|

市場調査レポート

商品コード

1644462

米国のデジタルレンディング:市場シェア分析、産業動向、成長予測(2025年~2030年)United States Digital Lending - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のデジタルレンディング:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

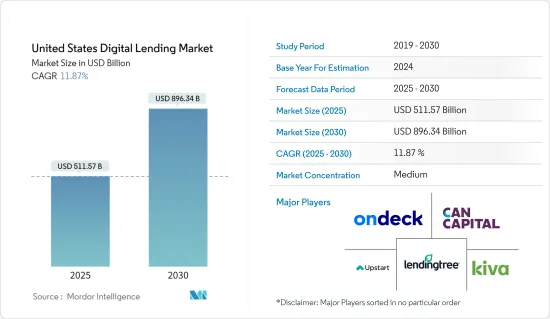

米国のデジタルレンディング市場規模は、2025年に5,115億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.87%で、2030年には8,963億4,000万米ドルに達すると予測されます。

市場の拡大は、融資最適化融資プロセスの改善、迅速な意思決定、規制や規範の遵守、企業効率の改善など、デジタル融資プラットフォームが提供する利点によって促進されると予測されます。従来の貸出プラットフォームでは、各段階で物理的な接触や人的関与が必要で、処理時間が長引き、人為的ミスの可能性が高まっていました。しかし、デジタル融資プラットフォームによって、銀行は融資プロセスを自動化し、消費者の満足度を向上させることができます。

主要ハイライト

- 米国は、様々なセグメントで早くからデジタル化を導入しているため、デジタルレンディングの世界最大かつ最先端市場のひとつです。また、好調な経済や著名なソリューション・プロバイダーの強固なプレゼンス、研究開発活動の開発と成長のための政府や民間組織による強力な投資などの要因が、この地域におけるデジタルレンディングの需要を促進する態勢を整えています。

- 資金調達はデジタルレンディングのビジネスモデルにとって極めて重要な要素です。デジタルレンディング業者が使用する主要資金調達モデルは3つあります。市場レンダー、バランスシートレンダー、銀行チャネルレンダーです。いくつかのデジタルレンダーは、成長するにつれて複数の資金調達モデルを利用しています。

- さらに、銀行には基本的な競争優位性があります。最も重要なのは、保険付き預金へのアクセスであり、これにより低コストの資本を得ることができます。規制上の懸念から、銀行は新しい技術の導入を躊躇しているようだが、銀行はますますフィンテックセグメントへの参入ポイントを探しています。多くの銀行が既存のフィンテック企業と提携し、フィンテックの技術力と自社のコスト優位性を併せ持つようになると予想されます。

- 銀行の資本コストの低さと技術的な専門知識を組み合わせることで、銀行はより効率的な顧客体験を低料金で提供できるようになり、これまで未開拓だった顧客層にも門戸を開くことができます。また米国では、クレジット組成に携わるプラットフォームは、各州のライセンシング要件に従う可能性があります。このため、多くのプラットフォームは銀行と提携し、オンラインで合意した融資を実行しています。

- COVID-19の大流行により、この地域の中小企業は、危機の間、事業を継続するための資金調達の課題に直面しました。デジタルレンディングは、特に中小企業において、成長と採用のためのいくつかの機会を見出すことが期待されます。さらに、COVID-19の大流行中、政府は国民を支援することを目的としていました。さらに、広範な雇用喪失、賃金引き下げ、深刻な流動性不足を考えると、銀行や金融機関(FI)は、COVID-19の貸出産業への影響が拡大するにつれて、与信コストと不良資産比率の増加を経験することが予想されます。貸し手は、新たな常態への適応を支援する技術の利用から大きな恩恵を受けることができます。

米国のデジタルレンディング市場動向

デジタル行動をとる潜在的ローン購入者の増加

- 米国中小企業庁によると、米国には100万米ドル以下の小企業向け融資が4,100億米ドル、小企業向け消費者ローン残高が4兆米ドルあります。また、米国ニューヨーク連銀は、銀行が小口融資に消極的なため、約1,000億米ドルの信用需要が満たされていないと計算しています。この未充足需要に対応するため、技術を駆使して銀行と連携するデジタル金融業者が注目を集めています。

- さらに、クレジットプラットフォームは、投資家がリスクを分散することを奨励しています。投資家は様々な複数のローンに分散投資することを選択でき、多くの場合、選択したリスク・カテゴリーと条件に基づいてローンのポートフォリオへのエクスポージャーを自動的に得ることができます。P2P(ピア・ツー・ピア)の消費者向けプラットフォームのうち、米国では95%以上が自動選択プロセスを採用しています。与信を促進する上で、フィンテックプラットフォームは、銀行などの伝統的クレジット・プロバイダーと同様のモニタリングやサービシング機能を提供することができます。

- ほとんどの消費者は、既存の債務の借り換えや一本化のためにフィンテック・プロバイダーを利用しているが、大きな買い物(自動車や不動産など)の資金調達に利用する人もいます。米国では、学生による高等教育資金の借り入れが目立っています。

- ビジネス面では、様々な中小・零細企業が運転資金や投資プロジェクトのために資金を求めるのが一般的です。また、投資家が企業の請求書(債権)に対する割引債権を購入する請求書取引という形で資金を調達することもあります。中小企業はほとんどの地域で経済に大きく貢献しています。以下の統計が、上記の発言を裏付けています。米国中小企業局(SBA)によると、米国人の50%以上が中小企業を経営しているか、中小企業で働いています。

消費者向けデジタルレンディングは大幅な成長が見込まれる

- 特に、消費者ローンに特化したGreenSky Inc.のIPOにより、銀行チャネルベースの融資が注目を集めました。同社は110億米ドル以上の銀行からのコミットメントを獲得しています。中小企業向け融資のOnDeckは、その技術を銀行にライセンス供与するOnDeck-as-a-Serviceプラットフォームの拡大を発表しました。同社はPNC銀行を顧客として追加し、将来の銀行チャネルベースのビジネスに対応するため、新たな子会社ODXを立ち上げました。アバントは、個人向け融資のための銀行提携プラットフォーム「Amount」を立ち上げました。

- 成長を続けるために、デジタル金融業者は、資金調達と商品提供の両面で、活動範囲を拡大する機会を活用しています。例えば、学生ローンの借り換え会社として始まったSoFiは、現在では個人ローンと住宅ローンを提供しています。個人ローンに特化したレンディングクラブもビジネスローン商品を提供しています。SquareやPaypalのように、隣接するフィンテックセグメントからデジタル融資に参入した企業がある一方で、融資以外のサービスを提供することで、による方向に進もうとしている金融業者もあります。SoFiはこの面で最も積極的で、資産管理サービスを提供し、高利回りの預金口座商品SoFi Moneyの申込者を受け入れています。

- 学生ローン新興企業は、この地域が学生ローン債務危機に直面し続けているため、新たな投資と新規顧客を目の当たりにしています。米連邦準備制度理事会(FRB)は、米国の学生ローン債務を1兆7,000億米ドルと見積もっています。学生は平均して、民間と連邦政府のローン債務2万9,000米ドルを抱えて卒業し、15%の割合でローンを滞納しています。

- このセグメントで提供される商品には、学生ローンの借り換え、ダイレクト学生ローン、個人ローン、さらには資産管理や住宅ローン商品などがあります。

- オンライン上でのサービス提供、文書管理、情報保管、データ処理など、金融機関を支援するその能力から、クラウドはデジタル融資における最も重要な動向のひとつと見なすことができます。Accentureによると、現在90%以上の銀行が、少なくともかなりのレベルのワークロードをクラウドで運用しているといいます。

米国のデジタルレンディング産業概要

米国のデジタルレンディング市場は半固定化されると予想され、様々な世界企業が市場に参入するための投資やM&A活動が増加しています。ベンダーは、多くの利点を提供することで消費者基盤を獲得するために支出を増やしています。さらに、こうした投資は競争戦略の強力な一翼を担っています。流通チャネルへのアクセス、すでに存在する取引関係、より優れたサプライチェーンの知識、自社所有のプラットフォームは、市場に参入する既存のハイテク大手企業に、新規参入の競合他社に対する優位性を与えています。

2023年10月、米国のソフトウェア会社であるBlend Labsと、金融機関や消費者研究機関向けのソフトウェアプロバイダーであるMeridianLink Inc.は提携を発表しました。ブレンドは、MeridianLinkの消費者向けローン組成ソフトウェア(LOS)を利用している金融機関は、ブレンドの統一プラットフォームと消費者向けバンキング組成ソフトウェアを利用することで、バンキング、クレジットカード、ローン商品の迅速なオンボーディングと申し込み手続きが可能になると述べています。

2023年9月、デジタルレンディングプラットフォームのRevvin(旧MortgageHippo)を、Wells Fargoがスポンサーを務める住宅ローン・フィンテックのMaxwellが買収し、POS技術を向上させると発表しました。同社は、Revvinのローン組成プロセスの高速化に注目しており、金利上昇、ローン量の制限、貸出費用の増加といった課題が続く住宅ローン市場において、Maxwellは貸出業者に利益をもたらすと考えています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 規制状況

- 米国における個人ローン借り手の主要指標

- 米国における借り手のローン負債比率

- スーパープライム

- プライム・プラス

- プライム

- ニアプライム

- サブプライム

- 米国における借り手の平均残高

- スーパープライム

- プライム・プラス

- プライム

- ニアプライム

- サブプライム

- 米国における借り手の延滞率

- スーパープライム

- プライム・プラス

- プライム

- ニアプライム

- サブプライム

- 米国における借り手のローン負債比率

- デジタルレンダーのオリジネーション・ボリュームの分析

- 個人ローン

- 中小企業向けローン

- 米国におけるサブプライム層の分析

- 州別分布

- 年齢層別人口統計

- サブプライム層の全体的な縮小

第5章 市場力学

- 市場促進要因

- デジタル行動」を持つ潜在的ローン購入者の増加

- 可処分所得の増加

- 市場抑制要因

- デジタルレンディングに伴うセキュリティ上の懸念

第6章 市場セグメンテーション

- タイプ別

- ビジネス

- ビジネスデジタルレンディング市場力学

- ビジネスデジタルレンディングのエコシステム(新興企業と既存企業の両方を含む)

- 市場推定・予測

- 消費者

- 消費者向けデジタルレンディング市場力学

- 消費者向けデジタルレンディングモデル(給料日貸し、ピアツーピアローン、個人ローン、自動車ローン、学生ローン)

- 消費者向けデジタルレンディングのエコシステム(新興企業と既存企業の両方を含む)

- 市場推定・予測

- ビジネス

第7章 競合情勢

- 企業プロファイル

- Bizfi, LLC.

- OnDeck Capital Inc.

- Prosper Marketplace Inc.

- LendingClub Corp.

- Social Finance Inc.(SoFi)

- Upstart Network Inc.

- Kiva Microfunds

- Kabbage Inc.

- Lendingtree Inc.

- CAN Capital Inc.

第8章 投資分析

第9章 市場機会と将来展望

The United States Digital Lending Market size is estimated at USD 511.57 billion in 2025, and is expected to reach USD 896.34 billion by 2030, at a CAGR of 11.87% during the forecast period (2025-2030).

Market expansion is anticipated to be fueled by the advantages provided by digital lending platforms, such as improved loan optimization loan process, quicker decision-making, compliance with regulations and norms, and improved corporate efficiency. Traditional lending platforms required physical contact and human engagement at every stage, which prolonged processing times and raised the possibility of human error. However, digital lending platforms allow banks to automate the loan process, improving consumer satisfaction.

Key Highlights

- The United States is one of the largest and most advanced markets for digital lending globally due to its early adoption of digitization in various sectors. Also, factors such as the strong economy and robust presence of prominent solution providers, coupled with strong investment by government and private organizations for the development and growth of research & development activities, are poised to drive the demand for digital lending in the region.

- Funding is a crucial element of the digital lending business model. There are three major funding models used by digital lenders: Marketplace lenders, Balance sheet lenders, and bank channel lenders. Several digital lenders have been tapping multiple funding models as they grow.

- Further, banking institutions retain certain fundamental competitive advantages. Arguably the most important is their access to insured deposits, which affords them low-cost capital. Regulatory concerns have likely caused banks to hesitate when adopting new technologies, but banks are increasingly looking for points of entry to the fintech space. It is expected that many banks will partner with existing fintech companies to have their cost advantages with the fintech's technological capabilities.

- By combining their technological expertise with banks' lower cost of capital, these partnerships could enable banks to provide more efficient customer experiences at lower rates and open them up to previously untapped customer segments. Also, in the United States, platforms engaging in credit origination can be subjected to licensing requirements in each state. For this reason, many platforms partner with the banks to originate loans agreed online.

- Owing to the COVID-19 pandemic, SMEs in the region faced challenges in raising funds during the crisis to keep their businesses operating. Digital Lending is expected to find several opportunities, especially among SMEs, for growth and adoption. Further, during the COVID-19 pandemic, the government aimed to support the people. Moreover, given widespread job losses, wage reductions, and a severe liquidity shortage, banks and financial institutions (FIs) anticipates to experience an increase in credit costs and non-performing assets ratio as the effects of COVID-19 on the lending industry develop. Lenders can benefit significantly from the use of technology to assist them in adjusting to the new normal.

United States Digital Lending Market Trends

Increasing Number of Potential Loan Purchasers with Digital Behavior

- According to the U.S. Small Business Administration, there are USD 410 billion in sub-USD 1 million loans to small firms and USD 4 trillion in outstanding consumer loans for small enterprises in the US. In addition, the US Federal Reserve Bank of NY calculates an approximate USD 100 billion unmet credit demand due to banks' resistance to making small-dollar loans. To address the unmet demand, technology-driven digital lenders are attracting attention in their capacity to collaborate with banks.

- Moreover, credit platforms majorly encourage investors to spread the risks. Investors can choose to spread the investments across various multiple loans and often can automatically gain exposure to a portfolio of loans based on the risk category and terms they select. Among P2P (peer-to-peer) consumer platforms, more than 95% of the United States use an auto-selection process. In facilitating credit, fintech platforms can provide monitoring and servicing functions that are similar to those of traditional credit providers such as banks.

- Most consumers use fintech providers to refinish or consolidate existing debts, but some use them to finance their major purchases (such as vehicles or real estate). Borrowing by students to fund higher education is prominent in the United States.

- On the business side, various small and micro enterprises typically seek funds for working capital or investment projects. Financing can also be in the form of invoice trading, whereby investors purchase discounted claims on a firm's invoices (receivables). SMEs are contributing to the economy significantly for most regions. The following statistics validate the above statement: According to the US Small Business Administration (SBA), more than 50% of Americans either own or work for a small business.

Consumer Digital Lending is Expected to Grow Significantly

- Bank channel-based lending drew particular attention, especially with the IPO of consumer loan-focused GreenSky Inc. The company has secured more than USD 11 billion in bank commitments. Small business-focused lender OnDeck announced an expansion of its OnDeck-as-a-Service platform through which it licenses its technology to banks. The company added PNC Bank as a customer and launched a new subsidiary, ODX, to handle future bank channel-based business. Avant launched a bank partnership platform for personal lending called Amount.

- In order to keep growing, digital lenders are taking advantage of opportunities to expand the scope of their activities, both in terms of funding and product offerings. For example, SoFi, which began as a student loan refinancing company, now offers personal loans and mortgages. Personal loan-focused LendingClub also offers a business loan product. While some the companies, such as Square and PayPal, entered digital lending from adjacent fintech segments, some lenders are moving in the other direction by offering nonlending services. SoFi has been the most aggressive on this front, offering wealth management services and accepting applicants for its high-yield deposit account product, SoFi Money.

- Student-focused lenders remain the most diversified platforms in the digital lending sector as Student loan startups are witnessing new investments and new customers as the region faces a continued student loan debt crisis. The Federal Reserve estimates USD 1.7 trillion in U.S. student loan debt. Students, on average, graduate with USD 29,000 of private and federal loan debt and default on their loans at a rate of 15%.

- Product offerings in this segment include student loan refinance, direct student loans, personal loans, and even wealth management and mortgage products.

- Due to its capacity to assist financial institutions with service delivery, document management, information storage, and data processing online, the cloud can be regarded as one of the most important trends in digital lending. It's understandable why, according to Accenture, more than 90% of banks currently have at least a significant level of workloads operating in the cloud.

United States Digital Lending Industry Overview

The United States digital lending market is expected to be semi-consolidated, observing an increase in the number of investments and M&A activities by various global enterprises to gain access to the market. Vendors are increasingly spending on gaining a consumer base by offering numerous benefits. In addition, such investments are a strong part of their competitive strategy. Access to the distribution channel, already present business relations, better supply chain knowledge, and the self-owned platform give the established tech giants entering the market an advantage over the new competitors.

In October 2023, Blend Labs, a United States-based software company, and MeridianLink Inc., a software provider for financial institutions and consumer reporting agencies, announced a partnership. Blend stated that lenders utilizing MeridianLink Consumer loan origination software (LOS) can use Blend's unified platform and consumer banking origination software for a quick onboarding and application procedure for banking, credit card, and loan products.

In September 2023, the digital lending platform Revvin, formerly MortgageHippo, was announced to be acquired by Maxwell, a mortgage fintech sponsored by Wells Fargo, to improve its point-of-sale technology. The company focuses on Revvin's faster loan origination process, which Maxwell thinks would benefit lenders as the mortgage market continues to be challenged by rising interest rates, limited loan volume, and increasing lending expenses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Regulatory Landscape

- 4.3 Key Indicators for Personal Loan Borrowers in the United States

- 4.3.1 Percentage of Loan Debt in United States Held By Borrowers

- 4.3.1.1 Super Prime

- 4.3.1.2 Prime Plus

- 4.3.1.3 Prime

- 4.3.1.4 Near Prime

- 4.3.1.5 Sub Prime

- 4.3.2 Average Outstanding Balances in United States Held By Borrowers

- 4.3.2.1 Super Prime

- 4.3.2.2 Prime Plus

- 4.3.2.3 Prime

- 4.3.2.4 Near Prime

- 4.3.2.5 Sub Prime

- 4.3.3 Delinquency Rates of Borrowers in United States

- 4.3.3.1 Super Prime

- 4.3.3.2 Prime Plus

- 4.3.3.3 Prime

- 4.3.3.4 Near Prime

- 4.3.3.5 Sub Prime

- 4.3.1 Percentage of Loan Debt in United States Held By Borrowers

- 4.4 Analysis of Origination Volumes of Digital Lenders

- 4.4.1 Personal Loans

- 4.4.2 SME Loans

- 4.5 Analysis of Subprime Borrowers in the United States

- 4.5.1 Distribution by States

- 4.5.2 Demographic Breakdown by Age

- 4.5.3 Overall Shrinking of Subprime Population in the Country

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Uptick of Potential Loan Purchasers with 'Digital Behavior'

- 5.1.2 Increasing Disposable Income

- 5.2 Market Restraints

- 5.2.1 Security Concerns involved in Digital Lending

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Business

- 6.1.1.1 Business Digital Lending Market Dynamics

- 6.1.1.2 Business Digital Lending Ecosystem (including both Startups and Incumbents)

- 6.1.1.3 Market Size Estimates and Forecasts

- 6.1.2 Consumer

- 6.1.2.1 Consumer Digital Lending Market Dynamics

- 6.1.2.2 Consumer Digital Lending Models (Payday Lenders, Peer-to-peer Loans, Personal Loans, Auto Loans, and Student Loans)

- 6.1.2.3 Consumer Digital Lending Ecosystem (including both Startups and Incumbents)

- 6.1.2.4 Market Size Estimates and Forecasts

- 6.1.1 Business

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Bizfi, LLC.

- 7.1.2 OnDeck Capital Inc.

- 7.1.3 Prosper Marketplace Inc.

- 7.1.4 LendingClub Corp.

- 7.1.5 Social Finance Inc. (SoFi)

- 7.1.6 Upstart Network Inc.

- 7.1.7 Kiva Microfunds

- 7.1.8 Kabbage Inc.

- 7.1.9 Lendingtree Inc.

- 7.1.10 CAN Capital Inc.