|

市場調査レポート

商品コード

1687992

倉庫・保管サービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Warehousing and Storage Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 倉庫・保管サービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

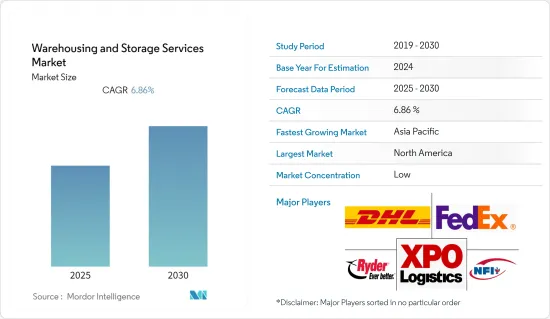

倉庫・保管サービス市場は予測期間中にCAGR 6.86%を記録すると予想されます。

産業部門の成長、製造製品、加工食品、冷凍食品の需要増加、eコマース産業の拡大などが、倉庫・保管サービスの需要を促進する大きな要因となっています。

主要ハイライト

- 倉庫・保管サービスは、部品、設備、車両、製品、生鮮品など、他の企業や組織の所有物の保管を記載しています。オムニチャネルモデルへの需要の高まりが市場を牽引すると予想されます。顧客はオンライン購入の傾向を受け入れてはいるもの、オフライン店舗は依然として大きな市場シェアを占めており、特に家具などの大口商品セグメントでは倉庫・保管市場を拡大しています。

- サプライチェーンがこれまで以上に迅速に需要に対応できるよう再構築される中、物流サービスがこのプロセスで重要な役割を果たすため、倉庫はますます物流を統合するようになっています。さらに、世界の動向がその範囲をさらに拡大するにつれて、世界に事業を展開する産業の在庫のかなりの部分は、サプライチェーンを通じて完成品を移送するために海外から倉庫に頻繁に納入されるようになっており、このことも倉庫・保管サービスの需要を促進しています。

- 需要の増加と新しいタイプの製品を保管するための要件は、倉庫サービスプロバイダの複雑さに大きな影響を与えており、彼らは現在、複雑さを軽減し、施設をよりよく管理するためのツールを提供するのに役立つ革新的な技術を探し始めています。例えば、倉庫システムはそのようなソリューションの1つで、企業の在庫全体に対する可視性を提供し、配送センターから店舗の棚に至るまで、サプライチェーンのフルフィルメント業務を行っています。

- さらに、倉庫/保管サービスプロバイダは、配送品質を確保しながら配送時間をさらに短縮するため、バッチ処理、ハンドリング、ピッキングプロセスの最適化にも注力しています。こうした動向は、新たな倉庫建設・管理技術の開発を促進します。さらに、世界の参入企業に対抗するため、多くのベンダーが倉庫業務にGPS、RFID、VoIP機器、デジタル音声、画像技術などの新技術を採用しています。

- しかし、倉庫の設置や先端技術の導入に必要な投資がかさむことは、倉庫・保管サービス業者が直面する大きな課題のひとつです。さらに、中小企業の認識不足や世界の共通規格も市場の成長に課題を与えています。

- COVID-19の結果、多くの倉庫がこれまで以上に忙しく稼働し、主に食品、医薬品、生活必需品に対応しています。Amazon、Aldi、Asda、Lidlの各社はこぞって、キャパシティを拡大し、倉庫従業員を増員する必要性を報告しています。一部のセクタ、特に工業・製造業領域では、特に初期段階において需要が減少したもの、市場は今後数年で徐々に回復すると予想されます。

冷蔵・冷凍倉庫市場の動向

冷蔵倉庫・保管部門が大きく成長

- 冷蔵倉庫・保管施設は、保管のために冷蔵管理された部屋を必要とする製品を扱う。また、腐敗しやすい製品を低温で保管・貯蔵する場所でもあります。これらの冷蔵倉庫や冷蔵倉庫のほとんどは、最適な条件内でアイテムを保つことができる特性を持つように設計されています。冷蔵倉庫・貯蔵産業の事業所は、テンパリング、ブラスト冷凍、改良雰囲気貯蔵サービスなどのサービスを提供しています。

- 冷蔵倉庫・貯蔵は、主に製薬や飲食品セグメントで市場成長への前向きな動向を見せています。Care Quality Commission(医療の質委員会)は、医薬品の有効性を維持するため、インシュリン、抗生物質液、注射薬、目薬、一部のクリームは20℃~80℃で保管することを推奨しています。米国国勢調査局によると、2021年には1億1,745万人の米国人が目薬や洗眼薬を使用していました。この数字は2023年には1億1,849万人に増加すると予測されています。特にパンデミック後の液体医薬品需要の増加は、市場の成長にプラスの影響を与えると予想されます。

- 冷蔵保管は、温度に敏感な製品を輸送・保管する際のサプライチェーンマネジメント(SCM)に不可欠です。また、北米自由貿易協定(NAFTA)のような二国間自由貿易協定によって、米国のベンダーが輸入関税を最小限に抑えて生鮮食品の取引を拡大できるようになり、新たな機会が生まれています。このような貿易協定は市場の成長に有利です。

- 冷蔵倉庫に対する需要の高まりを考慮し、同市場で事業を展開するベンダーは継続的に足跡の拡大に注力しています。例えば、国際冷蔵倉庫協会(IARW)によると、リネージュロジスティクスは北米地域で最も大規模な冷蔵倉庫ロジスティクスプロバイダであり、4,252万6,060立方メートルの温度管理スペースを有しています。

北米が大きなシェアを占める見込み

- 北米地域の倉庫ロジスティクス市場を牽引する要因もいくつかあります。流通業者や小売業者向けに原料や完成品を保管するロジスティクスニーズが増加しており、製造業各社が生産・業務拡大に注力するために倉庫サービスをアウトソーシングするケースが増えています。さらに、業務効率の向上とコスト削減により、荷送人は倉庫サービスプロバイダにロジスティクス業務を委託するようになっています。

- AmazonやWalmartといった小売・eコマース大手の存在は、この地域の倉庫・保管サービス需要に大きく貢献しています。Walmartによると、2022年現在、同社は31のeコマース専用フルフィルメントセンターと、米国人口の90%から10マイル以内にある4,700の店舗を使ってオンライン注文に対応しています。

- 米国のAmazonの販売者を対象とした調査によると、上流の倉庫・配送業務における販売者の3大苦悩は、複雑な料金体系、保管料の高さ、保管容量の不足でした。こうした課題に対処するため、ベンダーはより多くの顧客を惹きつける新たなビジネス戦略の開発にますます力を注いでいます。例えば、Amazonは2022年9月、販売者が大量の在庫保管と自動化された流通のために新たに建設された専用施設を利用できるようにする新サービスを発表しました。

- 製造、小売、製薬部門の著しい成長により、市場は米国で潜在的な成長を示しています。米国商務省によると、米国の倉庫・保管産業の売上高は2021年に5,049万米ドルに増加します。ベンダーは継続的に施設の拡大に注力しているため、こうした動向はさらに拡大すると予想されます。

- さらに、北米地域は新技術をいち早く採用する地域であるため、新しい倉庫・保管技術の採用率は引き続き高いと予想されます。さらに、必要とされるインフラ、意識の高まり、熟練労働力の利用可能性なども、こうした動向を支える重要な要因です。

倉庫・保管サービス産業概要

倉庫・保管サービス市場は、主に複数の参入企業が存在することから競合が激しくなっています。参入障壁が比較的低いため、競合の激化が予想されます。長期的なパートナーシップ、合併、買収、倉庫ソフトウェアへの高額投資は、競争の激化を維持するために企業が採用する主要な成長戦略です。同市場で事業を展開する主要企業には、DHL International Gmbh、XPO Logistics Inc.、FedEx Corp.などがあります。

- 2022年9月-大手コントラクトロジスティクスプロバイダであるGXO Logistics Inc.は、Bayerと新たな倉庫施設を開設。GXOは、ネブラスカ州カーニーに35万平方フィートの新施設を開設し、共有スペース型物流ネットワークGXOダイレクトを通じて、Bayerのクロップサイエンス部門のすべての入出荷業務を含む倉庫サポートを管理します。

- 2022年5月-温度管理された物流センターを開発・運営するVertical Cold Storageは、US Cold Storageからフロリダ州、ネブラスカ州、ノースカロライナ州にある3つの公共冷蔵倉庫を買収。同社は、鶏肉、食肉、鶏肉、魚介類など、拡大するタンパク質事業をサポートするため、これらの買収を実施。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- オムニチャネル流通の人気の高まり

- eコマース産業の成長

- 市場抑制要因

- 高い投資とメンテナンスコスト

第6章 市場セグメンテーション

- タイプ別

- 一般倉庫・保管

- 冷蔵倉庫

- 農産物倉庫・貯蔵

- 所有者別

- 個人倉庫

- 公共倉庫

- 保税倉庫

- エンドユーザー産業別

- 製造業

- 消費財

- 飲食品

- 小売

- 医療

- その他

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- DHL International GmbH

- XPO Logistics Inc.

- Ryder System Inc.

- NFI Industries Inc.

- AmeriCold Logistics LLC

- FedEx Corp

- Lineage Logistics Holding LLC

- NF Global Logistics Ltd

- APM Terminals BV

- DSV Panalpina AS

- Kane Is Able Inc.

- MSC-Mediterranean Shipping Agency AG

第8章 投資分析

第9章 市場の将来展望

The Warehousing and Storage Services Market is expected to register a CAGR of 6.86% during the forecast period.

The growth of the industrial sector, increasing demand for manufactured products, processed and frozen food products, and the expansion of the e-commerce industry are among the significant factors driving the demand for warehousing and storage services.

Key Highlights

- Warehousing and storage services provide storage for another company or organization's property, including parts, equipment, vehicles, products, and perishable goods. The increasing demand for an omnichannel model is expected to drive the market. Although customers embrace the online buying trend, offline stores still hold a significant market share, especially in the big-ticket products segment, such as furniture, which expands the warehouse and storage market.

- With supply chains being reconfigured to meet demand faster than ever, warehouses are increasingly integrating logistics, as logistics services play a crucial role in this process. Additionally, with the globalization trend further expanding its scope, a significant portion of the inventory of industries that operate globally is delivered frequently from abroad to a warehouse to transfer finished goods through the supply chain, which in turn is also driving the demand for warehouse and storage services.

- The growth in demand and requirement to store new product types have significantly impacted the complexity of the warehouse service providers, who now have started to look for innovative technologies that can help them reduce the complexity and provide them with tools to manage the facility better. For instance, Warehouse Management System is one such solution that offers visibility into a business' entire inventory and works supply chain fulfillment operations from the distribution center to the store shelf.

- Furthermore, warehousing/storage service providers are also focusing on optimizing their batching, handling, and picking processes to enhance delivery times further while ensuring the quality of delivery. Such trends facilitate the development of new warehouse construction and management techniques. Additionally, to compete with global players, many vendors are adopting emerging technologies, such as GPS, RFID, VoIP devices, digital voice, and imaging technology for warehouse operations.

- However, the higher investment required to set up warehouses and adopt advanced technologies is among the significant challenges warehouse/storage service providers face. Furthermore, a lack of awareness among SMEs and common global standards also challenges the market's growth.

- COVID-19 resulted in many warehouses running busier than ever, mainly catering to food products, pharmaceuticals, and essential household goods. Amazon, Aldi, Asda, and Lidl have all reported a need to increase their capacities and hire an additional warehouse workforce. Although in some sectors, especially in the industrial and manufacturing domain, the demand declined, especially during the initial phase, the market is expected to recover gradually in the coming years.

Warehousing and Storage Market Trends

The Refrigerated Warehousing and Storage Segment to Grow Significantly

- The refrigerated warehousing and storage facilities deal with products that require refrigerated and controlled rooms for storage. It also refers to where perishable products are stored or kept at low temperatures. Most of these cold storage rooms or refrigerated warehouses are designed with properties that can keep the items within optimum conditions. Establishments in the refrigerated warehousing and storage industry provide services, such as tempering, blast freezing, and modified atmosphere storage services.

- Refrigerated warehousing and storage are showing positive trends toward market growth, mainly in the pharma and food and beverage sectors. The Care Quality Commission recommends that insulins, antibiotic liquids, injections, eye drops, and some creams must be stored between 20C and 80C to maintain the effectiveness of the medicines. According to the U.S. Census Bureau, 117.45 million Americans used eye drops and eyewash in 2021. This figure is projected to increase to 118 .49 million in 2023. The increasing demand for liquid pharmaceutical products, especially after the pandemic, is expected to impact the market's growth positively.

- Refrigerated storage is integral to Supply Chain Management (SCM) when transporting and storing temperature-sensitive products. New opportunities are also being created by bilateral free trade agreements, such as the North America Free Trade Agreement (NAFTA), which allows vendors in the United States to increase the trading of perishable food products with minimal import duties. Such trade agreements favor the market's growth.

- Considering the growing demand for cold storage warehouses, the vendors operating in the market continuously focus on expanding their footprint. For instance, according to the International Association of Refrigerated Warehouses (IARW), Lineage Logistics was the most extensive refrigerated warehousing and logistics provider in the North American region, with 42,526.06 thousand cubic meters of temperature-controlled space.

North America is Expected to Hold a Major Share

- Several factors also drive the warehousing and storage market in the North American region. An increase in logistics needs for storing raw materials and finished goods for distributors and retailers has been growing as manufacturing companies increasingly outsource warehousing services to focus on productional and operational expansions. Additionally, enhanced operational efficiency and cost savings encourage shippers to outsource the logistics portion of their activities to warehouse service providers.

- The presence of retail and e-commerce giants, such as Amazon and Walmart contributes significantly to the region's demand for warehouse and storage services. According to Walmart, as of 2022, the company uses 31 dedicated e-commerce fulfillment centers and 4,700 stores within 10 miles of 90% of the U.S. population to fulfill online orders.

- According to a survey of U.S. Amazon sellers, the three most significant pain points for sellers in upstream warehousing and distribution operations were complicated fee structures, high prices for storage, and insufficient storage capacity. To address these challenges, vendors are increasingly focusing on developing new business strategies to attract more customers. For instance, in September 2022, Amazon announced new services to enable sellers to use new, purpose-built facilities for bulk inventory storage and automated distribution.

- With significant growth in the manufacturing, retail, and pharma units, the market shows potential growth in the United States. According to the U.S. Department of Commerce, the U.S. warehousing and storage industry's revenue increased to USD 50.49 million in 2021. With vendors continuously focusing on expanding their facilities, such trends are only expected to grow further.

- Furthermore, the adoption rate of new warehouse and storage technologies is expected to remain high in the North American region as the region is among the early adopters of new technologies. Additionally, the required infrastructure heightened awareness, and availability of a skilled workforce are other significant factors supporting such trends.

Warehousing and Storage Industry Overview

The warehousing and storage services market is competitive, mainly because of the presence of several players. The competition is expected to intensify because of the relatively low entry barriers. Long-term partnerships, mergers, acquisitions, and high investments in warehouse management software are the prime growth strategies adopted by companies to sustain the growing competition. Some major players operating in the market include DHL International Gmbh, XPO Logistics Inc., and FedEx Corp, among others.

- September 2022 - GXO Logistics Inc., a leading pure-play contract logistics provider, opened a new warehouse facility with Bayer. GXO will manage warehouse support, including all shipping and receiving activities, for Bayer's Crop Science division through its shared-space distribution network GXO Direct at the new 350,000-square-foot facility in Kearney, Nebraska.

- May 2022 - Vertical Cold Storage, a developer, and operator of temperature-controlled distribution centers acquired three public refrigerated warehouses in Florida, Nebraska, and North Carolina from US Cold Storage. The company made these acquisitions to support its expanding protein business, including poultry, meat, poultry, and seafood.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Popularity of Omnichannel Distribution

- 5.1.2 Growth in the E-commerce Industry

- 5.2 Market Restraints

- 5.2.1 High Investment and Maintenance Costs

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 General Warehousing and Storage

- 6.1.2 Refrigerated Warehousing and Storage

- 6.1.3 Farm Product Warehousing and Storage

- 6.2 By Ownership

- 6.2.1 Private Warehouses

- 6.2.2 Public Warehouses

- 6.2.3 Bonded Warehouses

- 6.3 By End-user Industry

- 6.3.1 Manufacturing

- 6.3.2 Consumer Goods

- 6.3.3 Food and Beverage

- 6.3.4 Retail

- 6.3.5 Healthcare

- 6.3.6 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 DHL International GmbH

- 7.1.2 XPO Logistics Inc.

- 7.1.3 Ryder System Inc.

- 7.1.4 NFI Industries Inc.

- 7.1.5 AmeriCold Logistics LLC

- 7.1.6 FedEx Corp

- 7.1.7 Lineage Logistics Holding LLC

- 7.1.8 NF Global Logistics Ltd

- 7.1.9 APM Terminals BV

- 7.1.10 DSV Panalpina AS

- 7.1.11 Kane Is Able Inc.

- 7.1.12 MSC - Mediterranean Shipping Agency AG