|

市場調査レポート

商品コード

1690871

北米の物流自動化:市場シェア分析、産業動向、成長予測(2025年~2030年)North America Logistics Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の物流自動化:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

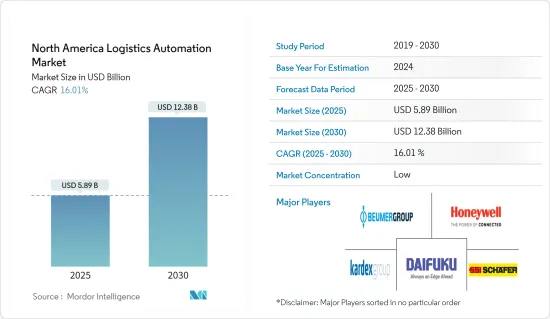

北米の物流自動化市場規模は2025年に58億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは16.01%で、2030年には123億8,000万米ドルに達すると予測されます。

主要ハイライト

- コロナウイルスの大流行は、物流セグメントにおける自動化導入の状況を複雑にしました。社会的距離と非接触操作というユニークな課題をもたらすことで、標準的な操作手順を変更し、組織は労働力を制限し、増加する需要に対処することを余儀なくされました。2020年以降も続くCOVID-19は、米国で多くの重要な労働者に感染し、最前線にいる主要企業が新たな安全プロセスの導入に踏み切るきっかけとなりました。ウィルスの蔓延は、例えば食品製造施設の操業停止を正当化するほど深刻なものであったが、他の複数の企業は新たな健康対策を加えることで操業を継続することができました。

- DHLの調査によると、倉庫業やトラック運送業の組織は、一般的に自動化をいち早く導入した企業として知られていないです。実際、2016年には世界の倉庫の80%がプロセスの自動化を導入していなかりました。

- 物流における自動化とは、業務の効率を高めるための制御システム、機械、ソフトウェアの使用を指します。これは通常、倉庫や配送センターで実行されるプロセスに適用され、最小限の人的介入を必要とします。自動化物流の利点としては、顧客サービスの向上、拡大性とスピード、組織管理、ミスの減少などが挙げられます。

- テネシー大学によると、ロボット工学は、その普及と応用という点で、サプライチェーン全体で最も進んだ技術の一つです。eコマースの継続的な成長と倉庫管理サービスの需要は、今後も増加し続けると予想されます。これは、自動化によるコスト削減ソリューションを見つけるために、このセグメントを加速させるためにさらに整列されています。

- eコマースの台頭により、分割ケース注文や1個単位の出荷も増加しており、フルパレット注文よりも効率的であるために自動化技術に大きく依存しています。さらに、自動化されたストレージソリューションは、生産性を向上させながら、倉庫の設置面積をわずか15%に縮小することができます。

- 2021年4月現在、SoftBank RoboticsとSB Logisticsは、eコマース・フルフィルメント業務のイノベーションを推進するため、Berkshire Greyと協業しています。Berkshire Greyのロボットピック・アンド・パックシステムは、SB物流が異なる製品カテゴリーの複数のSKUSをロボット処理することにより、顧客からの注文を処理するのに役立ちます。SB Logisticsの3PLは、AIを活用した最先端のロボット自動化ソリューションを含むインテリジェントエンタープライズロボティクスソリューションを使用し、日本市場で一般的な極めて高い基準を満たすために、顧客からの注文を自律的にピッキング、配置、梱包します。これは、国内参入企業が他の国で拡大していることを示すものです。

北米の物流自動化市場動向

ハードウェアの中ではソートシステムが大きな成長を遂げる見込み

- 仕分けシステムは、郵便・小包サービス、飲食品、eコマース産業など、さまざまな地域のエンドユーザー産業からの需要が増加しています。人件費の増加や消費者の購買行動の変化といった要因が、より迅速で正確な配送業務への需要を高めており、その結果、自動仕分けシステムへの需要が高まっている

- この地域の近代的な製造施設は、より高品質な製品をより高速に、より低コストで生産するための新技術とイノベーションに依存しています。スマートなソフトウェアとハードウェアの導入は、現在の競争市場で生き残るための唯一の実現可能な方法です。

- さらに、製造・加工部門における効率向上のための産業自動化の採用拡大も、同地域における選別システムの採用を後押しすると予想されます。新しい技術やイノベーションは、さらに産業全体でいくつかの規制の必要性を義務付けています。

- 例えば、FDA食品安全近代化法(FSMA)は、食中毒や異物混入への対応からその予防に重点を移すことで、食品会社の業務を一変させています。このため、マテリアルハンドリングの自動化を促進する食品安全基準を満たすために、産業は高度に規制されています。この要因は、予測期間中、飲食品産業における仕分けシステムを促進すると予想されます。

- 小売・eコマースセクタの著しい成長と倉庫の拡大は、調査された市場成長のもう一つの主要な促進要因です。eコマース売上は2020年第3四半期に小売売上全体の約14.3%に寄与し、そのうち米国ではAmazonがeコマース売上全体の3分の1以上を占めています。

- この地域の小売業者の大半は、このような高価格のレンタル環境で事業を拡大するよりも、倉庫の自動化を計画しています。しかし、同地域の倉庫の80%近くはまだ手作業で運営されています。

米国が主要市場シェアを占める見込み

- 米国は、自動化ソリューションの世界最大かつ最先端市場のひとつです。顕著な港湾交通、eコマースの活発化、主要な製造業指標など、好調な経済が製造業の著しい成長をもたらし、同国の物流部門全体で自動化ソリューションの需要を牽引しています。

- 小売、自動車、飲食品、医薬品などのセクタが、国内における自動化物流ソリューションの最大の需要源です。飲食品は最大の産業であり、米国の年間包装出荷量の35%以上を占めています。

- このため、パレタイザー、ユニットロードAGV、タグAGV、仕分けシステムなど、飲食品製造施設に広く導入されている機器に対する大きな需要が生じています。さらに、厳しい食品安全規制や、生産プロセスにおける人的介入の少なさを好む傾向は、予測期間中に飲食品産業の需要を増加させると予想されます。

- 同地域では数多くのパートナーシップが確認されており、より高い品質の製品をより速いスピードと安いコストで製造するための最新技術やイノベーションに依存しています。

- 例えば最近、アメリカの大手小売企業Krogerは、英国のオンラインスーパーマーケットOcadoと提携を開始し、倉庫業務、物流、自動化、配送ルート計画などに同社の技術を活用することになりました。この提携により、米国では自動化ソリューションによる小売部門の変革が進むことになります。

- また、倉庫の空室率が低く、賃貸料が高騰しているため、企業は倉庫用に貸し出す小規模な場所を探すようになっています。こうした狭いスペースの生産性を最適化するため、自動化ソリューションの導入が進むと予想されます。

- また、多くの倉庫や配送ユニットを持つ大手企業は、人件費を削減し収益性を高めるために買収戦略を活用しています。例えば、巨大小売企業のAmazonは、2012年に7億7,500万米ドルを投じてKiva Systemsという若いロボット企業を買収し、新種の移動ロボットの所有者を得ました。この投資により、新バージョンの倉庫ロボットを構築するための技術的基盤ができ、ロボットの将来の可能性の舞台が整いました。

北米の物流自動化産業概要

承認された資本予算と予想されるリードタイムの範囲内で、必要な機器を製造・統合できるベンダーが、市場を独占し続けています。物流自動化市場は、複数の世界の参入企業で構成され、かなり競合の激しい市場空間で注目を集めようと競い合っています。

技術的混乱は、サステイナブル競合優位性の重要な要因となっています。また、提供するサービスの差別化を図るため、各参入企業はサービス機能へと移行しています。例えば、ローカスは自社技術のトレーニング面を考慮し、同社のLocusEmpowerソリューションはトレーニングを支援し、数ヶ月ではなく数日で労働者を入社させるとしています。

同市場における著名な参入企業としては、Honeywell、Swisslog、Daifuku、Schaeferなどが挙げられます。これらの参入企業の存在と絶え間ない革新的な活動が、市場のシナリオを激化させています。同市場は新規参入企業にとって適度な参入障壁となっているため、VCの支援を受けた複数の新規参入企業が同市場で牽引力を発揮しています。これにより、市場競争はさらに激化する可能性があります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- COVID-19の産業エコシステムへの影響

- 市場の促進要因

- eコマースの活発化

- 市場課題

- 高い設備投資と技術の初期性

第5章 市場セグメンテーション

- ソリューションタイプ別

- ハードウェア

- 移動ロボット(無人搬送車(AGV)、自律移動ロボット(AMR))

- 自動化保管・検索システム(AS/RS)(ユニットロード-固定通路と可動通路、ミニロード、シャトル&ボットシステム、その他のシステム-カルーセルと垂直リフトモジュール)

- コンベア(ベルト、ローラー、パレット、オーバーヘッド)

- パレタイザー/デパレタイザー(従来型-ハイレベル+ローレベル、ロボット式)

- 仕分けシステム

- ソフトウェア-倉庫管理システム(WMS)、WES、WCS

- その他のソリューション

- 輸送管理ソリューション

- その他(ピースピッキングロボット、協働ロボット、倉庫ドローン、サポートインフラ)

- ハードウェア

- 業種別

- 一般商品

- アパレル

- 飲食品

- 食料品

- 郵便・小包

- 製造業(耐久・非耐久)

- その他

- 国別

- 米国

- カナダ

第6章 競合情勢

- 企業プロファイル

- SSI SCHAEFER AG

- Daifuku Co. Limited

- Kardex Group

- Honeywell Intelligrated

- Beumer Group GMBH & Co. KG

- Jungheinrich AG

- Murata Machinery Limited

- TGW Logistics Group GmbH

- Witron Logistik

- Mecalux SA

- Viastore Systems GmbH

- Swisslog Holdings AG(KUKA AG)

- Kion Group AG(Dematicを含む)

- Vanderlande Industries BV

- ベンダーランキング分析

- Mobile Robots

- AS/RS

- Collaborative Robots

- Palletizers/De-palletizers

- Conveyors/Sortation Systems

第7章 投資分析

第8章 市場の将来

The North America Logistics Automation Market size is estimated at USD 5.89 billion in 2025, and is expected to reach USD 12.38 billion by 2030, at a CAGR of 16.01% during the forecast period (2025-2030).

Key Highlights

- The Coronavirus pandemic complicated the situation of automation adoption in logistics sector. By bringing in unique challenges of social distancing and contactless operation it has changed the standard operating procedure and organizations were forced to limit workforce, and deal with the increasing demand. COVID-19 over 2020 and continuing has infected a number of essential workers in the United States, leading companies on the front lines to implement new safety processes. While the spread of the virus has been grave enough to warrant shutdowns for instance, food production facilities, multiple other businesses have been able to continue operations with the addition of new health measures.

- Organizations within the warehousing and trucking industries, when considered, are generally not known as early adopters to automation; in fact, 80% of warehouses globally didn't have any process automation in 2016 as per DHL study.

- Automation in logistics refers to the use of control systems, machinery, and software to enhance the efficiency of operations. It usually applies to the processes performed in a warehouse or distribution center, which requires minimal human intervention. Some of the benefits of automation logistics are improved customer service, scalability and speed, organizational control, and reduced mistakes.

- As per the University of Tennessee, robotics has been one of the most advanced technologies across a supply chain in terms of its proliferation and application. The continued growth in e-commerce and the demand for warehousing services is expected to continue to increase. This is further aligned for acceleration in the segment in order to find cost-reduction solutions through automation.

- The rise of e-commerce has brought a rise in split case orders and even single-unit shipments, which rely much more heavily on automation technologies to be efficient than full-pallet orders. Additionally, an automated storage solution serves an ability to shrink a warehouse's footprint to just 15 percent while increasing productivity.

- As of April 2021, SoftBank Robotics and SB Logistics collaborated with Berkshire Grey to drive innovation in E-Commerce fulfillment operations. Berkshire Grey's robotic pick and pack systems would benefit SB Logistics to process customer orders by robotically handling multiple SKUS in different product categories. SB Logistics' 3PL would use Intelligent Enterprise Robotics solutions, including leading AI-enabled robotic automation solutions to autonomously pick, place, and pack customer orders to best meet the extremely high standards prevalent in the Japanese market. This marks domestic player's expanding in other countries.

North America Logistics Automation Market Trends

Among Hardware, Sortation System is Expected to Witness Significant Growth

- Sortation systems are witnessing increased demands from various regional end-user industries, such as post and parcel services, food and beverages, and the e-commerce industry. Factors such as increasing labor costs and changing consumer buying behavior have bolstered the demand for faster and more accurate delivery operations, which have, in turn, developed a considerable demand for automated sortation systems.

- Modern manufacturing facilities in the region rely on new technologies and innovations to produce higher quality products at faster speeds, with lower costs. Implementing smart software and hardware proves to be the only feasible way to survive in the current competitive market.

- Further, the growing adoption of industrial automation to enhance efficiency in the manufacturing and processing sectors is also expected to boost the adoption of sortation systems in the region. New technologies and innovations have further mandated the need for several regulations across the industries.

- For instance, the FDA Food Safety Modernization Act (FSMA) is transforming the operations of food companies by shifting the focus from responding to foodborne illness and foreign material contamination to preventing it. This makes the industry highly regulated to meet food safety norms that promote automation in material handling. This factor is expected to drive the sortation system in the food and beverage industry over the forecast period.

- The significant growth of the retail and e-commerce sector and warehouse expansion is another primary driver of the studied market growth. E-commerce sales contributed to about 14.3% of total retail sales in the third quarter of 2020, of which Amazon accounted for more than a third of all e-commerce sales in the United States.

- Most of the retailers in the region are planning to automate their warehouse establishments rather than expanding in such a high-priced rental environment. However, almost 80% of the warehouses in the region are still manually operated.

United States is Expected to Account for Major Market Share

- The United States is one of the largest and most advanced markets for automated solutions globally. The strong economy, with notable port traffic, increased e-commerce activity, and key manufacturing indices, all resulting in significant growth in manufacturing, drive the demand for automated solutions across the logistics sector in the country.

- Sectors, including retail, automotive, food and beverage, and pharmaceutical, are the largest sources of demand for automated logistics solutions in the country. Food and beverage is the largest industry and represents more than 35% of all US packaging shipments annually.

- This creates a significant demand for equipment, such as palletizers, unit load AGVs, tug AGVs, and sortation systems, which are extensively deployed in food and beverage manufacturing establishments. Moreover, the stringent food safety regulations and preference for low human intervention in the production process are expected to increase the demand for the food and beverage industry over the forecast period.

- The region is witnessing numerous partnerships and is relying on the latest technologies and innovations to manufacture a higher quality of products at quicker speeds and cheaper costs.

- For instance, recently, a principal American retail company, Kroger, started a partnership with the UK online supermarket, Ocado, to utilize its technology to handle warehouse operations, logistics, automation, and delivery route planning in the region. This partnership is set to transform the retail sector, with the aid of automation solutions, in the United States.

- Additionally, owing to low vacancy and a surge in the rental prices of warehouses, enterprises are progressively looking for smaller places to rent out for warehouse purposes. In order to optimize the productivity of these narrow spaces, they are expected to deploy more automated solutions soon.

- Also, the major companies with many warehouses and distribution units utilize acquisition strategies to reduce labor costs and increase their profitability. For instance, Amazon, the giant retail, has spent USD 775 million in 2012 to acquire a young robotics company called Kiva Systems that gave it ownership over a new breed of mobile robots. This investment gave a technical foundation for building new versions of warehouse robotics, setting the stage for a potential future of the robots.

North America Logistics Automation Industry Overview

The market vendors that can fabricate and integrate the required equipment within the approved capital budgets and expected leads times have been continuing to dominate the market. The logistics automation market comprises several global players, vying for attention in a fairly-contested market space.

Technological disruption has been a key factor in sustainable competitive advantage. Also, in order to differentiate amongst offerings, the players have been witnessed moving toward the service capabilities. For instance, Locus considered the training aspect of its technology, and its LocusEmpower solution aids in training and the company claims it would onboard workers in days, rather than months.

Some of the prominent players in the market include Honeywell, Swisslog, Daifuku, Schaefer, among others. The presence of these players and their constant innovative activities are intensifying the market scenario. As the market poses moderate barriers to entry for new players, several new entrants backed by VC's have been able to gain traction in the market. This could further intensify the market competition.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Impact of COVID-19 on the Industry Ecosystem

- 4.5 Market Drivers

- 4.5.1 Increased E-commerce Activity

- 4.6 Market Challenge

- 4.6.1 High Capital Investment & Nascency Of The Technology

5 MARKET SEGMENTATION

- 5.1 By Solution Type

- 5.1.1 Hardware

- 5.1.1.1 Mobile Robots (Automated Guided Vehicle (AGV) and Autonomous Mobile Robots (AMR))

- 5.1.1.2 Automated Storage and Retrieval System (AS/RS) (Unit Load - Fixed and Movable Aisle, Mini Load, Shuttle & Bot Systems and Other Systems - Carousels and Vertical Lift Modules)

- 5.1.1.3 Conveyor (Belt, Roller, Pallet and Overhead)

- 5.1.1.4 Palletizer/De-palletizer (Conventional - High Level + Low Level, and Robotic)

- 5.1.1.5 Sortation System

- 5.1.2 Software - Warehouse Management Systems (WMS), WES and WCS

- 5.1.3 Other Solutions

- 5.1.3.1 Transportation Management Solutions

- 5.1.3.2 Others (Piece-picking robots, collaborative robots, warehouse drones, and supporting infrastructure)

- 5.1.1 Hardware

- 5.2 By Industry

- 5.2.1 General Merchandise

- 5.2.2 Apparel

- 5.2.3 Food and Beverages

- 5.2.4 Groceries

- 5.2.5 Post & Parcel

- 5.2.6 Manufacturing (Durable and Non-Durable)

- 5.2.7 Other Industries

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 SSI SCHAEFER AG

- 6.1.2 Daifuku Co. Limited

- 6.1.3 Kardex Group

- 6.1.4 Honeywell Intelligrated

- 6.1.5 Beumer Group GMBH & Co. KG

- 6.1.6 Jungheinrich AG

- 6.1.7 Murata Machinery Limited

- 6.1.8 TGW Logistics Group GmbH

- 6.1.9 Witron Logistik

- 6.1.10 Mecalux SA

- 6.1.11 Viastore Systems GmbH

- 6.1.12 Swisslog Holdings AG (KUKA AG)

- 6.1.13 Kion Group AG (including Dematic)

- 6.1.14 Vanderlande Industries BV

- 6.2 Vendor Ranking Analysis

- 6.2.1 Mobile Robots

- 6.2.2 AS/RS

- 6.2.3 Collaborative Robots

- 6.2.4 Palletizers/De-palletizers

- 6.2.5 Conveyors/Sortation Systems