|

市場調査レポート

商品コード

1690743

カートンボード-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| カートンボード-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 186 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

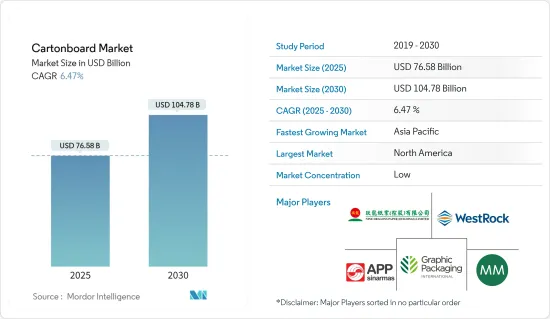

カートンボードの市場規模は2025年に765億8,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは6.47%で、2030年には1,047億8,000万米ドルに達すると予測されます。

主要ハイライト

- カートンボードの容器は、木材から作られたセルロース繊維の3層以上のプライヤーからなる板紙から作られています。カートンボードの人気が高まっているのは、その丈夫で堅い特性が製品需要を押し上げているためです。複数のエンドユーザー産業における出荷、保管、包装の目的でカートンボードの使用が増加していることが、市場成長の原動力となっています。

- カートンボード市場は、進化する消費者行動、都市化の進展、人口の購買力増加によって活況を呈するeコマース産業の影響を大きく受けています。さらに、環境意識の高い消費者はエコフレンドリー製品を好み、板紙のようなサステイナブル包装への自主的なシフトにつながり、市場の受け入れが急速に進んでいます。

- eコマースにおける包装需要の高まりと、包装材料へのセンサやその他の技術の統合です。eコマースは、製品の安全性、開梱体験、偽造防止対策、最終配送の最適化といった新たな包装に関する懸念をもたらし、特に大手eコマース小売業者の間では、一次包装と二次包装の融合に対する関心が高まっている

- プラスチック包装に代わるサステイナブル包装として、紙ベースの包装に対する需要の高まりが市場成長に寄与しています。カートンボードは他の包装材料に比べて二酸化炭素排出量が少ないため、製造業者の間で人気が高まっています。カートンボードは高い水分バリア性を持ち、印刷に適した表面特性を持つため、医薬品用途への利用が拡大しています。

- 近年、紙の価格は、需要の増加、供給問題、紙パルプ産業におけるその他の市場変化などの要因により高騰しています。また、原料不足や輸送問題など、サプライチェーンの混乱による紙の供給不足が、製品の入手を妨げることもあります。このような需給の不均衡は紙の価格を著しく上昇させ、景気回復とサプライチェーンの力学に影響される産業の課題を浮き彫りにしています。

カートンボード市場の動向

飲料セグメントが最速の成長を記録する見込み

- フルーツジュース、アルコール飲料、炭酸飲料などの飲料に対する消費者需要の高まりが、カートンボード包装の需要を牽引しています。飲料産業はますますダイナミックになっており、メーカーに飲料産業の革新的な包装ニーズに投資する成長機会をいくつか提供しています。カートンボードは、飲料の鮮度と風味を保証する高い耐湿性を提供し、製品の賞味期限を長くします。

- 固形未晒し硫酸塩(SUS)、または未晒しクラフト板紙は、包装産業で一般的に使用される丈夫で印刷可能な材料です。クラフト紙の丈夫さと白色仕上げを兼ね備えており、飲料箱や容器の製造によく使用されます。ボードの片面は通常、印刷に適するように粘土でコーティングされています。

- 長年にわたり、飲料容器のリサイクル能力を高める努力が続けられてきました。これは、リサイクル業者、技術サプライヤー、設備プロバイダとの共同投資により、新しい施設を建設することで達成されてきました。2023年6月、Tetra PakとStora Ensoは、ポーランドの飲料カートンの新しいリサイクルラインに約2,900万ユーロ(3,150万米ドル)を投資しました。このラインは、ポーランドの飲料用カートンの年間リサイクル能力を2万5,000トンから7万5,000トンに引き上げることを目的としています。

- 包装産業の様々な企業が、サステイナブル飲料用カートンの製造に投資しています。テトラパックは、飲料用カートンと環境のための同盟(ACE)のメンバーとして、2030年までにEUにおける飲料用カートンの回収率を90%、リサイクル率を70%にするという産業目標の達成に尽力しています。

- 液体カートンボード/テトラパックは、ノンアルコール飲料に牽引され、最も急速に成長している包装タイプの1つです。米国農務省(USDA)によると、2023年に米国は総額9億2,670万米ドルの果物・野菜ジュースを輸出し、その上位国はカナダ、メキシコ、日本です。

- リサイクル可能な包装材料とカートンボードの強固なリサイクル可能性に関する意識が高まっています。2023年2月、テトラパックとセーブボードは、オーストラリアのニューサウスウェールズ州で最初の飲料用カートンリサイクル施設の1つを公開しました。これは、集団的な環境目標に向けた大きな成果でした。この種の施設としては同国初のもので、余分な水や接着剤、化学品を一切消費することなく、住宅やオフィスの低炭素建材を作るためにカートンを再利用し、サステイナブル製品としています。

アジア太平洋が大きな市場シェアを占めると予想される

- 中国のカートンボード包装市場は、都市人口の増加、eコマース包装産業の発展、パルプ価格の下落、エコフレンドリー包装の使用に対する意識の向上により成長すると予測されます。同国では医薬品産業とeコマース産業が成長しており、カートンボード包装の需要を押し上げています。国際貿易局によると、Alibaba、JD.com、Pinduduoが国内のeコマース市場を独占するオンラインプラットフォームです。

- 中国の包装セグメントは進化を続け、より先進的になっています。ここ数年、果物の包装はプラスチック製が主流だったが、この地域では規制がプラスチックから紙やカートンの包装に変わりつつあり、動向が変わりつつあります。さらに、安全性と環境保護への関心が高まっていることから、今後数年間は安全な包装が食品包装の重要な焦点になると考えられます。

- インドのカートンボード市場の成長は、様々な消費財製品、医薬品、繊維製品、組織小売業、化粧品、eコマース産業などの高品質包装に対する継続的な需要が牽引しています。果物のパルプ、ジュース、その他の濃縮物の消費が伸びていることが、インドにおけるカートンボードの需要拡大を牽引しています。また、インドで急成長しているeコマース産業も市場成長を後押しすると予想されます。

- 日本では、レディトゥドリンク飲料やエナジードリンクの動向の高まりによる飲料消費の拡大が市場成長の原動力となっています。米国農務省(USDA)によると、2023年に日本で最も消費された飲料はコーヒー、緑茶、炭酸飲料です。日本は米国からノンアルコール飲料を輸入しており、市場の成長を後押ししています。

- オーストラリアでは、飲食品、eコマース、医薬品、美容・化粧品セグメントで段ボール包装の需要が大きく、紙器などの二次包装の需要が増加しています。オーストラリアでは、ノンアルコール飲料の消費量が多く、食品小売業が成長しているため、段ボール包装の需要が高まっています。オーストラリア統計局によると、2023年には1,480万トンの飲食品とノンアルコール飲料が販売され、包装産業を強化しています。

カートンボード市場概要

カートンボード市場は細分化されています。主要参入企業には、Asia Pulp & Paper Group (APP)、Mayr-Melnhof Karton AG (MM Group)、Nine Dragons Paper Holdings Limited、Westrock Company、Graphic Packaging Holding Companyなどがあります。これらの企業は、製品ポートフォリオを強化し、永続的な競合を確保するために、提携や買収などの戦略的策略を採用しています。

- 2023年9月Smurfit KappaとWestRockの合併により、Smurfit WestRockはサステナビリティに焦点を当てた世界企業として登場しました。この統合は、紙ベースの包装事業をシナジーさせ、相互補完的な強みを活かして、サステイナブル包装において世界規模で確固たる存在感を確立することを目的としています。

- 2023年4月Mayr-Melnhof Karton AG(MM Group)は、ポーランドの主要段ボール・製紙工場を強化するための包括的な投資計画を発表しました。約6億6,000万ユーロ(7億2,160万米ドル)に上るこの3部構成の計画には、エネルギーとCO2コストの削減、パルプ資源の統合、サッククラフト紙市場への参入といった対策が含まれています。これらの戦略的な動きは、工場の長期的な存続可能性と環境の持続可能性を維持するためのものです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 地政学的シナリオが市場に与える影響

- カートンボード-EXIM分析

第5章 市場力学

- 市場の促進要因

- eコマースセグメントからの旺盛な需要

- 軽量材料への需要の高まりと印刷技術革新の可能性がパーソナルケアセグメントの成長を促進

- 市場抑制要因

- 運用コストの増大

第6章 市場セグメンテーション

- 製品グレード別

- 漂白ボード

- 無漂白ボード

- 折りたたみボックスボード

- 白ラインチップボード

- 液体包装ボード

- フードサービスボード

- エンドユーザー別

- 飲料

- 食品

- 医薬品・医療

- 化粧品・トイレタリー

- タバコ

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- エジプト

- 北米

第7章 競合情勢

- 企業プロファイル

- Asia Pulp & Paper Group(APP)

- Mayr-Melnhof Karton AG(MM Group)

- Nine Dragons Paper Holdings Limited

- Westrock Company

- Graphic Packaging Holding Company

- Stora Enso OYJ

- International Paper Company

- Metsa Board

- Smurfit Kappa Group

- Pankaboard OYJ

第8章 投資分析

第9章 市場の将来

The Cartonboard Market size is estimated at USD 76.58 billion in 2025, and is expected to reach USD 104.78 billion by 2030, at a CAGR of 6.47% during the forecast period (2025-2030).

Key Highlights

- A carton board container is made from paperboard, which comprises three or more layers of pliers of cellulose fiber made from wood. The growing popularity of carton boards is attributable to their sturdy and rigid properties, thus boosting product demand. The rising use of carton boards for shipping, storage, and packaging purposes for multiple end-user industries is driving market growth.

- The carton board market is significantly influenced by the booming e-commerce industry, driven by evolving consumer behavior, rising urbanization, and the increasing purchasing power of the population. Furthermore, environmentally conscious consumers are favoring eco-friendly products, leading to a voluntary shift toward sustainable packaging like paperboard, which is gaining market acceptance rapidly.

- The packaging industry, being ever-evolving, has been impacted by technological advancements in two significant ways: the rising demand for packaging in e-commerce and the integration of sensors and other technologies into packaging materials. E-commerce has brought forth new packaging concerns such as product safety, unpacking experiences, anti-counterfeiting measures, optimization for final delivery, and a growing interest, especially among major e-commerce retailers, in merging primary and secondary packaging.

- The growing demand for paper-based packaging as a sustainable alternative to plastic packaging is contributing to market growth. Carton board has a low carbon footprint compared to other packaging materials, which has increased its popularity among manufacturers. The use of carton board packaging for pharmaceutical applications is growing as it provides a high moisture barrier and good surface properties for printing.

- In recent years, the price of paper has soared due to factors like increasing demand, availability issues, and other market changes in the pulp and paper industry. Also, the supply shortages of paper due to disruptions in the supply chain, including raw material shortages and transportation problems, can hamper product availability. This supply-demand imbalance significantly escalated paper prices, highlighting the industry's challenges influenced by economic recovery and supply chain dynamics.

Cartonboard Market Trends

The Beverage Segment is Expected to Record the Fastest Growth

- The growing consumer demand for beverages such as fruit juices, alcoholic beverages, and carbonated drinks drives the demand for carton board packaging. The beverage industry is becoming increasingly dynamic, providing manufacturers with several growth opportunities to invest in innovative packaging needs in the beverage industry. Carton board provides high resistance to humidity that ensures the freshness and flavors of the beverages, lengthening the products' shelf-life.

- Solid unbleached sulfate (SUS), or unbleached kraft paperboard, is a strong and printable material commonly used in the packaging industry. It is often used to make beverage boxes and containers, combining Kraft paper's sturdiness with a white finish. One side of the board is typically coated with a clay coating to make it suitable for printing.

- For many years, efforts have been made to increase the ability to recycle beverage containers. This has been achieved through joint investments with recyclers, technology suppliers, and equipment providers to build new facilities. In June 2023, Tetra Pak and Stora Enso invested roughly EUR 29 million (USD 31.5 million) in a new recycling line for beverage cartons in Poland. This line was intended to multiply the country's yearly recycling capacity of beverage cartons - from 25,000 to 75,000 tonnes.

- Various companies in the packaging industry invest in manufacturing sustainable cartons for beverages. As a member of the Alliance for Beverage Cartons and the Environment (ACE), Tetra Pak is dedicated to achieving the industry objective of having a 90% collection rate and a 70% recycling rate for beverage cartons in the EU by 2030.

- Liquid carton boards/tetra packs are one of the fastest-growing packaging types, driven by non-alcoholic beverages. According to the US Department of Agriculture (USDA), in 2023, the United States exported fruit and vegetable juices totaling a value of USD 926.7 million, with the top countries being Canada, Mexico, and Japan.

- Awareness regarding recyclable packaging material and the robust recyclability feature of carton boards is rising. In February 2023, Tetra Pak and Save Board disclosed one of the first beverage carton recycler facilities in New South Wales, Australia. This was a major accomplishment toward the collective environmental objectives. It was the first of its kind in the country; it reuses the cartons to create low-carbon building materials for homes and offices without consuming any extra water, adhesives, or chemicals, thus making it a sustainable product.

Asia-Pacific is Expected to Hold a Significant Market Share

- China's market for carton board packaging is projected to grow due to the growing urban population, an evolving e-commerce package industry, declining pulp prices, and improving awareness of the use of eco-friendly packaging. The growing pharmaceutical and e-commerce industry in the country is boosting the demand for carton board packaging. According to the International Trade Administration, Alibaba, JD.com, and Pinduduo are the domestic online platforms that dominate the country's e-commerce market.

- The Chinese packaging sector continues to evolve and become more advanced. For the past few years, most fruit package options have been made of plastic; however, the trend is changing in the region, with regulations changing from plastics to paper and carton packages. In addition, given the increasing concern about safety and environmental protection, safe packaging is set to become a significant focus for food packaging over the next few years.

- India's carton board market's growth is driven by continued demand for quality packaging of various consumer goods products, pharmaceuticals, textiles, organized retail, cosmetics, and e-commerce industries. The growing consumption of fruit pulps, juices, and other concentrates drives the growing demand for carton boards in India. Also, the rapidly growing e-commerce industry in India is expected to boost market growth.

- The growing beverage consumption in Japan due to the rising trend of ready-to-drink beverages and energy drinks drives the market growth. According to the US Department of Agriculture (USDA), coffee, green tea, and carbonated drinks were the most consumed beverages in Japan in 2023. Japan imports non-alcoholic beverages from the United States, boosting the market growth.

- Australia witnessed huge demand for corrugated packaging in the food and beverage, e-commerce, pharmaceutical, and beauty and cosmetics sectors, increasing the demand for secondary packaging, such as folding cartons, in the country. The high consumption of non-alcoholic beverages and the growing food retail sector in the country boosts the demand for packaging. According to the Australian Bureau of Statistics, 14.8 million tons of food and non-alcoholic beverages were sold in 2023, enhancing the packaging industry.

Cartonboard Market Overview

The carton board market is fragmented. Key players include Asia Pulp & Paper Group (APP), Mayr-Melnhof Karton AG (MM Group), Nine Dragons Paper Holdings Limited, Westrock Company, and Graphic Packaging Holding Company. These companies employ strategic maneuvers like partnerships and acquisitions to fortify their product portfolios and secure a lasting competitive edge.

- September 2023: Smurfit WestRock emerged as a sustainability-focused global force following the merger of Smurfit Kappa and WestRock. This consolidation aimed to synergize its paper-based packaging businesses, capitalizing on its complementary strengths to establish a formidable presence in sustainable packaging on a global scale.

- April 2023: Mayr-Melnhof Karton AG (MM Group) greenlit a comprehensive investment initiative designed to fortify Poland's major cardboard and paper mill. Valued at approximately EUR 660 million (USD 721.6 million), this three-part plan entails measures to curtail energy and CO2 expenses, integrate pulp resources, and penetrate the sack kraft paper market. These strategic moves were geared toward positioning the plant for sustained long-term viability and environmental sustainability.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of the Geo-Political Scenarios on the Market

- 4.5 Cartonboard - EXIM Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Strong Demand from the E-commerce Sector

- 5.1.2 Growing Demand for Lightweight Materials and Scope for Printing Innovations Propelling Growth in the Personal Care Segment

- 5.2 Market Restraints

- 5.2.1 Increasing Operational Costs

6 MARKET SEGMENTATION

- 6.1 By Product Grade

- 6.1.1 Solid Bleached Board

- 6.1.2 Solid Unbleached Board

- 6.1.3 Folding Boxboard

- 6.1.4 White-lined Chipboard

- 6.1.5 Liquid Packaging Board

- 6.1.6 Food Service Board

- 6.2 By End-User

- 6.2.1 Beverage

- 6.2.2 Food

- 6.2.3 Pharmaceutical and Healthcare

- 6.2.4 Cosmetics and Toiletries

- 6.2.5 Tobacco

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Australia and New Zealand

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Argentina

- 6.3.4.3 Mexico

- 6.3.5 Middle East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 South Africa

- 6.3.5.4 Egypt

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Asia Pulp & Paper Group (APP)

- 7.1.2 Mayr-Melnhof Karton AG (MM Group)

- 7.1.3 Nine Dragons Paper Holdings Limited

- 7.1.4 Westrock Company

- 7.1.5 Graphic Packaging Holding Company

- 7.1.6 Stora Enso OYJ

- 7.1.7 International Paper Company

- 7.1.8 Metsa Board

- 7.1.9 Smurfit Kappa Group

- 7.1.10 Pankaboard OYJ