ドイツの医薬品倉庫:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Germany Pharmaceutical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1645033

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

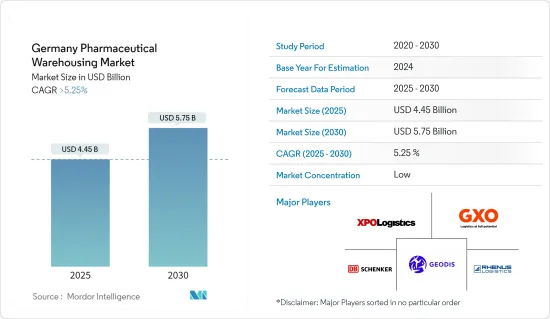

ドイツの医薬品倉庫の市場規模は2025年に44億5,000万米ドルと推定され、予測期間中(2025-2030年)のCAGRは5.25%を超え、2030年には57億5,000万米ドルに達すると予測されています。

ドイツの医薬品倉庫産業は、国内の医薬品物流ネットワークにおいて極めて重要な役割を果たしています。特に、ワクチンや生物製剤のような温度に敏感な品目向けの専用倉庫の需要が急増しています。2024年、コールドチェーン市場は急速に拡大し、前年比平均成長率は6%に迫る勢いです。ドイツ貿易投資総省(GTAI)の報告書によると、この成長には、温度管理された保管庫や冷蔵輸送網などの施設が含まれます。この成長は、国内外からの需要に応えるドイツの強固な物流インフラ、特にEUの厳しいGDP基準を満たす施設によって支えられています。

自動化や人工知能を含む技術の進歩は、ドイツにおける医薬品保管に変革をもたらしつつあります。ロボット工学と自動化システムの統合は、業務効率を高めるだけでなく、費用対効果も高めています。ドイツ物流協会の報告によると、医薬品需要の増加を受けて、医薬品倉庫では2024年から自動化の導入が年間15%増加すると予測されています。さらに、倉庫業務のスピードと一貫性を高めるために多額の投資が行われており、主要な物流センターでは、この分野によりよく対応するために最先端の技術が活用されています。

ドイツの医薬品倉庫に関する規制状況は、市場拡大の重要なきっかけとなっています。政府は、ドイツ医薬品法(Arzneimittelgesetz)やGDPのようなEU規制で規定されているように、厳格な基準を実施しています。これらの規制は、医薬品の安全性、綿密な温度管理、強固なトレーサビリティを重視しています。特に、2024年までに温度変化に敏感な医薬品が倉庫の総容量の20%以上を占めると予測されているため、コールドチェーンの遵守は重要な課題となっています。ワクチンや生物製剤に対する温度管理の義務化が進んでいることから、このような専門施設に対する需要は毎年8%増加すると予想されています。

ドイツの医薬品倉庫市場の動向

医薬品倉庫における自動化とAIの採用

医薬品倉庫部門では、自動化とAIの導入が急増し、業界の顕著な動向となっています。同時に、医薬品サプライチェーンの複雑さが増し、効率的で正確なオペレーションへの要求が高まっていることが、ドイツの物流企業にロボット工学とAI技術への多額の投資を促しています。これらの進歩は、人件費を削減するだけでなく、在庫管理、注文処理、規制遵守を強化します。

多くの大手医薬品倉庫は現在、仕分けやピッキング作業にAGVやロボットアームを活用し、迅速なターンアラウンドタイムと注文精度の向上を実現しています。ドイツの大手医薬品ロジスティクス企業の多くは、倉庫の最適化を目的としたAIシステムへの投資を表明しており、特に在庫追跡と予知保全に重点を置いています。

ドイツの医薬品倉庫部門では、近年AIが業務を再構築しています。2024年1月、ベーリンガーインゲルハイムは機械学習アルゴリズムを活用し、需要予測、在庫管理の合理化、特に温度に敏感な医薬品の無駄の削減を実現しました。同様に、2024年初頭には、メルクKGaAがAI主導の予測分析を採用し、在庫の監視と保管予測を即座に行うことで、医薬品規制の遵守を保証し、運用経費を削減しました。こうした開発は、ドイツの医薬品サプライチェーンにおける効率性の向上と規制遵守の確保において、AIの影響力が拡大していることを浮き彫りにしています。

特にワクチンや生物製剤のような温度に敏感な製品に関する厳しい規制要件は、自動化を推進する大きな原動力となっています。AIと自動化は、保管条件の正確な制御と温度や湿度などの環境要因のリアルタイム監視を提供することで、コンプライアンスを確保する上で極めて重要な役割を果たしています。さらに、ヒューマンエラーを最小限に抑えることで、これらの技術は医薬品の適切な取り扱いと輸送を保証します。業界筋によると、自動化された医薬品倉庫は、ドイツ企業によるこれらの先端技術の採用増加により、年率15%で拡大しています。高効率の業務に対する需要が高まっていることから、この動向は今後も続くと予想されます。

医薬品向けコールドチェーンロジスティクスの成長

コールドチェーンロジスティクスは、ドイツの医薬品保管事情における極めて重要な動向として浮上しています。生物製剤、ワクチン、その他の温度に敏感な医薬品に対する需要の急増は、特殊な低温貯蔵施設の緊急の必要性を強調しています。2024年までに、コールドチェーン・ストレージはドイツの医薬品倉庫の総容量の20%以上を占め、この分野は急成長を遂げています。この急成長の主な要因は、ワクチンと生物製剤の取扱量の増加であり、いずれも厳しい温度管理が要求されます。ある種のワクチンは-80℃という極寒での保管が必要だが、大半の生物製剤は2~8℃の範囲で管理されています。

この傾向は2024年まで続くだけでなく、新しい生物製剤やさらに温度の影響を受けやすい製品のイントロダクションよっても強化されています。コールドチェーンロジスティクスの拡大は、一般的な規制状況に大きな影響を受けています。例えば、欧州連合の適正流通規範とドイツのArzneimittelgesetzは、製薬会社に対し、温度に敏感な商品の安全な保管と輸送を義務付けています。

2023年後半、クーネ+ナーゲルはフランクフルトに新しい定温倉庫を開設し、ドイツにおけるコールドチェーンロジスティクス能力を強化しました。この施設は、温度変化に敏感な医薬品、特にワクチンや生物製剤の需要の高まりに対応するものです。この拡張は、EUの適正流通規範(GDP)ガイドラインに対するドイツのコミットメントに沿ったもので、これらの重要な製品の安全な保管と輸送を保証するものです。このイニシアチブは、医薬品ロジスティクスの専門知識を強化することにドイツが注力していることを浮き彫りにしています。

ドイツの医薬品倉庫業者は、厳しい基準を満たすため、リアルタイムの温度監視とデータ記録を備えた先進的なコールドチェーン施設に投資しています。ロジスティクス企業は需要の増加に対応するため、冷蔵倉庫の容量を増やしています。

ドイツの医薬品倉庫業界の概要

ドイツの医薬品倉庫市場は、世界企業とローカル企業が混在する断片的な市場です。輸出入製品のほとんどは、冷蔵輸送で監視する必要があります。ベンダーは市場での存在感を高めるため、戦略的提携、パートナーシップ、M&A、地理的拡大、製品・サービスの発売など、さまざまな戦略を実施しています。主なプレーヤーは、XPO Logistics Inc.、CDS Hackner GmbH、GXO Logistics、Wagner Group GmbHなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 製薬業界における品質と製品感度の重視の高まり

- 効率性と正確性を高めるための倉庫の自動化

- 市場抑制要因

- 効率的な物流サポートの欠如

- 熟練労働者の不足

- 市場機会

- 医薬品倉庫強化のための政府イニシアチブの台頭

- 医薬品の技術革新と開発の増加

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 地政学とパンデミックが市場に与える影響

第5章 市場セグメンテーション

- タイプ別

- コールドチェーン倉庫

- 非コールドチェーン倉庫

- 用途別

- 製薬工場

- 薬局

- 病院

- その他

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- Nippon Express

- Bio Pharma Logistics

- Rhenus SE and Co. KG

- ADAllen Pharma

- DB Schenker

- FedEx Corp.

- GEODIS SA

- CEVA Logistics

- Hellmann Worldwide Logistics SE and Co KG

- CDS Hackner GmbH

- Pfenning Logistics

- GXO Logistics

- Wagner Group GmbH

- Kuehne Nagel Management AG

- United Parcel Service Inc.

- XPO Logistics Inc.

- その他の企業

第7章 市場の将来

第8章 付録

- マクロ経済指標(GDP分布、活動別)

- 経済統計-運輸・倉庫業の経済への貢献

- 対外貿易統計-品目別、仕向地・原産地別輸出入額

目次

The Germany Pharmaceutical Warehousing Market size is estimated at USD 4.45 billion in 2025, and is expected to reach USD 5.75 billion by 2030, at a CAGR of greater than 5.25% during the forecast period (2025-2030).

Germany's pharmaceutical warehousing industry plays a pivotal role in the nation's pharmaceutical logistics network. The demand for specialized warehouses, particularly for temperature-sensitive items like vaccines and biologics, has surged. In 2024, the cold chain market is expanding swiftly, with an average year-on-year growth rate nearing 6%. This growth encompasses facilities like temperature-controlled storage units and refrigerated transportation networks, as highlighted in a report by Germany Trade & Invest (GTAI). This growth is bolstered by Germany's robust logistics infrastructure, which caters to both domestic and international demands, especially with facilities meeting stringent EU GDP standards.

Technological advancements, including automation and artificial intelligence, are transforming pharmaceutical storage in Germany. The integration of robotics and automated systems not only boosts operational efficiency but also enhances cost-effectiveness. The German Logistics Association reports that, in response to increasing demand for medicines, pharmaceutical warehouses are projected to see a 15% annual rise in automation adoption, beginning in 2024. Furthermore, significant investments are being channeled to enhance the speed and consistency of warehouse operations, with major logistics centers leveraging state-of-the-art technologies to better cater to the sector.

Germany's regulatory landscape for pharmaceutical warehousing is a crucial catalyst for market expansion. The government enforces stringent standards, as delineated in the German Medicines Act (Arzneimittelgesetz) and EU regulations like GDP. These regulations emphasize the safety of pharmaceutical products, meticulous temperature control, and robust traceability. Cold chain compliance poses a significant challenge, especially with temperature-sensitive pharmaceuticals projected to occupy over 20% of total warehouse capacity by 2024. Given the heightened temperature control mandates for vaccines and biologics, the demand for such specialized facilities is anticipated to grow by 8% annually.

Germany Pharmaceutical Warehousing Market Trends

Adoption of Automation and AI in Pharmaceutical Warehousing

The pharmaceutical warehouse sector witnessed a significant surge in the adoption of automation and AI, marking it as a prominent trend in the industry. At the same time, the rising intricacies of pharmaceutical supply chains, coupled with a heightened demand for efficient and precise operations, are prompting German logistics firms to invest heavily in robotics and AI technologies. These advancements not only curtail labor costs but also enhance stock management, order fulfillment, and adherence to regulations.

Many leading pharmaceutical warehouses now utilize AGVs and robotic arms for sorting and picking tasks, leading to quicker turnaround times and heightened order accuracy. Numerous major pharmaceutical logistics firms in Germany have pledged investments in AI systems aimed at warehouse optimization, particularly emphasizing inventory tracking and predictive maintenance.

In Germany's pharmaceutical warehousing sector, AI has been reshaping operations in recent years. In January 2024, Boehringer Ingelheim harnessed machine learning algorithms to forecast demand, streamline inventory management, and curtail wastage, especially for temperature-sensitive medications. Likewise, in early 2024, Merck KGaA employed AI-driven predictive analytics for immediate stock oversight and storage predictions, guaranteeing adherence to pharmaceutical regulations and cutting down operational expenses. These developments highlight AI's expanding influence in boosting efficiency and ensuring regulatory compliance in Germany's pharmaceutical supply chain.

Stringent regulatory requirements, especially concerning temperature-sensitive products like vaccines and biologics, significantly drive the push for automation. AI and automation play a pivotal role in ensuring compliance by providing precise control over storage conditions and real-time monitoring of environmental factors such as temperature and humidity. Moreover, by minimizing human error, these technologies ensure the proper handling and transportation of medications. Industry sources indicate that automated pharmaceutical warehouses are expanding at an annual rate of 15%, driven by the increasing adoption of these advanced technologies by German firms. Given the escalating demand for high-efficiency operations, this trend is expected to persist.

Growth in Cold Chain Logistics for Pharmaceuticals

Cold chain logistics emerges as a pivotal trend in Germany's pharmaceutical storage landscape. The surging demand for biologic pharmaceuticals, vaccines, and other temperature-sensitive medications underscores the urgent need for specialized cold storage facilities. By 2024, cold chain storage has claimed over 20% of Germany's total pharmaceutical warehouse capacity, with the sector witnessing rapid growth. This surge is predominantly fueled by the increasing volume of vaccines and biologics, both of which demand stringent temperature controls. While certain vaccines necessitate storage at a frigid -80°C, the majority of biologics are maintained within a 2 to 8°C range.

The urgency for these facilities was amplified by the pressing demands of COVID-19 vaccine distribution, a trend that has not only persisted into 2024 but has also been bolstered by the introduction of new biologics and even more temperature-sensitive products. The expansion of cold chain logistics is heavily influenced by the prevailing regulatory landscape. For instance, both the European Union's Good Distribution Practice standards and Germany's Arzneimittelgesetz mandate that pharmaceutical companies ensure the safe storage and transport of temperature-sensitive goods.

In late 2023, Kuehne + Nagel strengthened its cold chain logistics capabilities in Germany by opening a new temperature-controlled warehouse in Frankfurt. This facility addresses the rising demand for temperature-sensitive pharmaceuticals, notably vaccines and biologics. The expansion aligns with Germany's commitment to the EU Good Distribution Practice (GDP) guidelines, ensuring the secure storage and transportation of these essential products. This initiative highlights Germany's focus on bolstering its pharmaceutical logistics expertise.

German pharmaceutical warehouse providers are investing in advanced cold chain facilities with real-time temperature monitoring and data recording to meet stringent standards. Logistics companies are increasing cold storage capacities to meet rising demand.

Germany Pharmaceutical Warehousing Industry Overview

The Germany Pharmaceutical Warehousing market is fragmented in nature, with a mix of global and local players. Most of the imports and exports products need to be monitored in refrigerated transports. Vendors are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. Major players include XPO Logistics Inc., CDS Hackner GmbH, GXO Logistics, and Wagner Group GmbH.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased focus on quality and product sensitivity in the pharma industry

- 4.2.2 Automation at warehouses to increase efficiency and accuracy

- 4.3 Market Restraints

- 4.3.1 Lack of efficient logistics support

- 4.3.2 Shortage of skilled labor

- 4.4 Market Opportunities

- 4.4.1 Rise in government initiatives to enhance Pharmaceutical Warehousing

- 4.4.2 Increasing Pharmaceutical product innovation and Development

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Cold Chain Warehouse

- 5.1.2 Non-Cold Chain Warehouse

- 5.2 By Application

- 5.2.1 Pharmaceutical Factory

- 5.2.2 Pharmacy

- 5.2.3 Hospital

- 5.2.4 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Nippon Express

- 6.2.2 Bio Pharma Logistics

- 6.2.3 Rhenus SE and Co. KG

- 6.2.4 ADAllen Pharma

- 6.2.5 DB Schenker

- 6.2.6 FedEx Corp.

- 6.2.7 GEODIS SA

- 6.2.8 CEVA Logistics

- 6.2.9 Hellmann Worldwide Logistics SE and Co KG

- 6.2.10 CDS Hackner GmbH

- 6.2.11 Pfenning Logistics

- 6.2.12 GXO Logistics

- 6.2.13 Wagner Group GmbH

- 6.2.14 Kuehne Nagel Management AG

- 6.2.15 United Parcel Service Inc.

- 6.2.16 XPO Logistics Inc.*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to Economy

- 8.3 External Trade Statistics - Exports and Imports by Product and by Country of Destination/Origin

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日