|

|

市場調査レポート

商品コード

1644435

PETボトル:市場シェア分析、産業動向・統計、成長予測(2025~2030年)PET Bottles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| PETボトル:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

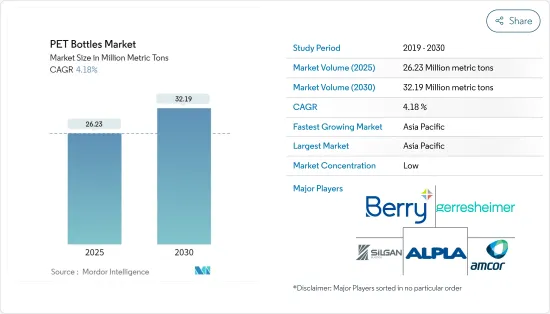

PETボトルの市場規模は2025年に2,623万トンと推定され、予測期間(2025-2030年)のCAGRは4.18%で、2030年には3,219万トンに達すると予測されます。

主なハイライト

- 主にポリエチレンテレフタレート製のプラスチックボトルと容器は、軽量で耐久性があり、取り扱いが容易なため広く使用されています。製造コストが低いため、メーカーはプラスチック包装を好みます。予測期間中、プラスチック包装の費用対効果と包装食品・飲食品の需要増に後押しされ、同市場は成長する見込みです。さらに、ポリエチレンテレフタレート(PET)容器は、耐久性、汎用性、費用対効果で支持されています。飲食品、薬局などのエンドユーザー産業が拡大し、技術革新が進むにつれて、プラスチックボトルと容器包装の需要は伸びています。業界では、様々なフレーバーや包装形態を持つ新しい飲料のイントロダクションが、硬質プラスチックボトルのニーズを引き続き牽引しています。

- PETボトルは軽量で耐久性に優れているため、ガラスボトルに取って代わりつつあります。これらのボトルは、ミネラルウォーターやその他の飲料の包装に使用することができ、より費用対効果の高い輸送を可能にしています。PETの透明性と固有のCO2バリア特性は、様々な用途に適しています。PETは容易に様々な形状に成形したり、吹き込んでボトルにすることができます。製造業者は、着色剤、UVカット剤、酸素バリア剤などの添加剤を組み込むことによってPETの特性をカスタマイズすることができ、特定のブランドのニーズに合わせたボトルを作ることができます。

- PETボトル包装市場は、主に環境問題への関心の高まりに後押しされた規制基準の進化により、大きな課題に直面しています。世界各国の政府は、環境への影響を最小限に抑え、廃棄物管理プロセスを改善するための規制を実施することで、プラスチック包装廃棄物に対する国民の不安に対応しています。このような規制の変更には、使い捨てプラスチックの制限、リサイクル目標の引き上げ、生産者責任プログラムの拡大などがよく含まれます。その結果、PETパッケージングメーカーは、これらの新しい基準に準拠するために、生産プロセスを適応させ、環境に優しい代替品に投資し、より持続可能なパッケージングソリューションを開発しています。このような規制状況は業界の運営コストに影響を与え、環境意識の高い消費者が持続可能な包装オプションを求めるようになっているため、消費者の嗜好にも影響を及ぼしています。

- 持続可能なパッケージング・ソリューションは、環境に優しいパッケージングの環境上の利点に関する消費者の意識の高まりにより、注目されるようになった。PETは、そのリサイクル性と循環の可能性から、環境に優しい包装材料の中でも不可欠な樹脂となっています。プラスチックがリサイクルされ、同じカテゴリの新製品を作るために使用されるクローズドループリサイクルは、PETボトルによく適用されています。このアプローチにより、企業は他の樹脂素材よりもPETを優先するようになった。その結果、ペットボトルのリサイクルは市場にプラスの影響を与えると予想されます。

- 各企業は、エンドユーザー・セグメントにおけるrPETの需要増に対応するために技術革新を進めています。持続可能なパッケージングの急増は、消費者の嗜好とプラスチック廃棄物を抑制するための規制義務によって後押しされています。例えば、2024年6月、クラフト・ハインツは12オンスと22オンスのKraft Real MayoとMiracle Whipサイズに100%リサイクルPETボトルを導入しました。この動きは、同社が2023年に発表した、2030年までに全世界のパッケージング・ポートフォリオにおけるバージン・プラスチックの使用量を20%削減するという目標に続くものです。食品包装にrPETを採用することは、この素材が汎用性があり、業界で受け入れられつつあることを示しています。他の企業も追随する可能性が高く、rPET需要の大幅な増加と、この需要に対応するためのリサイクル技術のさらなる革新につながる可能性があります。

PETボトル市場の動向

飲料分野が大きな成長を遂げる見込み

- PETボトルは、その耐久性とリサイクル性により、ガラスや他のプラスチックボトルよりも水の包装業界を支配しています。この動向は、軽量で耐久性があり、費用対効果の高いPETが、水の包装媒体としてますます好まれるようになってきていることを示しています。このシフトは、利便性と持続可能性に対する消費者の要求と、効率的で費用対効果の高いパッケージング・ソリューションに対するメーカーのニーズによってもたらされています。PETボトルは成形可能であるため、変化する包装動向やラベリングニーズに素早く対応でき、デザインやブランディングのための多様なキャンバスを提供することができます。軽量で耐久性に優れているため、ペットボトル飲料に適しており、費用対効果の高い輸送と二酸化炭素排出量の削減に貢献しています。

- ポリエチレンテレフタレート(PET)ボトルは、多様な製品分野でますます普及しています。その魅力は、手頃な価格、軽量性、印刷技術の絶え間ない進歩にあります。これらの要因により、特に目の肥えた消費者の間で、PETボトルの地位は著しく向上しています。Indorama Venturesは、ポリエチレンテレフタレート樹脂の需要が2023年の3,000万トンから2030年には4,200万トンに急増すると予測しています。

- PETボトル市場の飲料分野は、ボトル入り飲料水とノンアルコール飲料の需要増加により成長する見込みです。この需要は、消費者が高品質の飲料水を好むこと、汚染された水道水に対する懸念、携帯用ボトル入り飲料水の利便性などが背景にあります。包装飲料水に対する世界の需要は、プラスチックボトル包装業界の飲料カテゴリーをさらに推進する可能性があります。ペットボトルは、他の包装オプションと比べ、費用対効果が高く、保存期間が長く、使いやすいことから支持されています。

- 世界各国の政府は、使い捨てプラスチックボトルのリサイクルを促進する取り組みを強化しています。その戦略には、消費者に再利用可能なペットボトルに詰め替えるよう奨励すること、製造に生分解性または再生PETを利用すること、環境に優しい製品を設計すること、ペットボトルリサイクルのための専門協議会を設立することなどが含まれます。メーカー各社は、技術革新によってこの動向に対応しています。政府の規制や企業の持続可能性目標を達成しようと努力し、持続可能な生産におけるリーダーとしての地位を確立しています。

アジア太平洋が市場で大きなシェアを占める見込み

- アジア太平洋地域の飲料包装業界は、近年著しい成長を遂げています。この成長を促進する主な要因には、地域全体の包装動向の急速な変化が含まれます。飲料包装の新たな動向は、構造の変化、ポストコンシューマーリサイクルなどのリサイクル素材の開発、顧客の受容性、安全性、より新しい充填技術、耐熱性PETボトルの開発などに焦点を当てています。これらの進歩は、様々な飲料の保存性を向上させながら、市場に新たな可能性と選択肢を提供しています。

- 人口増加とライフスタイルの変化により、中国とインドではボトル入り飲料水の消費が増加しています。この動向は、持続可能性に関する規制を満たしながら、軽量で持ち運びができ、保存が容易な様々なボトル形式への需要を生み出しています。人口が多く新興経済諸国であるインドでは、ボトル入り飲料水の消費量が大幅に増加しています。Indian Railway Catering and Tourism Corporation Limitedは、PETボトル入り飲料水ブランド「Rail Neer」を導入し、主に列車内や駅で販売しています。同公社は、ボトル入り飲料水の消費量の増加と鉄道産業の拡大に伴い、生産量を増やしています。2021年には7,530万本が生産され、2023年には3億5,770万本に増加します。

- この地域の国々は、再生プラスチックの使用を促進するため、持続可能で環境に優しい慣行に重点を移しています。このシフトにより、コカ・コーラのような飲料メーカーは、環境への影響を減らすための戦略に再生プラスチックを取り入れるようになった。2024年4月、米国の飲料会社コカ・コーラ社は、再生ポリエチレンテレフタレート(rPET)製のコカ・コーラオリジナル、コカ・コーラ無糖、コカ・コーラプラスのボトルを香港で発売しました。北京では、INCOMが2023年6月に天津でrPET工場の第2段階を開始すると発表しました。このプロジェクトは、年間5万トンの廃ペットボトル処理能力を持つ食品グレードのパッケージング生産ラインの確立を目指しています。

- さらに2023年6月、コカ・コーラ・インディアはオーストリアのパッケージング・ソリューション・プロバイダーであるALPLA社と提携し、インドにおけるキンレイ・ブランドの画期的な取り組みを発表しました。ボトル入りの飲料水ブランドとして知られるキンレイは、100%リサイクルされたrPETボトルのみを使用するようになり、インドの飲料業界における先駆的な動きとなった。注目すべきは、1リットル入りのこのボトルが、このような持続可能な素材から作られた飲食品分野ではインド初の製品であることです。この戦略的コラボレーションは、循環型経済の育成に対するアルプラとコカ・コーラのコミットメントを強調するものです。

- インドネシア、カンボジア、シンガポール、タイ、ベトナムを含む東南アジア諸国では、様々な業界でPETボトルの需要が増加しています。この成長は特に飲食品業界で顕著であり、PETボトルは飲料や液体食品の包装に広く使用されています。製薬業界では、PETボトルはその耐久性と化学的相互作用に対する耐性から好まれています。化粧品やパーソナルケア産業もこの需要に貢献しており、シャンプー、ローション、その他のパーソナルケア製品にPETボトルが利用されています。このように複数の分野で広く採用されていることが、アジア太平洋地域の市場成長を牽引する重要な要因となっています。

PETボトル産業の概要

PETボトル市場は断片化されており、Amcor Group GmbH、Gerresheimer AG、Alpla Group、Berry Global Inc.など、複数の世界的・地域的プレーヤーが、競争の激しい市場空間で注目度を競っています。この市場の特徴は、製品の差別化が低いこと、製品の普及が進んでいること、競合が多いことです。

- 2024年5月-アルプラは、従来のガラス瓶に比べいくつかの利点を持つリサイクル可能なPETワインボトルを発表しました。この革新的なパッケージング・ソリューションは、ガラス瓶の約8分の1の重さで、二酸化炭素排出量を最大50%削減し、コストを最大30%削減できます。このボトルは全て再生PET(rPET)で製造されています。

- 2024年4月-責任あるパッケージング・ソリューションの開発・製造企業であるアムコーは、消費者再生利用(PCR)原料のみを使用した炭酸飲料(CSD)用1Lポリエチレンテレフタレート(PET)ボトルの発売を発表しました。Amcor Rigid Packaging(ARP)は、この1L CSD 100%PCRボトルを、再生材料を使用した責任あるパッケージング・ポートフォリオに加える予定です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン分析

- 地政学的動向の業界への影響評価

第5章 市場力学

- 市場促進要因

- 軽量包装方法の採用増加

- ボトル入り飲料水業界におけるPET包装の需要増加

- 市場の課題

- プラスチック使用に関する環境問題

第6章 技術スナップショット

- ストレッチブロー成形

- 射出成形

- 押出ブロー成形

- 熱成形

第7章 市場セグメンテーション

- 業界別

- 飲料

- パッケージ飲料水

- 炭酸飲料

- フルーツジュース

- エナジードリンク

- その他の飲料

- 食品

- パーソナルケア

- 家庭用品

- 医薬品

- その他のエンドユーザー業界別

- 飲料

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- アジア

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- ラテンアメリカ

- メキシコ

- ブラジル

- コロンビア

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- 北米

第8章 競合情勢

- 企業プロファイル

- Gerresheimer AG

- Pact Group Holdings Limited

- Alpla Group

- Berry Global Inc.

- Alpha Packaging Pvt. Ltd

- Greiner Packaging International GmbH

- Retal Industries Limited

- Zhejiang Xinlei Packaging Co. Ltd

- Shenzhen Zhenghao Plastic & Mold Co. Ltd

- Manjushree Technopack Limited

- Resilux NV

- Greiner Packaging International GmbH

- Comar Packaging LLC

- Retal Industries Limited

- SILGAN PLASTICS LLC(Silgan Holdings Inc.)

- Nampak Ltd.

- Amcor Group GmbH

- Graham Packaging

- Container Corporation of Canada

- Altium Packaging

- Apex Plastics

第9章 投資分析

第10章 市場機会と今後の動向

The PET Bottles Market size is estimated at 26.23 million metric tons in 2025, and is expected to reach 32.19 million metric tons by 2030, at a CAGR of 4.18% during the forecast period (2025-2030).

Key Highlights

- Plastic bottles and containers, primarily made of polyethylene terephthalate, are widely used because they are lightweight and durable, facilitating easier handling. Manufacturers prefer plastic packaging because of its lower production costs. During the forecast period, the market studied is poised for growth, propelled by the cost-effectiveness of plastic packaging and the rising demand for packaged food and beverages. Furthermore, polyethylene terephthalate (PET) containers are favored for their durability, versatility, and cost-effectiveness. As end-user industries such as food, beverage, and pharmacy expand and innovate, the demand for plastic bottles and container packaging grows. The introduction of new drinks with various flavors and packaging formats in the industry continues to drive the need for rigid plastic bottles.

- PET bottles are increasingly replacing glass bottles due to their lightweight and durable nature. These bottles can be used to pack mineral water and other beverages, enabling more cost-effective transportation. PET's transparency and inherent CO2 barrier properties suit it for various applications. PET can readily be molded into different shapes or blown into bottles. Manufacturers can customize PET's properties by incorporating additives like colorants, UV blockers, and oxygen barriers, enabling the creation of bottles tailored to specific brand needs.

- The PET packaging market faces significant challenges due to evolving regulatory standards, primarily driven by growing environmental concerns. Governments worldwide are responding to public apprehension about plastic packaging waste by implementing regulations to minimize environmental impact and improve waste management processes. These regulatory changes often include restrictions on single-use plastics, increased recycling targets, and extended producer responsibility programs. As a result, PET packaging manufacturers adapt their production processes, invest in eco-friendly alternatives, and develop more sustainable packaging solutions to comply with these new standards. This regulatory landscape affects the industry's operational costs and influences consumer preferences as environmentally conscious consumers increasingly demand sustainable packaging options.

- Sustainable packaging solutions have gained prominence due to increased consumer awareness regarding the environmental benefits of eco-friendly packaging. PET has become an essential resin among eco-friendly packaging materials due to its recyclability and potential for circularity. Closed-loop recycling, where plastic is recycled and used to create new products in the same category, is often applied to PET bottles. This approach has led businesses to prioritize PET over other resin materials. As a result, the recycling of plastic bottles is expected to impact the market positively.

- Companies are innovating to meet the increasing demand for rPET across end-user segments. The surge in sustainable packaging is propelled by consumer preferences and regulatory mandates to curb plastic waste. For instance, in June 2024, Kraft Heinz introduced 100% recycled PET bottles for its 12- and 22-oz Kraft Real Mayo and Miracle Whip sizes. This move followed the company's 2023 announcement of a goal to reduce virgin plastic use in its global packaging portfolio by 20% by 2030. Adopting rPET in food packaging demonstrates the material's versatility and growing acceptance in the industry. Other companies are likely to follow suit, potentially leading to a significant increase in rPET demand and further innovations in recycling technologies to meet this demand.

PET Bottles Market Trends

The Beverages Segment is Expected to Witness Significant Growth

- PET bottles dominate the water packaging industry over glass and other plastic bottles due to their durability and recyclability. The trend indicates that lightweight, durable, and cost-effective PET is increasingly becoming the preferred packaging medium for water. This shift is driven by consumer demand for convenience and sustainability and manufacturers' need for efficient and cost-effective packaging solutions. Due to their moldability, PET bottles can quickly adapt to changing packaging trends and labeling needs, providing a versatile canvas for design and branding. Their lightweight and durable properties make them a preferred choice for bottled beverages and contribute to cost-effective transportation and lower carbon emissions.

- Polyethylene terephthalate (PET) bottles are increasingly prevalent across diverse product segments. Their appeal lies in their affordability, lightweight nature, and the continuous advancements in printing technologies. These factors have notably elevated PET bottles' status, particularly among discerning consumers. Indorama Ventures projects a surge in demand for polyethylene terephthalate resins, from 30 million metric tons in 2023 to 42 million by 2030.

- The beverages segment in the PET bottles market is poised for growth due to increasing demand for bottled water and non-alcoholic beverages. This demand is driven by consumers' preference for high-quality drinking water, concerns about contaminated tap water, and the convenience of portable bottled water. The global demand for packaged drinking water may further propel the beverage category in the plastic bottle packaging industry. Plastic bottles are favored for their cost-effectiveness, extended shelf life, and ease of use compared to other packaging options.

- Governments worldwide are intensifying their efforts to promote recycling single-use plastic bottles. Strategies include encouraging consumers to refill reusable plastic bottles, utilizing biodegradable or recycled PET for manufacturing, designing eco-friendly products, and establishing dedicated councils for bottle recycling. Manufacturers are responding to this trend by innovating. They strive to meet government regulations and corporate sustainability goals and are positioning themselves as leaders in sustainable production.

Asia-Pacific Expected to Hold Significant Share in the Market

- The beverage packaging industry in the region has experienced significant growth in recent years. Key factors driving this growth include rapid changes in packaging trends across the region. New trends in beverage packaging focus on structural changes, the development of recycled materials such as post-consumer recycling, customer acceptance, safety, newer filling technologies, and the development of heat-resistant PET bottles. These advancements have provided new possibilities and options in the market while improving the preservation of various drinks.

- The consumption of bottled water is increasing across China and India due to population growth and changing lifestyles. This trend is creating demand for various bottle formats that are lightweight, portable, and easily stored while meeting sustainability regulations. With its large population and developing economy, India is experiencing a significant increase in bottled water consumption. The Indian Railway Catering and Tourism Corporation Limited introduced a PET bottled water brand, "Rail Neer," primarily sold on trains and at railway stations. The corporation is increasing production with the increase in bottled water consumption and expansion of the railway industry. In 2021, 75.30 million bottles were produced, which rose to 357.70 million in 2023.

- Countries in the region are shifting their focus toward sustainable and eco-friendly practices to promote the use of recycled plastic. This shift has prompted beverage manufacturers like Coca-Cola to incorporate recycled plastic into their strategies for reducing environmental impact. In April 2024, The Coca-Cola Company, a US-based beverage company, introduced Coca-Cola Original, Coca-Cola No Sugar, and Coca-Cola Plus bottles made from recycled polyethylene terephthalate (rPET) in Hong Kong. In Beijing, INCOM announced the commencement of phase II of its rPET plant in Tianjin in June 2023. The project aims to establish a food-grade packaging production line with an annual waste plastic bottle processing capacity of 50,000 tons.

- Furthermore, in June 2023, Coca-Cola India, in partnership with Austrian packaging solution provider ALPLA, introduced a groundbreaking initiative for its Kinley brand in India. Kinley, a prominent bottled drinking water brand, now exclusively utilizes 100% recycled rPET bottles, marking a pioneering move in India's beverage landscape. Notably, these bottles, available in one-liter variants, are the nation's inaugural offering in the food and beverage realm crafted from such sustainable materials. This strategic collaboration underscores ALPLA's and Coca-Cola's commitment to fostering a circular economy.

- Southeast Asian countries, including Indonesia, Cambodia, Singapore, Thailand, and Vietnam, experienced increased demand for PET bottles in various industries. This growth is particularly notable in the food and beverage industry, where PET bottles are widely used for packaging beverages and liquid food products. In the pharmaceutical industry, PET bottles are preferred for their durability and resistance to chemical interactions. The cosmetics and personal care industries also contribute to this demand, utilizing PET bottles for products such as shampoos, lotions, and other personal care items. This widespread adoption across multiple sectors has been a significant factor in driving market growth in Asia-Pacific.

PET Bottles Industry Overview

The PET bottles market is fragmented, with several global and regional players, such as Amcor Group GmbH, Gerresheimer AG, Alpla Group, and Berry Global Inc., vying for attention in a contested market space. This market is characterized by low product differentiation, growing levels of product penetration, and high levels of competition.

- May 2024 - ALPLA introduced a recyclable PET wine bottle that offers several advantages over traditional glass bottles. This innovative packaging solution weighs approximately one-eighth of a glass bottle, reduces carbon footprint by up to 50%, and can lower costs by up to 30%. The bottle is manufactured entirely from recycled PET (rPET).

- April 2024 - Amcor, a player in developing and producing responsible packaging solutions, announced the launch of a 1 L polyethylene terephthalate (PET) bottle for carbonated soft drinks (CSDs) made entirely from post-consumer recycled (PCR) content. Amcor Rigid Packaging (ARP) is expected to incorporate this 1 L CSD 100% PCR bottle into its growing portfolio of responsible packaging made from recycled materials.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of Geopolitical Developments on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Lightweight Packaging Methods

- 5.1.2 Increasing Demand for PET Packaging from the Bottled Water Industry

- 5.2 Market Challenges

- 5.2.1 Environmental Concerns Regarding Use of Plastics

6 TECHNOLOGY SNAPSHOT

- 6.1 Stretch Blow Molding

- 6.2 Injection Molding

- 6.3 Extrusion Blow Molding

- 6.4 Thermoforming

7 MARKET SEGMENTATION

- 7.1 By End-user Vertical

- 7.1.1 Beverages

- 7.1.1.1 Packaged Water

- 7.1.1.2 Carbonated Soft Drinks

- 7.1.1.3 Fruit Juice

- 7.1.1.4 Energy Drinks

- 7.1.1.5 Other Beverages

- 7.1.2 Food

- 7.1.3 Personal Care

- 7.1.4 Household Care

- 7.1.5 Pharmaceuticals

- 7.1.6 Other End-user Verticals

- 7.1.1 Beverages

- 7.2 By Geography

- 7.2.1 North America

- 7.2.1.1 United States

- 7.2.1.2 Canada

- 7.2.2 Europe

- 7.2.2.1 United Kingdom

- 7.2.2.2 Germany

- 7.2.2.3 France

- 7.2.2.4 Italy

- 7.2.3 Asia

- 7.2.3.1 China

- 7.2.3.2 India

- 7.2.3.3 Japan

- 7.2.3.4 Australia and New Zealand

- 7.2.4 Latin America

- 7.2.4.1 Mexico

- 7.2.4.2 Brazil

- 7.2.4.3 Columbia

- 7.2.5 Middle East and Africa

- 7.2.5.1 Saudi Arabia

- 7.2.5.2 South Africa

- 7.2.5.3 United Arab Emirates

- 7.2.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Gerresheimer AG

- 8.1.2 Pact Group Holdings Limited

- 8.1.3 Alpla Group

- 8.1.4 Berry Global Inc.

- 8.1.5 Alpha Packaging Pvt. Ltd

- 8.1.6 Greiner Packaging International GmbH

- 8.1.7 Retal Industries Limited

- 8.1.8 Zhejiang Xinlei Packaging Co. Ltd

- 8.1.9 Shenzhen Zhenghao Plastic & Mold Co. Ltd

- 8.1.10 Manjushree Technopack Limited

- 8.1.11 Resilux NV

- 8.1.12 Greiner Packaging International GmbH

- 8.1.13 Comar Packaging LLC

- 8.1.14 Retal Industries Limited

- 8.1.15 SILGAN PLASTICS LLC (Silgan Holdings Inc.)

- 8.1.16 Nampak Ltd.

- 8.1.17 Amcor Group GmbH

- 8.1.18 Graham Packaging

- 8.1.19 Container Corporation of Canada

- 8.1.20 Altium Packaging

- 8.1.21 Apex Plastics