|

市場調査レポート

商品コード

1644471

米国のプリントラベル:市場シェア分析、産業動向、統計、成長予測(2025~2030年)United States Print Label - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のプリントラベル:市場シェア分析、産業動向、統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

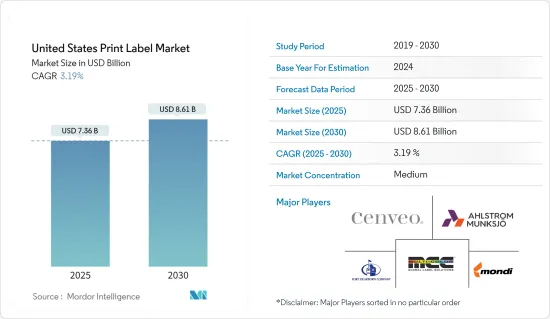

米国のプリントラベル市場規模は2025年に73億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.19%で、2030年には86億1,000万米ドルに達すると予測されます。

主なハイライト

- COVIDの流行は、ラベリングにデジタル印刷の機会を提供しています。ラベルは必需品のサプライチェーンの一部です。また、情報を伝達するための重要なツールでもあります。そのため、市場は食品、衛生、医薬品ラベル、eコマース販売に関連するラベリング情報の需要の増加を目の当たりにしています。米国ラベル業界は、発生当初の1ヶ月間、重要な役割を果たしました。米国のラベルコンバーターは、COVID-19の発生時に需要の高かった印刷製品を納品しました。

- デジタル技術は、潜在的な消費者の購買意欲を高める魅力的なラベルデザインの開発において、様々なエンドユーザー業界の複数の要求に応えてきました。デジタル技術と既存のラベル印刷技術との統合は、小規模から大規模のすべての分野に大規模な変化をもたらし、市場全体を改善すると期待されています。

- さらに、フレキソ印刷が国内のプリントラベル市場を牽引すると予想されます。自動化が進むにつれ、顧客はできるだけ注文時間に近い製品を求めています。需要に応えるためには、これまで以上に迅速な納期が不可欠になっています。フレキソ印刷機は、連続印刷ソリューション、印刷機や技術へのより多くのソフトウェア統合、耐久性を備えており、より短いリードタイムで顧客の需要を満たすことができます。

- ロールフィードの高速印刷技術であるフレキソ印刷は、ほとんどのパッケージングやラベルの用途に適しています。このフレキソ印刷の最も優れた点は、さまざまな製品に素早く、手頃な価格で、優れた品質でラベルを印刷できることです。フレキソ印刷版は、ゴムやその他の柔軟な素材に希望のイメージを立体的に浮き彫りにすることで、フレキソ印刷を作成します。品質、生産性、柔軟性の優れた組み合わせにより、フレキソ印刷はプリントラベル業界で最も人気のある印刷世代となっています。

- プリントラベルは、ほぼすべてのサイズや数量でのオンデマンド印刷に起因する柔軟なパッケージングを通じて、製品の安全性とプロモーションにおいて非常に重要です。高度なフレキソ印刷技術により、ブランドオーナーは効率的に製品のプロモーションを行い、原産地や重要な栄養データ、さらには製品リコールのための重要な追跡データなど、製品に関する情報を発信することができます。

- フレキソ印刷は低コストであるため、そのプラットフォームはますます市場に参入しています。また、パーソナライズされた限定印刷ラベリングの作成も魅力的になっています。フレキソ印刷は、(固形ではなく)柔軟な版を使用する印刷技術です。凸版印刷の新しい形です。

- ラベルのコンバーティングプロセスを向上させることは、技術の最新の進歩に追いつくことが難しいため、継続的で厳しい作業です。UV LED硬化技術は、様々な印刷工程における重要なブレークスルーとして登場しました。現在では、ラベル、タグ、軟包装、シュリンクスリーブ包装用途のナローウェブフレキソ印刷やオーバープリントニス加工に大きな利点をもたらしています。

- UV硬化型インキは印刷性能を高めるだけでなく、マイグレーションに対応しているため、UVフレキソ食品包装やラベル用途に理想的です。サンケミカルは最近、高顔料、低粘度、多目的のUVフレキソベース濃縮物であるSolarVerseを発売しました。

- さらに、紙フィルムはフィルムに比べて耐久性に劣る傾向があり、塗布工程で適切な注意を払わないと、時間の経過とともに破れたりしわが寄ったりする可能性があります。しかし、環境規制に関するラベリングもプリントラベル市場の成長を妨げます。リサイクル時にラベルが品物に残っていると、その品物のリサイクル性が阻害されます。例えば、ラベル付き段ボール箱がリサイクルされる際、湿潤強度の高い紙ラベルは箱のリサイクルを妨げないが、湿潤強度の高い紙の代わりにフィルムが使用された場合、ラベルはリサイクルされなかった可能性があります。

米国のプリントラベル市場動向

感圧ラベルが最大の市場シェアを占める

- 感圧ラベル(PSL)は、ライナー、リリースコート、粘着剤、フェースストック、トップコートの5層からなり、ハイテクステッカーに似ています。PSLは、紙、フィルム、箔を主なラベル素材として使用することができ、シャープで鮮やかな色を出すために幅広い種類のインクを使用することができます。

- PSLは、熱、溶剤、水を一切必要とせず、製品表面に軽く、または適度な圧力を加えるだけで貼付できるため、最も広く使用されているラベルアプリケーターの一つです。リソース・ラベル・グループと全子会社によると、PSLは市場のラベル全体の80%以上を占めています。

- 伝統的なビールラベルの世界のような競争の激しい市場では、ラベルを群衆や競合から際立たせるための最も重要な要因の1つは、ユニークな外観と感触を持つことです。そのため、従来の湿式のりラベルは、さまざまな装飾の可能性と優れた外観のため、感圧ラベルやスリーブに急速に取って代わられつつあります。

- 従来のビールラベルの世界では、特に大規模で長持ちする仕事では、非常に費用対効果が高いため、湿式糊ラベルが好まれています。一方、より多くの装飾を施せば、混雑した棚で目立つラベルが注目される可能性が高くなります。ウェットグルーラベルの具体的かつ効果的な代替手段は、感圧ラベルです。感圧ラベルは、より優れた粘着特性と、メタリック効果のある裏刷りミラーソリューションでより多くの装飾オプションを提供します。米国で事業展開している企業は、変化する市場ニーズに応えることに注力している理由です。

- 感圧ラベルは、食品・飲料、医薬品、消費財、パーソナルケア、建設業界で使用されています。これらの業界にサービスを提供するベンダーは、重要な消費財やヘルスケア製品向けのラベル素材を生産・供給し続けるため、最前線で取り組んでいます。しかし、競争の激化や印刷・加飾技術の進化と相まって、原材料価格は上昇しています。

飲料が大きな市場シェアを占める見込み

- 飲料は、米国のプリントラベル市場にとって主要なエンドユーザー産業の1つです。これは、飲料分野での革新的なラベルやパッケージングの採用率が高いことと、健康飲料分野の市場が拡大していることによる。

- 重要な飲料カテゴリーの売上高は、2024年までに1,700億米ドルを超えると予想されています。国内ではパンデミック時に一部の飲料セグメントの消費が影響を受けたが、COVID-19の流行により多くのセグメントの範囲が拡大しました。

- さらに、同国には最大手の炭酸飲料企業があり、エナジードリンクの市場も好調で、顧客を惹きつけるために新しいパッケージング技術を採用する企業が増えています。米国の消費者の間で健康への関心が高まっているため、これらの企業はラベルに成分を印刷するようになっており、印刷の範囲が広がっています。また、これらの成分はブランドや特定のエナジードリンク製品によって異なる場合があります。

- ワイン市場の成長に伴い、ラベルの必要性は極めて重要になってきています。ワイン・ラベルのほとんどは、紙ラベル風か、フィルム・ラベルによるラベルなし風を使用しています。さらに、ラベルは、出荷、保管、使用される環境に耐えるように設計される必要があります。したがって、国内のワイナリーの増加は、ラベル印刷と製造の拡大にもつながります。

- ラベリングのサプライチェーンにおいて持続可能性が存在感を増すにつれ、リサイクル素材やリサイクル可能な素材の使用が増えると思われます。素材としては、PET、バイオプラスチック、再利用可能な厚手のガラスなどが有力な選択肢となると思われます。ラベリングサプライチェーンにおいて持続可能性がより重要になるにつれ、リサイクル可能なラベル素材の使用が増えると思われます。さらに、エイブリー・デニソンは、PETボトルリサイクル用のCleanFlake粘着技術、ClearCut粘着技術、飲料ラベリング用途の様々な紙やフィルムのフェイスストックなど、持続可能性のためのいくつかの技術を推進しています。

- 飲料の容器は、その後の粘着剤の選択も左右します。調査によると、ガラス容器はプラスチック容器とは異なる接着剤を必要とします。紙とポリプロピレンが飲料ラベルに使用される最も一般的な2つの素材であり、ポリプロピレン基材を採用するものがほとんどです。同国では飲料産業の拡大が進んでおり、飲料用ラベルのアップグレードも進んでいることから、同国の市場需要が高まっています。

- さらに、米国ベンダーはラベルソリューションの充実とブランド認知度向上のため、提携・買収戦略に投資しています。例えば、米国のフォート・ディアボーン社は、カット&スタックラベル、ロールフェッドラベル、シュリンクスリーブラベルの主要サプライヤーであるウォール・コーポレーション社を買収しました。この買収により、同社は主に食品、飲食品、家庭用品セグメント向けの米国におけるプリントラベルソリューションでさらなる成長を遂げました。

米国のプリントラベル産業の概要

米国のプリントラベル市場は、国内外に多数の大小プレーヤーが存在するため、適度に集中しています。プレーヤーは、製品革新、戦略的パートナーシップ、事業拡大、M&Aなどの主要戦略を採用しています。市場開拓の主な発展には次のようなものがある:

- 2023年3月米国のグラフィック・コミュニケーション企業Taylor社は、メキシコのモンテレイに新しいラベル製造施設を開設すると発表しました。直近の開設は、メキシコの産業企業による長持ちするラベルへの需要の高まりに対応する上で、事業をさらに支援することになります。

- 2023年10月All4Labelsはメキシコシティにあるより大きな施設に移転し、メキシコと米国での存在感を高めるための素晴らしい拡張計画の一環として、多数の新技術を導入中です。Almirall社によると、感圧ラベルとシュリンクスリーブを中心とした5つの新しい印刷ラインにより、同施設の生産能力は3倍になります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- デジタル印刷技術で製造されたラベルの需要拡大

- ヘルスケアと化粧品セグメントからの高い採用率

- 市場の課題

- 過酷な気候条件に耐える製品の不足

- エコシステム分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の米国のプリントラベル市場への影響評価

第5章 市場セグメンテーション

- 印刷工程別

- オフセットリソグラフィー

- グラビア

- フレキソ印刷

- スクリーン

- 凸版印刷

- 電子写真

- インクジェット

- ラベルフォーマット別

- 湿接着ラベル

- 感圧ラベル

- ライナーレスラベル

- マルチパートトラッキングラベル

- インモールドラベル

- シュリンク&ストレッチスリーブ

- エンドユーザー産業別

- 食品

- 飲料

- ヘルスケア

- 化粧品

- 家庭用

- 産業(自動車、工業用化学品、耐久消費財・非耐久消費財)

- 物流

- その他のエンドユーザー産業

第6章 競合情勢

- 企業プロファイル

- Fort Dearborn

- Multi Color Corporation

- Mondi Group

- Ahlstrom-munksjo Oyj

- Cenveo Corporation

- Avery Dennison Corporation

- Brady Corporation

- Westrock Company

- R.R. Donnelley & Sons Company

- Taylor Corporation

第7章 市場の将来展望

The United States Print Label Market size is estimated at USD 7.36 billion in 2025, and is expected to reach USD 8.61 billion by 2030, at a CAGR of 3.19% during the forecast period (2025-2030).

Key Highlights

- The COVID pandemic has provided opportunities for digital printing in labeling. Labels are part of the supply chains of necessities. Additionally, they serve as an essential tool for conveying information. Hence, the market has witnessed an increased demand for food, hygiene, pharmaceutical labels, and labeling information related to e-commerce sales. Short runs on a regular and increasing basis have become the norm.The United States label industry played a key role in the initial month of the outbreak. The label converters in the US delivered printed products that were in high demand during the COVID-19 outbreak.

- Digital technology has met the multiple requirements of various end-user industries in developing attractive label designs to encourage potential consumers to make purchases. The integration of digital technology with the existing label printing techniques is expected to bring a massive change to all the small-scale and large-scale sectors, improving the overall market.

- Moreover, flexography printing is expected to drive the print label market in the country. With the rise in automation, customers want their products as close to the order time as possible. Faster turnaround times are becoming more vital than ever to meet demand. Flexographic printer with continuous print solutions, more software integrations into the presses and technologies, and durability would meet customer demand in shorter lead times.

- Flexography, a roll-feed high-speed printing technique, is appropriate for most packaging and label applications. The best thing about this flexography is that it makes it possible to print labels on a wide range of products quickly, affordably, and with excellent quality. A flexible printing plate creates a flexographic print by creating a three-dimensional relief of the desired image in rubber or another flexible material. Due to its excellent combination of quality, productivity, and flexibility, flexographic printing has become the most popular print generation in the print label industry.

- Print Labels is crucial in product safety and promotions through flexible packaging attributed to on-demand printing in almost any size or quantity. Advanced flexographic printing techniques enable brand owners to efficiently promote their products and transmit information about them, including their origin, crucial nutritional data, and even crucial tracking data for a product recall.

- Due to the lower cost of flexo printing, its platforms have increasingly entered the market. Creating personalized, limited-run print labeling has also grown more appealing. Flexography is a printing technique that uses a flexible (rather than a solid) plate. It is a newer incarnation of relief printing.

- Enhancing the process of label converting is a continuous and demanding task due to the difficulty in keeping pace with the latest advancements in technology. UV LED curing technology has emerged as a significant breakthrough in various printing processes. It now provides significant advantages for narrow web flexographic printing and overprint varnishing for labels, tags, flexible packaging, and shrink-sleeve packaging applications.

- Apart from enhancing printing performance, UV cured inks are migration-compliant and, hence, ideal for UV flexo food packaging and label applications. Sun Chemical recently launched SolarVerse, a range of highly pigmented, low viscosity, multipurpose UV flexo base concentrates that are ideal for labeling food materials.

- Moreover, paper film stocks tend to be less durable than films, potentially ripping or wrinkling over time if proper care is not taken during the application process. However, labeling about environmental regulation will also hinder the growth of the print label market. If a label remains on an item during recycling, it will hinder the recyclability of the item. For example, when labeled corrugated boxes are recycled, wet strength paper labels do not hinder box recycling, but if the film is used instead of wet strength paper, the label could not have been recycled.

United States Print Label Market Trends

Pressure-sensitive Labels Accounts for the Largest Market Share

- Pressure-sensitive labels (PSL) consist of five individual layers, such as liner, release coat, adhesive, face stock, and topcoat, and are analogous to a high-tech sticker. A PSL can use paper, film, and foil as its primary label materials and can be used with a wide range of inks to produce sharp and bright colors.

- The PSL is one of the most widely used forms of label applicator, as it does not require any heat, solvent, or water to activate; it only takes light or moderate pressure to apply it to a product surface. According to the Resource Label Group and all subsidiaries, PSLs constitute more than 80% of all labels in the market.

- In a highly competitive market like the traditional world of beer labeling, one of the most important factors in making a label stand out from the crowd and the competition is having a unique look and feel. For this reason, traditional wet glue labels are quickly being replaced by pressure-sensitive labels or sleeves because of the various embellishment possibilities and the superior appearance.

- The traditional beer labeling world prefers wet glue labels because they are very cost-effective, especially for large-scale, long-lasting jobs. On the other hand, with more decoration, a label that stands out on a crowded shelf is more likely to be noticed. A concrete and effective alternative to wet glue labels is pressure-sensitive labels. Pressure-sensitive labels offer better adhesive properties and more decoration options on a reverse-printed mirror solution with metallic effects in advancements. This is why players operating in United States, focus on catering to the changing market needs.

- Pressure pressure-sensitive labels are used in the food and drink, pharmaceutical, consumer goods, personal care, and construction industries. Depending on the application, different adhesives may make pressure-sensitive labels permanent or reusable.The vendors serving these industries are working on the front line to continue producing and supplying label materials for critical consumer and healthcare products. However, the raw material prices are rising, coupled with increased competition and evolving printing and decorating technologies.

Beverage is Expected to Account For Significant Market Share

- The beverage is one of the primary end-user industries for the US print label market, owing to the high rate of adoption of innovative label and packaging in the beverage sectors and the growing market for the health drinks segment.

- Sales of significant beverage categories is expected to cross USD 170 billion by 2024. Although the consumption of some beverage segments in the country was affected during the pandemic, the scope of many segments expanded due to the COVID-19 outbreak.

- Furthermore, the country is home to some of the largest carbonated beverage companies, along with a strong market for energy drinks, which are increasingly adopting new packaging techniques to attract customers. These companies are also printing their ingredients on their labels, as health-related concerns are growing among US consumers, expanding the scope of printing. Also, these ingredients may vary between brands and specific energy drink products.

- With the growing wine market, the need for labeling is becoming crucial. Most of the wine labels use paper label look or no label look with film label. In addition, labels need to be designed to withstand the environment in which they are shipped, stored, and used. Therefore, the growing number of wineries in the country will also expand label printing and manufacturing.

- As sustainability becomes more of a presence in the labeling supply chain, there will be an increased use of recycled and recyclable materials. Top material choices will include PET, bioplastic, and thicker reusable glass. As sustainability becomes more critical in the labeling supply chain, they will likely see increased use of recyclable label materials. In addition, Avery Dennison promotes several technologies for sustainability, including its CleanFlake adhesive technology for PET bottle recycling, ClearCut Adhesive technology, and a variety of paper and film face stocks for beverage labeling applications.

- The beverage's container also dictates the subsequent adhesive choice. According to research, glass containers require a different adhesive than plastic containers. Paper and polypropylene are the two most common materials used for beverage labels, while most employ polypropylene substrates. The growing expansion of the beverage industry in the country as well as the launch of upgraded labels for beverages in the market boosted the market demand in the country.

- Further, the US vendors invest in collaboration and acquisition strategies to enrich their label solutions and increase brand awareness. For instance, US-based Fort Dearborn Company acquired Walle Corporation, a leading supplier of cut & stack, roll-fed, and shrink sleeve labels. This acquisition helped the company grow more in the printed label solutions in the US, primarily for the food, beverage, and household products segments.

United States Print Label Industry Overview

The United States print label market is moderately concentrated, owing to the presence of many large and small players in the market operating in the domestic and international market. Players are adopting key strategies, such as product innovation, strategic partnerships, expansions, and mergers and acquisitions. Some of the key developments in the market are:

- In March 2023: Taylor, a United States-based graphic communications company, announced the opening of its new label manufacturing facility in Monterrey, Mexico. The most recent opening would further aid the business in meeting the growing demand for long-lasting labels from industrial firms in Mexico.

- In October 2023: All4Labels moved to a new larger facility in Mexico City and is in the process of installing a host of new technologies as part of an impressive expansion plan to grow its presence in Mexico and the United States. The five new printing lines, focused on pressure-sensitive labels and shrink sleeves, will treble production capacity at the site, according to Almirall, while space remains for further press installations in the future

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Labels Manufactured with Digital Print Technologies

- 4.2.2 High Adoption From Healthcare and Cosmetics Segment

- 4.3 Market Challenges

- 4.3.1 Lack of Products with Ability to Withstand Harsh Climatic Conditions

- 4.4 Industry Ecosystem Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of the Impact of COVID-19 on the US Print Label Market

5 MARKET SEGMENTATION

- 5.1 By Print Process

- 5.1.1 Offset Lithography

- 5.1.2 Gravure

- 5.1.3 Flexography

- 5.1.4 Screen

- 5.1.5 Letterpress

- 5.1.6 Electrophotography

- 5.1.7 Inkjet

- 5.2 By Label Format

- 5.2.1 Wet-glue Labels

- 5.2.2 Pressure-sensitive Labels

- 5.2.3 Linerless Labels

- 5.2.4 Multi-part Tracking Labels

- 5.2.5 In-mold Labels

- 5.2.6 Shrink and Stretch Sleeves

- 5.3 By End-user Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare

- 5.3.4 Cosmetics

- 5.3.5 Household

- 5.3.6 Industrial (Automotive, Industrial Chemicals, and Consumer and Non-consumer Durables)

- 5.3.7 Logistics

- 5.3.8 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fort Dearborn

- 6.1.2 Multi Color Corporation

- 6.1.3 Mondi Group

- 6.1.4 Ahlstrom-munksjo Oyj

- 6.1.5 Cenveo Corporation

- 6.1.6 Avery Dennison Corporation

- 6.1.7 Brady Corporation

- 6.1.8 Westrock Company

- 6.1.9 R.R. Donnelley & Sons Company

- 6.1.10 Taylor Corporation