパイロット導入を進めています。こうした特殊部品の用途拡大は価値密度を高め、生産量が伸び悩んでも収益を支え、北米の産業用ファスナー市場のプレミアム層を支えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 建設セクターの成長

- 自動車および航空宇宙製造の拡大

- 耐食性コーティングの進歩

- 北米における電気自動車(EV)サプライチェーンの急速な成長

- 米国製品購入法による現地調達促進

- デジタルトレーサビリティとスマートファスナー構想

- 市場抑制要因

- 構造用接着剤の採用拡大

- 鉄鋼および非鉄金属価格の変動性

- めっきに対する厳しい環境規制

- 特殊品におけるリショアリング主導の生産能力不足

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済動向が市場に与える影響

第5章 市場規模と成長予測

- 素材別

- 金属

- プラスチック

- 複合材および特殊材料

- グレード別

- 標準

- 高性能

- 製品タイプ別

- 外ねじ

- 内ねじ

- 非ねじ

- 用途特化型/特殊用途

- エンドユーザー用途別

- OEM

- 自動車/自動車産業

- 内燃機関軽自動車

- 内燃機関(ICE)中型・大型トラック/バス

- 電気自動車

- 航空宇宙

- 機械・資本財

- 電気・電子機器

- 加工金属

- 医療機器

- その他のOEM用途

- 自動車/自動車産業

- 保守・修理・運用(MRO)

- 建設

- OEM

- コーティング/仕上げ別

- 無塗装(未コーティング)

- 亜鉛めっき

- 溶融亜鉛めっき

- PTFEおよび特殊コーティング

- 国別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Illinois Tool Works Inc.

- Howmet Aerospace Inc.

- Stanley Black and Decker, Inc.

- Wurth Group

- Fastenal Company

- Fontana Gruppo(Acument Global Technologies, Inc.)

- LISI Group

- Nifco Inc.

- Bulten AB

- ARaymond Group

- Marmon Holdings, Inc.(Berkshire Hathaway)

- Hilti Corporation

- KAMAX Holding GmbH and Co. KG

- Bossard Holding AG

- PennEngineering and Manufacturing Corp.

- Simpson Manufacturing Co., Inc.

- Precision Castparts Corp.(SPS Technologies)

- TriMas Corporation

- Agrati Group

- SFS Group AG

- Optimas Solutions