|

市場調査レポート

商品コード

1645036

シンガポールのケミカルロジスティクス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Singapore Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シンガポールのケミカルロジスティクス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

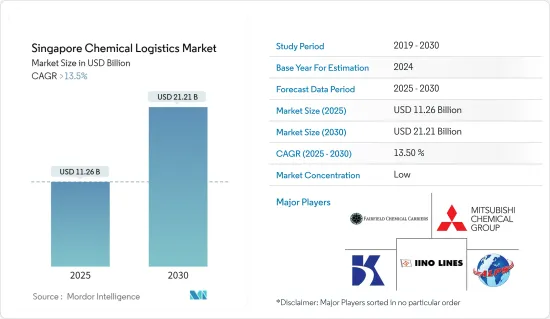

シンガポールのケミカルロジスティクスの市場規模は2025年に112億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは13.5%を超え、2030年には212億1,000万米ドルに達すると予測されます。

主なハイライト

- シンガポールは、精製、オレフィン生産、化学品製造、ビジネス、イノベーション能力を強力に組み合わせた世界有数のエネルギー・化学センターです。100社を超える国際的な化学企業の主要拠点となっています。シンガポールの石油化学、特殊化学、精製事業の主要拠点はジュロン島です。顧客とサプライヤーは、高度に統合されたインフラによって緊密に結ばれており、文字通りフェンス越しにパイプでつながっています。ユーティリティや物流サービス・プロバイダーを含むこの統合されたエコシステムは、企業にとってコスト削減の生産シナジーを生み出します。ジュロン島には総額372億7,000万米ドル以上の投資が行われています。シンガポールは、世界産業がテーラーメイドの配合や環境に優しい処方へと進化する中、持続可能で生産性の高い化学品製造の拠点として位置づけられています。

- 化学製品の倉庫や貯蔵施設の新設は、非常に資本集約的な事業であり、さまざまな基準を遵守し、認可を取得する必要があります。さらに、倉庫には非常に大きな運営・維持コストがかかります。倉庫ソリューションのニーズが高まっているため、この分野にはさまざまな投資が集まっています。しかし、倉庫の効率的かつ効果的な運用は重要な義務です。実用的かつ効果的な倉庫・貯蔵施設に必要な不可欠な要素のいくつかは、適切な財務モデリング、需要マッピング、インフラ評価です。倉庫の製造と設置に関わる現金は不可逆的であるため、投資回収に必要な期間は長いです。その結果、倉庫の設置や運営、在庫ロスの管理に多額の費用がかかるため、予測期間中の市場の成長は制限されると予想されます。

- シンガポールは欧州金融危機から遠く離れているとはいえ、化学産業は世界の出来事の影響を直接受ける。石油・ガスセクターと密接な関係にあるため原料価格に左右され、貿易摩擦にさらされ、消費者動向の変化にも左右されます。パンデミックにもかかわらず、あるいはパンデミックのためかもしれないが、GBRが今年話を聞いた企業のほとんどすべてが、2022年第1四半期は堅調な成長、2021年は記録的な成長を遂げたと報告しています。しかし、将来は不透明であり、化学企業がいかにコストをバリューチェーンの次のリンク、ひいては顧客に転嫁できるかにかかっています。

- パフォーマンス・ケミカルは、原料価格やエネルギー価格の上昇の影響を直接受けるバルク・ケミカルよりも、コストを転嫁して健全なマージンを生み出すのに有利な立場にあります。利用可能な原材料の不足と継続的な物流の制約が相まって、特殊化学品業界の企業にとって重大な問題を引き起こしており、注文が遅れ、品目によっては長期の入荷待ちに陥っています。シンガポールのセクターは、現在の市場要因に加えて、アジア太平洋の非常に良好な人口動態のファンダメンタルズの影響を受けています。このセクターは栄養に高い優先順位を置いており、シンガポールは食料安全保障と食料持続可能性の両方の困難との戦いの中心にいます。

シンガポールケミカルロジスティクス市場の動向

化学生産の増加が市場を牽引

- 水曜に発表された政府の統計によると、特殊品と石油化学部門の生産減少の結果、3月のシンガポール全体の化学品生産高は前年同月比11.8%減少しました。経済開発庁(EDB)は声明で、2023年3月の石油化学生産が前年同月比20.3%減少したのは「市場需要の低迷とプラントのメンテナンス停止」が原因であると述べた。鉱油と食品添加物の生産が減少したため、同月の特殊部門の生産高は6.5%減少しました。2022年の同時期と比較すると、石油を含む化学クラスターの総生産高は、2023年1月から3月まで毎年13.1%減少しました。シンガポール全体の工業生産は、2023年2月が年率9.7%減であったのに対し、2023年3月は4.2%減とそれほど顕著な減少ペースではありません。

- シンガポールの化学産業を、食品、再生可能エネルギー、特殊なバイオベース材料などの他のセクターと区別することは難しくなっています。化学産業や石油産業の最大手は、水素のような新しいエネルギーへの最大の投資家でもあり、化学企業の研究施設は、炭素回収・隔離や高度な分子リサイクルの最先端の技術革新が開発される場所でもあります。人、エンジニア、化学者、労働者、管理職が、さまざまな業界をかつてないほど自由に行き来する一方で、バイオポリマー、バイオ界面活性剤、バイオ燃料は、食品成分と同じ原材料をめぐって競争しています。それらは食品成分と同じデジタル・チャンネルで商品化されています。化学産業の運命は、石油・ガス部門と密接不可分の関係にあります。

- 天然ガスの減少がもたらしたエネルギー危機は、化石燃料からの脱却を好意的に約束する社会にあって、炭素源からの離脱の準備がまだ整っていないことを思い知らされました。インフレが続いているという事実は、ガソリンの価格(そしてそれ以下は入手可能性)がいかに世界経済に密接に影響しているかを示しています。先進国の状況は、インフレ圧力の持続と拡大、それに対応する中央銀行の積極的な引き締めによって、ますます混迷の度を深めています。自動車や建設セクターを含む消費者産業や主要顧客産業は、持続的な景気後退と継続的な高インフレの結果、化学品に対する需要が大幅に減少する可能性があります。

物流サービスとインフラへの投資が市場を牽引

- デバイスの普及が進んでいるため、シンガポールのeコマース市場における1取引あたりの平均注文額は今後数年で上昇すると思われます。サプライチェーンの透明性と安全性は、技術の進歩によって向上し、費用対効果が高まると予測されます。さらに今後数年間は、複合一貫輸送、ロジスティクスパーク、港湾などの物流インフラの開発によって商機が生まれると思われます。食品や大量生産品の原材料の輸出入の増加が、シンガポールの3PL市場の拡大に拍車をかけている主な理由です。国際海運会議所の推定によると、年間およそ110億トンの貨物が船舶で輸送されています。グローバリゼーションの結果、世界の貿易は著しく増加しています。機械・輸送機器と石油はシンガポールの主要輸入品であり、石油精製品は最大の輸出品です。中国、米国、インドネシア、マレーシア、日本が最も重要な貿易相手国です。

- 市場の変動により、メーカーが供給業務を把握することは難しいです。これが、3PLの重要性が増している理由です。さらに、国際市場の成長は、このセクターをさらに助けるかもしれないです。企業が3PLを商品の輸出入のための費用対効果の高いオプションと見なす傾向が強まっているため、3PL利用市場は予測期間を通じてかなりの成長を遂げると思われます。労働力不足やサプライチェーンの問題が続いているため、3PLは自動化やロボット技術を採用し、ライフサイクル全体の業務を合理化しています。同時に、消費者、ブランド、物流サービス・プロバイダーの可視性とコミュニケーションを強化するために、データ主導の発注、倉庫管理、輸送技術が活用されています。このように、シンガポールの3PL市場は、ロジスティクスにおけるテクノロジー導入の高まりにより、かなりの成長が見込まれます。

シンガポールのケミカルロジスティクス産業の概要

シンガポールのケミカルロジスティクス市場は非常に細分化されており、地元、地域、世界のプレーヤーが多数存在します。主なプレーヤーには、ALPS Global Logistics、Koyo Kaiun、Iino Singapore Pte Ltd、Fairfield Chemical Carriers、MCL Logistics Asia Pte Ltdなどがあります。この分野では近年、ビッグデータ分析やIoT技術の採用など、多くの革新的でデジタルな動向が見られ、ケミカルロジスティクス業界の成長をさらに後押ししています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析方法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学

- 現在の市場シナリオ

- 市場概要

- 市場力学

- 促進要因

- 石油化学製品の需要増加が市場を牽引

- 投資の増加が市場を牽引

- 抑制要因

- 高い操業コスト

- 機会

- 技術革新

- 促進要因

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界における技術革新

- 業界への投資誘致に向けた政府の取り組み

- 3PL市場の洞察(市場規模と予測)

- COVID-19が業界に与える影響

第5章 市場セグメンテーション

- サービス別

- 輸送

- 倉庫、配送、在庫管理

- その他のサービス

- 輸送手段別

- 道路

- 鉄道

- 航空

- 水路

- その他の輸送手段

- エンドユーザー別

- 医薬品

- 化粧品

- 石油・ガス

- 特殊化学品

- その他のエンドユーザー

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- ALPS Global Logistics

- Koyo Kaiun Co., Ltd.

- Iino Singapore Pte Ltd

- Fairfield Chemical Carriers

- MCL Logistics Asia Pte Ltd

- Tatsumi Marine(Singapore)Pte Ltd

- MSR Green Corporation(S)Pte Ltd

- Aurora Tankers Management Pte. Ltd.

- Win-Bells Logistics & Services Pte. Ltd.

- DHL

- K" Line Pte Ltd"

- Bertschi Singapore Pte Ltd.

- Kaplan Logistics*

第7章 市場の将来

第8章 付録

The Singapore Chemical Logistics Market size is estimated at USD 11.26 billion in 2025, and is expected to reach USD 21.21 billion by 2030, at a CAGR of greater than 13.5% during the forecast period (2025-2030).

Key Highlights

- Singapore is one of the top energy and chemical centers in the world thanks to its potent combination of refining, olefins production, chemical manufacture, business, and innovation capabilities. Here are major activities for more than 100 international chemical companies. Singapore's main hub for petrochemical, specialty chemical, and refining operations is Jurong Island. Customers and suppliers are connected tightly by its highly integrated infrastructure, frequently literally over the fence through pipes. This integrated ecosystem, which includes utilities and logistical service providers, generates cost-saving production synergies for businesses. Investments totaling more than USD 37.27 billion have been made in Jurong Island. Singapore has positioned itself as a sustainable, highly productive base for chemical manufacture as the global industry evolves towards tailored blending and eco-friendly formulations.

- A new chemical warehouse and storage facility building is a very capital-intensive undertaking that necessitates adhering to a variety of criteria and acquiring approvals. Additionally, warehouses have very significant operational and maintenance costs. Due to the rising need for warehousing solutions, the sector is drawing a variety of investments. The efficient and effective operation of warehouses is a crucial duty, though. Some of the essential components needed for a practical and effective warehouse and storage facility are appropriate financial modeling, demand mapping, and infrastructural evaluations. The period needed to see a return on investment is lengthy since the cash involved in manufacturing and setting up a warehouse is irreversible. Consequently, the high expense of putting up and operating a warehouse and managing inventory loss is expected to limit the growth of the market during the forecast period.

- Even though Singapore is far from the European financial crisis, its chemical industry is directly affected by world events. It is dependent on the price of feedstocks because it is a close relative of the oil and gas sector, exposed to trade conflicts, and subject to changing consumer trends. Despite, and perhaps because of, the pandemic, almost all of the businesses GBR spoke to this year reported robust growth in the first quarter of 2022 and record-level growth in 2021. The future is uncertain, though, and depends on how well chemical companies can transfer costs to the next link in the value chain and ultimately to the customer.

- Performance chemicals are better positioned to pass on costs and generate healthy margins than bulk chemicals, which are directly impacted by rising feedstock and energy prices. The lack of available raw materials combined with ongoing logistical constraints has caused significant problems for companies in the specialty chemical industry, delaying orders and resulting in lengthy waiting lists for some items. The Singaporean sector is subject to the very good demographic fundamentals of Asia-Pacific in addition to the current market factors. The sector places a high priority on nutrition, with Singapore at the center of the fight against the difficulties of both food security and food sustainability.

Singapore Chemical Logistics Market Trends

Increase in chemical production driving the market

- As a result of lower production at the specialities and petrochemicals segments, Singapore's overall chemicals output in March decreased by 11.8% year over year, according to government figures released on Wednesday. The Economic Development Board (EDB) stated in a statement that "weak market demand and plant maintenance shutdowns" were to blame for the 20.3% year-over-year decrease in petrochemical production in March 2023. Due to lower production of mineral oil and food additives, the specialty segment's output for the month decreased by 6.5%, it stated. When compared to the same period in 2022, the total output of the chemicals cluster, which includes petroleum, declined 13.1% annually from January to March 2023. Singapore's overall industrial production declined in March 2023 at a less pronounced annual pace of 4.2% compared to a 9.7% contraction in February 2023.

- It is getting harder to distinguish Singapore's chemical industry from other sectors, such as food, renewables, and specialized bio-based materials ones. The biggest participants in the chemical and oil industries are also the biggest investors in new forms of energy, such as hydrogen, and chemical companies' research facilities are where the most cutting-edge innovations in carbon capture and sequestration and advanced molecular recycling are developed. While people, engineers, chemists, laborers, and managers travel across various industries more freely than ever, bio-polymers, bio-surfactants, and bio-fuels compete for the same raw materials as food components. They are commercialized on the same digital channels as food ingredients. The fate of the chemical industry is still inextricably linked to that of the oil and gas sector.

- The energy crisis brought on by the reduction in natural gas came as a rude reminder that we are still far from being ready to wean ourselves off carbon sources in a society that is virtuously promising to phase out fossil fuels. The fact that inflation is still present shows how closely the price (and, below it, the availability) of petrol affects the world economy. The picture for advanced countries is becoming more and more clouded by persistent and expanding inflationary pressures as well as aggressive tightening by central banks in response. Consumer and major customer industries, including the automobile and construction sectors, may have substantially declining demand for chemicals as a result of a persistent recession and continuous high inflation.

Investment in logistics services and infrastructure driving the market

- Due to growing device penetration, the average order value per transaction in the Singaporean e-commerce market will rise in the upcoming years. The transparency and security of the supply chain are predicted to improve with technological advancements, increasing cost-effectiveness. Additionally, in the upcoming years, commercial opportunities will be generated by the development of logistical infrastructures such as intermodal connectivity, logistics parks, and ports. The increase in the import and export of raw materials for food and mass-produced goods is the main reason fueling the expansion of the 3PL market in Singapore. The International Chamber of Shipping estimates that roughly 11 billion tonnes of cargo are transported annually on ships. Trade worldwide has significantly increased as a result of globalization. Machinery and transport equipment and petroleum are Singapore's major imports, while refined petroleum products are its largest exports. China, the United States, Indonesia, Malaysia, and Japan are the most important trading partners.

- It is challenging for manufacturers to keep track of supply operations due to market fluctuations. This is why 3PL is growing in significance. Additionally, the growth of international markets may help the sector even more. The market for 3PL usage will experience considerable growth throughout the projected period as firms increasingly view 3PL as a cost-effective option for importing and exporting goods. Due to ongoing labor shortages and supply chain issues, 3PLs have adopted automation and robotic technology to streamline operations across the whole lifecycle. Simultaneously, data-driven ordering, warehousing, and transportation technologies are being leveraged to enhance visibility and communication for consumers, brands, and logistics service providers. Thus, the 3PL market in Singapore is anticipated to show considerable growth due to the rising adoption of technology in logistics.

Singapore Chemical Logistics Industry Overview

The Singaporean chemical logistics market is highly fragmented, with a lot of local, regional, and global players. Some of the major players include ALPS Global Logistics, Koyo Kaiun Co., Ltd., Iino Singapore Pte Ltd, Fairfield Chemical Carriers, MCL Logistics Asia Pte Ltd, and many more. The sector has been observing many innovative and digital trends in recent years, like adopting big data analytics and IoT technologies to further fuel the growth of the chemical logistics industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Method

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Overview

- 4.3 Market Dynamics

- 4.3.1 Drivers

- 4.3.1.1 Increase demand of Petrochemical is driving the market

- 4.3.1.2 Increase in Investments is driving the market

- 4.3.2 Restraints

- 4.3.2.1 High Cost of Operations

- 4.3.3 Opportunities

- 4.3.3.1 Technological Innovations

- 4.3.1 Drivers

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Technological Innovations in the industry

- 4.7 Government Initiatives to Attract Investment in the Industry

- 4.8 Insights into the 3PL Market (Market Size and Forecast)

- 4.9 Impact of COVID - 19 on the Industry

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.2 Warehousing, Distribution, and Inventory Management

- 5.1.3 Other Services

- 5.2 By Mode of Transportation

- 5.2.1 Roadways

- 5.2.2 Railways

- 5.2.3 Airways

- 5.2.4 Waterways

- 5.2.5 Other Modes of Transportation

- 5.3 By End-User

- 5.3.1 Pharmaceutical

- 5.3.2 Cosmetic

- 5.3.3 Oil and Gas

- 5.3.4 Specialty Chemicals

- 5.3.5 Other End-Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 ALPS Global Logistics

- 6.2.2 Koyo Kaiun Co., Ltd.

- 6.2.3 Iino Singapore Pte Ltd

- 6.2.4 Fairfield Chemical Carriers

- 6.2.5 MCL Logistics Asia Pte Ltd

- 6.2.6 Tatsumi Marine (Singapore) Pte Ltd

- 6.2.7 MSR Green Corporation (S) Pte Ltd

- 6.2.8 Aurora Tankers Management Pte. Ltd.

- 6.2.9 Win-Bells Logistics & Services Pte. Ltd.

- 6.2.10 DHL

- 6.2.11 K" Line Pte Ltd"

- 6.2.12 Bertschi Singapore Pte Ltd.

- 6.2.13 Kaplan Logistics*