|

市場調査レポート

商品コード

1645079

英国のケミカルロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)United Kingdom Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国のケミカルロジスティクス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

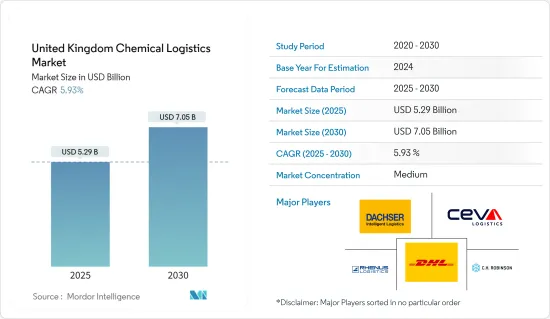

英国のケミカルロジスティクスの市場規模は2025年に52億9,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.93%で、2030年には70億5,000万米ドルに達すると予測されています。

英国では、ケミカルロジスティクス業務に厳しい法的要件があります。2001年6月27日の欧州議会および理事会指令2001/45/EECは、作業中の労働者に対する作業機器の適用に関する最低限の安全衛生要件に関する理事会指令89/655/EECを改正するものです。(理事会指令89/391/EECの第16条(1)に基づく第2次個別指令)。

業界の専門家によると、化学品と化学製品からの収益は、石鹸と洗剤、香水、クリーナー、研磨剤またはトイレ用品のカテゴリーで、2023年に92億8,000万米ドル増加し、2024年には95億6,000万米ドルに達するといいます。

英国の化学品市場の付加価値額は、2023年の122億8,000万米ドルから2024年には127億6,000万米ドルに達すると報告されています。技術革新と技術進歩は、化学部門の頻繁な原動力です。研究開発に投資し、新しく改良された製品やプロセスを導入することで、英国化学市場の企業の付加価値を高めることができます。

英国のケミカルロジスティクス市場の動向

ブレグジットの対英貿易への影響

英国に輸入される化学製品は著しく減少しており、ブレグジットの影響を示しています。業界専門家によると、2021年には132億2,000万米ドルの取引が行われたが、2022年には100億2,000万米ドルの取引しか行われなかった。同国では、この期間にほぼ24%の減少が見られました。

中国と英国間の商取引は一転しました。化学製品の輸入額は2021年の60億米ドルから2022年には29億5,000万米ドルに激減しました。

英国の非EU諸国、特に米国への輸出は不調です。部分的には、非輸出市場を中心に減少しているようで、英国が需要増加の恩恵を受ける立場が弱くなっているためです。雑多な化学製品の対米輸出額は、2021年の12億5,000万米ドルから2022年には11億1,000万米ドルに減少しています。

英国の化学品消費

英国の肥料の輸入額は増加しており、同国の化学品消費と物流の必要性を示しています。Statistaによると、2022年に英国は26億2,000万米ドル相当の肥料を輸入します。

Croda International Plcは英国最大の化学企業であり、Johnson Matthey Plcがそれに続く。業界の専門家によると、英国における2022年の純利益はそれぞれ1億9,390万ポンド(2億4,412万米ドル)と1億7,700万ポンド(2億2,284万米ドル)だった。これは同国の化学品消費額を示しています。

また、2023年11月、化学産業におけるポリオレフィンのサプライヤーであるLyondellBasell社は、英国に同社のグレードの新しい流通センターを設立すると発表しました。顧客の施設に在庫を置くことで注文のリードタイムを短縮し、顧客体験を向上させるという同社のコミットメントの一環として、この戦略的な動きはこうした取り組みの継続となります。英国におけるこの物流ハブは、LyondellBasellの世界・フットプリントの重要な一部です。

英国のケミカルロジスティクス業界の概要

英国のケミカルロジスティクス市場は、様々な企業が存在するため競争が激しいです。英国のeコマース物流市場は適度に細分化されており、市場プレイヤー間の競争を描き出しています。競合情勢はダイナミックで、新たな動向、技術の進歩、消費者の嗜好の変化に適応するために、継続的な開発と競合が企業を駆り立てています。DHLのような世界のロジスティクス大手は強い存在感を示しており、速達便からサプライチェーン管理まで幅広いサービスを提供しています。しかし、英国のケミカルロジスティクス業界は、厳しい規制や厳格な安全・環境基準のため、参入障壁が比較的高いです。DHL International Gmbh、Dachser、Rhenus Logisticsは、この分野で最も重要なプレーヤーです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 技術動向

- 業界のバリューチェーン分析

- 政府の規制と取り組み

- 3PLに関する洞察

- バリューチェーン/サプライチェーン分析

- 需要と供給の分析

第5章 市場力学

- 促進要因

- 厳しい規制への対応

- サプライチェーンの世界化

- 抑制要因

- 環境への懸念

- 機会

- グリーン物流

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第6章 市場セグメンテーション

- サービス別

- 輸送

- 倉庫、流通、在庫管理

- コンサルティング&マネジメントサービス

- 通関・セキュリティ

- グリーンロジスティクス

- その他のサービス

- 輸送手段別

- 道路

- 鉄道

- 航空

- 水路

- パイプライン

- エンドユーザー別

- 製薬業界

- 化粧品産業

- 石油・ガス産業

- 特殊化学品産業

- その他のエンドユーザー

第7章 競合情勢

- 企業プロファイル

- DHL

- DACHSER

- Rhenus Logistics

- C.H. Robinson

- CEVA Logistics

- Den Hartogh

- BDP International

- Streamline Shipping

- Hoyer Group

- Suttons Group*

- その他の企業

第8章 市場機会と今後の動向

第9章 付録

The United Kingdom Chemical Logistics Market size is estimated at USD 5.29 billion in 2025, and is expected to reach USD 7.05 billion by 2030, at a CAGR of 5.93% during the forecast period (2025-2030).

There are strict legal requirements for chemical logistics operations in the United Kingdom. Directive 2001/45/EEC of the European Parliament and of the Council of 27 June 2001, which amends Council Directive 89 /655 / EEC on the minimum health and safety requirements for the application of work equipment to workers at work. (Second individual Directive under Article 16 (1) of Council Directive 89 /391 / EEC).

According to industry experts, the revenue from chemicals and chemical products is set to increase by USD 9.28 billion in 2023 up to USD 9.56 billion in 2024 for the category of soap and detergents, perfumes, cleaners, and polishings or toilet preparations.

The value added in the UK chemicals market is reported to amount to USD 12.76 billion in 2024 from USD 12.28 billion in 2023. Innovation and technical progress are frequent drivers of the chemicals sector. Investing in R&D and introducing new and improved products or processes can increase the value added by companies in the United Kingdom chemical market.

United Kingdom Chemical Logistics Market Trends

The Impact of Brexit on Trade with the United Kingdom

Chemical products imported into the United Kingdom have severely declined, indicating an effect of Brexit. According to industry experts, while transactions worth USD 13.22 billion were done in 2021, only USD 10.02 billion was done in 2022. The country saw a decline of almost 24% in the period.

Business transactions between China and the UK have taken a turn. The import value of chemical products has fallen sharply from USD 6.0 billion in 2021 to USD 2.95 billion in 2022.

The United Kingdom's exports to non-EU countries, particularly to the United States, have performed poorly. Partially, this is due to the United Kingdom being in a weaker position to benefit from increased demand, as it seems to be declining mainly in non-exporting markets. The export value of miscellaneous chemical products to the United States has fallen from USD 1.25 billion in 2021 to USD 1.11 billion in 2022.

Chemical Consumption in the United Kingdom

The United Kingdom's import value of fertilizers has been rising, indicating the country's consumption of chemicals and the need for logistics. According to Statista, in 2022, the United Kingdom imported USD 2.62 billion worth of fertilizers.

Croda International Plc is the largest chemical company in the United Kingdom in terms of revenue, followed by Johnson Matthey Plc. According to industry experts, their 2022 net income in the United Kingdom was GBP 193.9 million (USD 244.12 million) and GBP 177 million (USD 222.84 million), respectively. This indicates the value of the country's consumption of chemicals.

Also, in November 2023, LyondellBasell, a supplier of polyolefins in the chemical industry, announced that it is setting up a new distribution center for its grades in the United Kingdom. As part of their commitment to improve the customer experience by placing stocks in customers' facilities, which reduces lead times for orders, this strategic move is a continuation of these efforts. This distribution hub in the United Kingdom is an integral part of LyondellBasell's global footprint.

United Kingdom Chemical Logistics Industry Overview

The market for chemical logistics in the United Kingdom is competitive, owing to the presence of various companies. The e-commerce logistics market in the United Kingdom is moderately fragmented and depicts competition among the market players. The competitive landscape is dynamic, with ongoing developments and competition driving companies to adapt to emerging trends, technological progress, and changing consumer preferences. Global logistics giants such as DHL have a strong presence, providing a range of services from express delivery to supply chain management. However, the chemical logistics industry in the United Kingdom has relatively high entry barriers due to stringent regulations and strict safety and environmental standards. DHL International Gmbh, Dachser, and Rhenus Logistics are among the most important players in this sector.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Government Regulations and Initiatives

- 4.5 Insights into the 3PL

- 4.6 Value Chain / Supply Chain Analysis

- 4.7 Demand and Supply Analysis

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Adherence to Stringent Regulations

- 5.1.2 Globalization of Supply Chains

- 5.2 Restraints

- 5.2.1 Environmental Concerns

- 5.3 Opportunities

- 5.3.1 Green Logistics

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers / Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Transportation

- 6.1.2 Warehousing, Distribution, and Inventory Management

- 6.1.3 Consulting & Management Services

- 6.1.4 Customs & Security

- 6.1.5 Green Logistics

- 6.1.6 Other Services

- 6.2 By Mode of Transportation

- 6.2.1 Roadways

- 6.2.2 Railways

- 6.2.3 Airways

- 6.2.4 Waterways

- 6.2.5 Pipelines

- 6.3 By End User

- 6.3.1 Pharmaceutical Industry

- 6.3.2 Cosmetic Industry

- 6.3.3 Oil and Gas Industry

- 6.3.4 Specialty Chemicals Industry

- 6.3.5 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 DHL

- 7.2.2 DACHSER

- 7.2.3 Rhenus Logistics

- 7.2.4 C.H. Robinson

- 7.2.5 CEVA Logistics

- 7.2.6 Den Hartogh

- 7.2.7 BDP International

- 7.2.8 Streamline Shipping

- 7.2.9 Hoyer Group

- 7.2.10 Suttons Group*

- 7.3 Other Companies